Sabitlenmiş Tweet

CHAINS ARE THE NEW TOKENS.

Launch phase

In 2017, during the ETH ICO craze, it was really easy to launch your new tokens

In 2023, building your own ETH L2 chain will be easy.

English

sanket.polygon (agg/layer)

5.6K posts

@sourcex44

@polarisfund crypto observoor

I’m happy @Polymarket is going away from @0xPolygon. I was discussing with my bro @0xDmitry (huge PM guy), and I see a lot of use cases for conditional DeFi, so trades and more based on outcomes, basically using PM as a on-chain-verified newspaper. The problem is that Polygon doesn’t have liquidity and volume, looks like a dead chain to me, but if Polymarket will go on ETH or @unichain or @base, I want to build something on top of @Uniswap V4 + Polymarket!

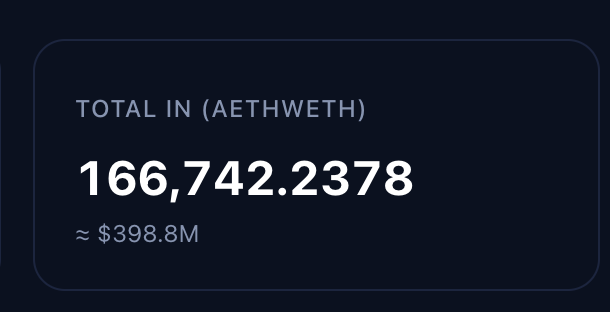

Introducing aWETH Redemption Protocol With ETH utilization at 100% on Aave, many lenders are currently unable to withdraw and face increasing risk if markets move. aWETH Redemption Protocol allows ETH lenders to: • Exit into wstETH or weETH • Regain immediate liquidity • Reduce exposure to liquidation risk If you’re just lending ETH — you can fully exit. If you have ETH collateral and another debt — your collateral is seamlessly swapped into wstETH or weETH while your debt remains the same. We’re working alongside @LidoFinance , @ether_fi, @0xProject, @1inch, @KyberNetwork, and other ecosystem partners to: • Reduce systemic risk in DeFi • Ease utilization pressure • Support a healthier DeFi market Our goal is simple: protect users while reinforcing the foundations of DeFi. Capacity is initially limited to $1B in ETH. fluid.io/lite/aave-v3/e…

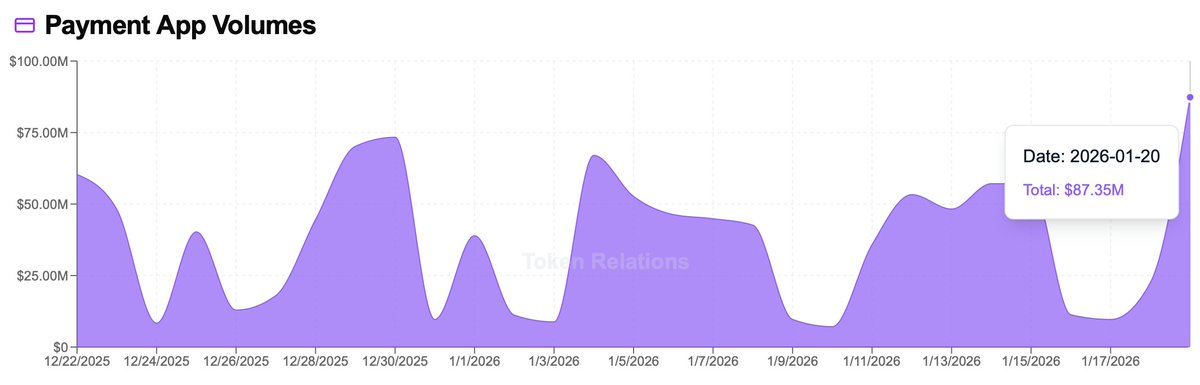

JPYC払い一番乗り!😆 HashPortウォレットでQRを読み取って、PayPayみたいに金額を自分で入力して払う。5秒ほどで送金完了、早い!(けどPayPayと比べると遅い) 選択肢なしにPolygonチェーン。 刻まれてしまった。 レシートにはJPYCとは書かれず、現金と同じ扱いだと思います。 興奮してきた!

There have recently been some discussions on the ongoing role of L2s in the Ethereum ecosystem, especially in the face of two facts: * L2s' progress to stage 2 (and, secondarily, on interop) has been far slower and more difficult than originally expected * L1 itself is scaling, fees are very low, and gaslimits are projected to increase greatly in 2026 Both of these facts, for their own separate reasons, mean that the original vision of L2s and their role in Ethereum no longer makes sense, and we need a new path. First, let us recap the original vision. Ethereum needs to scale. The definition of "Ethereum scaling" is the existence of large quantities of block space that is backed by the full faith and credit of Ethereum - that is, block space where, if you do things (including with ETH) inside that block space, your activities are guaranteed to be valid, uncensored, unreverted, untouched, as long as Ethereum itself functions. If you create a 10000 TPS EVM where its connection to L1 is mediated by a multisig bridge, then you are not scaling Ethereum. This vision no longer makes sense. L1 does not need L2s to be "branded shards", because L1 is itself scaling. And L2s are not able or willing to satisfy the properties that a true "branded shard" would require. I've even seen at least one explicitly saying that they may never want to go beyond stage 1, not just for technical reasons around ZK-EVM safety, but also because their customers' regulatory needs require them to have ultimate control. This may be doing the right thing for your customers. But it should be obvious that if you are doing this, then you are not "scaling Ethereum" in the sense meant by the rollup-centric roadmap. But that's fine! it's fine because Ethereum itself is now scaling directly on L1, with large planned increases to its gas limit this year and the years ahead. We should stop thinking about L2s as literally being "branded shards" of Ethereum, with the social status and responsibilities that this entails. Instead, we can think of L2s as being a full spectrum, which includes both chains backed by the full faith and credit of Ethereum with various unique properties (eg. not just EVM), as well as a whole array of options at different levels of connection to Ethereum, that each person (or bot) is free to care about or not care about depending on their needs. What would I do today if I were an L2? * Identify a value add other than "scaling". Examples: (i) non-EVM specialized features/VMs around privacy, (ii) efficiency specialized around a particular application, (iii) truly extreme levels of scaling that even a greatly expanded L1 will not do, (iv) a totally different design for non-financial applications, eg. social, identity, AI, (v) ultra-low-latency and other sequencing properties, (vi) maybe built-in oracles or decentralized dispute resolution or other "non-computationally-verifiable" features * Be stage 1 at the minimum (otherwise you really are just a separate L1 with a bridge, and you should just call yourself that) if you're doing things with ETH or other ethereum-issued assets * Support maximum interoperability with Ethereum, though this will differ for each one (eg. what if you're not EVM, or even not financial?) From Ethereum's side, over the past few months I've become more convinced of the value of the native rollup precompile, particuarly once we have enshrined ZK-EVM proofs that we need anyway to scale L1. This is a precompile that verifies a ZK-EVM proof, and it's "part of Ethereum", so (i) it auto-upgrades along with Ethereum, and (ii) if the precompile has a bug, Ethereum will hard-fork to fix the bug. The native rollup precompile would make full, security-council-free, EVM verification accessible. We should spend much more time working out how to design it in such a way that if your L2 is "EVM plus other stuff", then the native rollup precompile would verify the EVM, and you only have to bring your own prover for the "other stuff" (eg. Stylus). This might involve a canonical way of exposing a lookup table between contract call inputs and outputs, and letting you provide your own values to the lookup table (that you would prove separately). This would make it easy to have safe, strong, trustless interoperability with Ethereum. It also enables synchronous composability (see: ethresear.ch/t/combining-pr… and ethresear.ch/t/synchronous-… ). And from there, it's each L2's choice exactly what they want to build. Don't just "extend L1", figure out something new to add. This of course means that some will add things that are trust-dependent, or backdoored, or otherwise insecure; this is unavoidable in a permissionless ecosystem where developers have freedom. Our job should make to make it clear to users what guarantees they have, and to build up the strongest Ethereum that we can.

i see u @0xPolygon 👀 was not familiar w your game

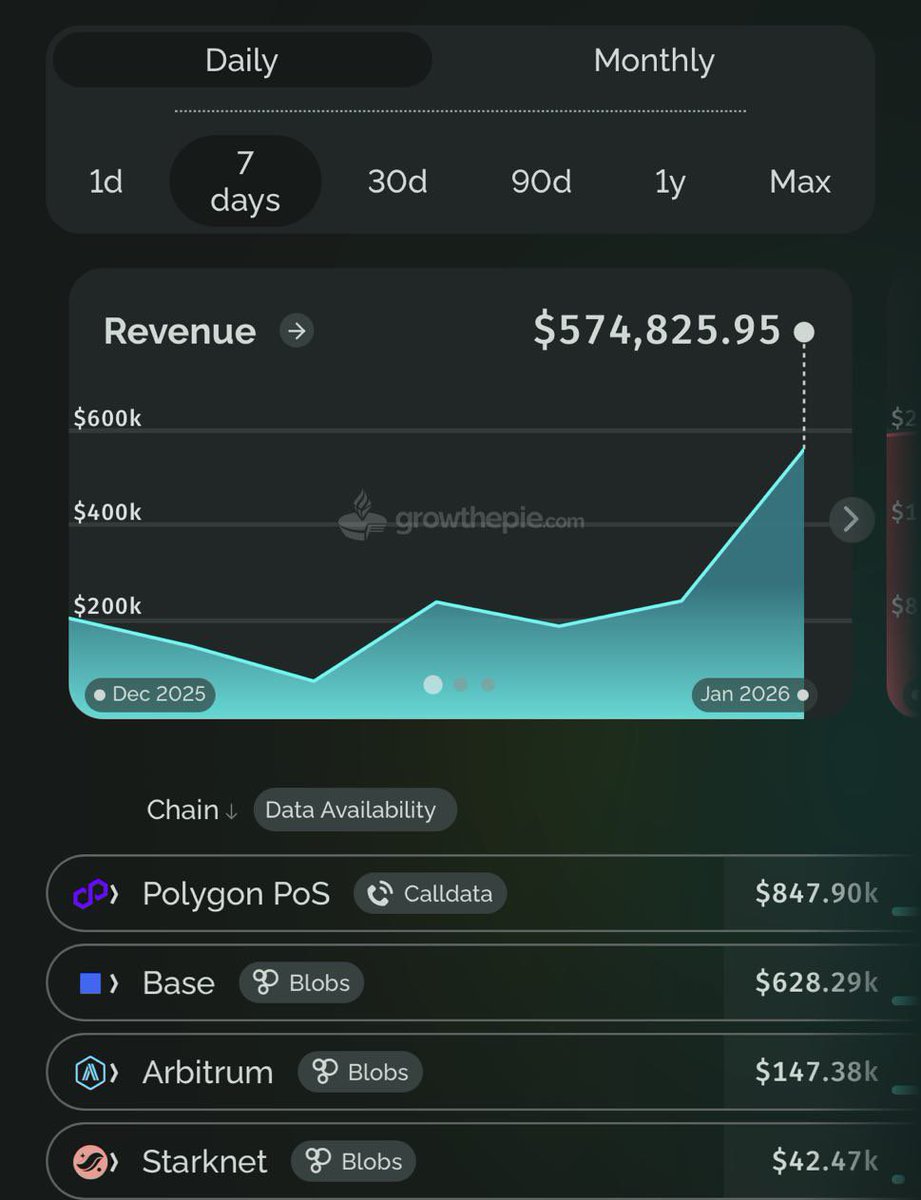

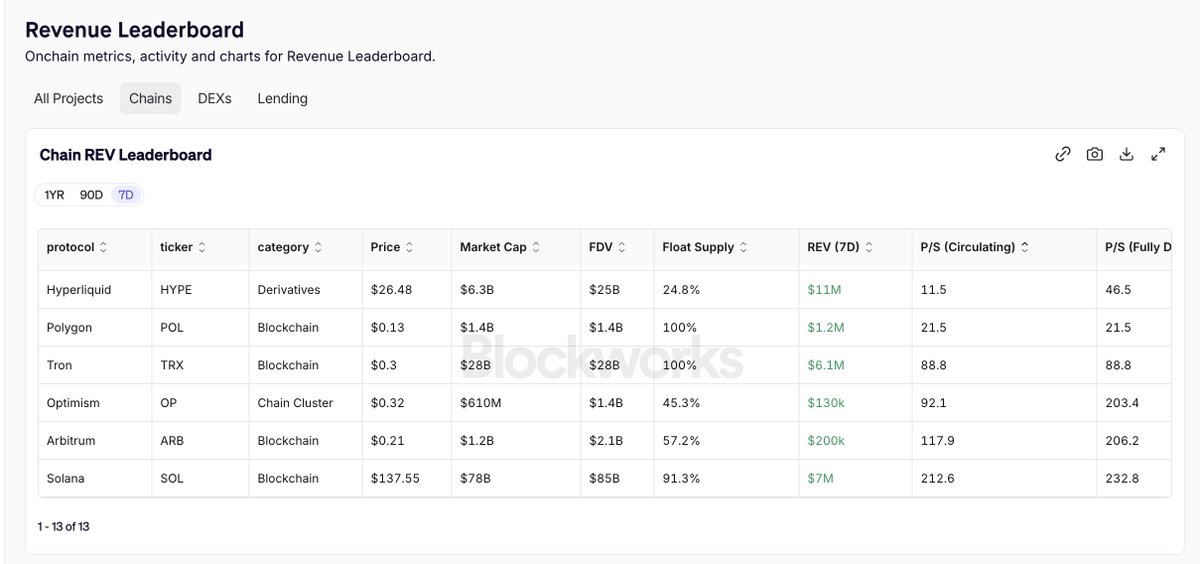

Polygon PoS doing $1.4 mn revenue is last 7 days growing at 75% week on week due to micro payments and prediction market usage h/t @GrowThePie

Polygon PoS doing more revenue than Base and Arbitrum in last 7 days💹💹 h/t @growthepie_eth @0xPolygon