Sabitlenmiş Tweet

🧵 Types of Credit Cards – Understanding the basics

Credit Cards are often spoken about as a single product.

In reality, they are designed differently for different use cases.

Let’s understand the types 👇

English

Kishor Naik

284 posts

@thatfinanceguy

That Finance Guy 💸 CA who breaks down money like a friend, not a textbook. Credit cards · investing · tax · insurance ✌🏻

The single most under-rated category in India is the mid-cap. I remember talking with @deepakshenoy on how the Nifty Next 50 (or JuniorBees) is actually a rock solid index to own. So..

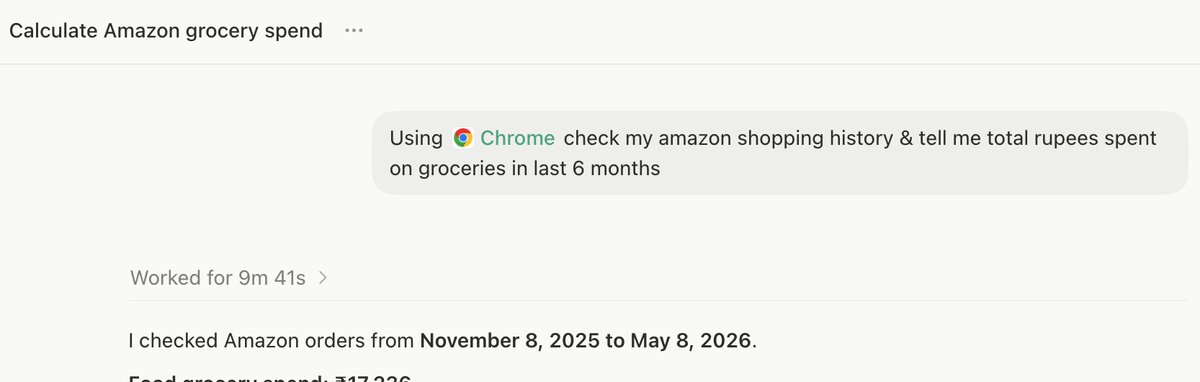

Codex now works directly in Chrome on macOS and Windows. It’s even better at working with apps and sites in Chrome, and now works in parallel across tabs in the background without taking over your browser. To get started, install the Chrome plugin in the Codex app.

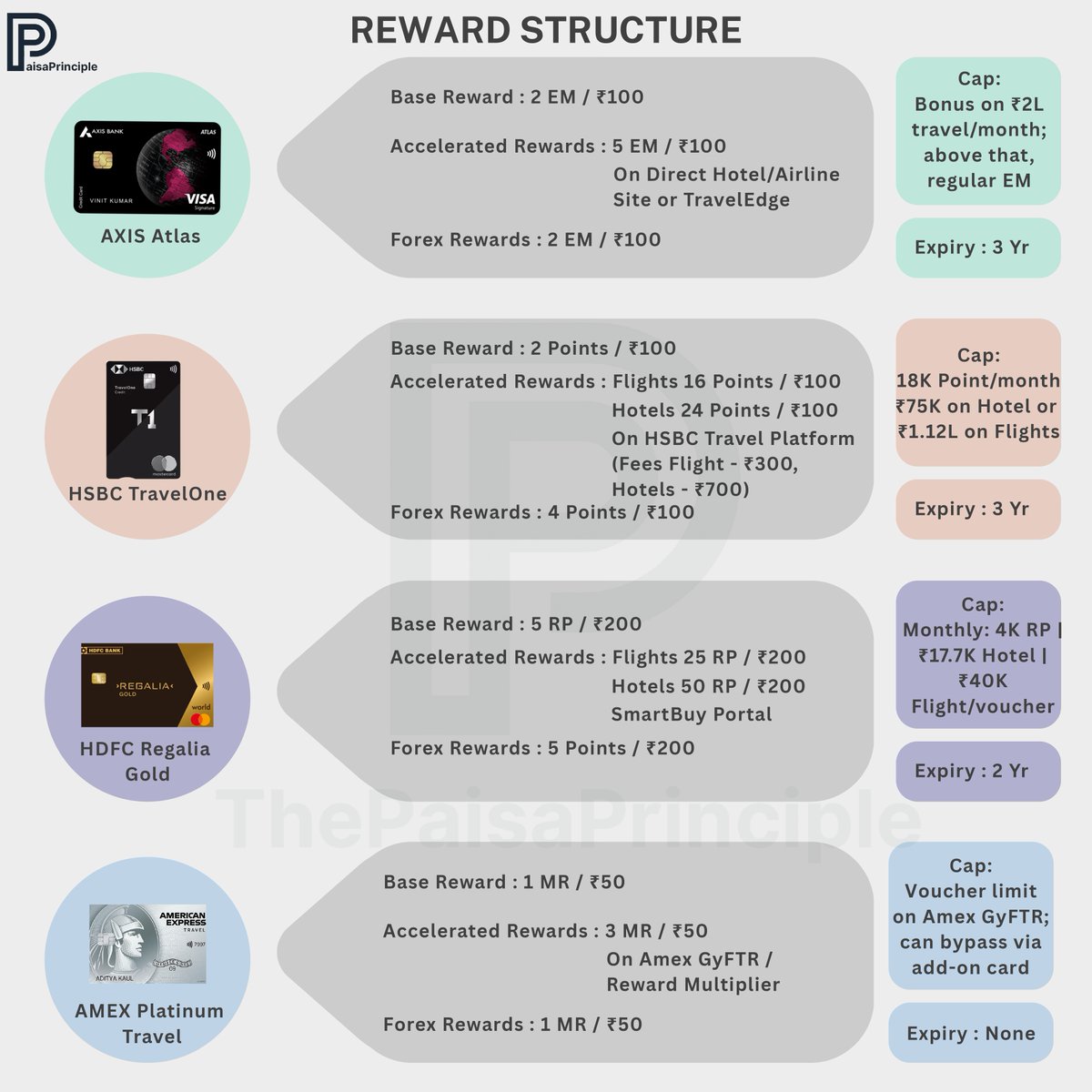

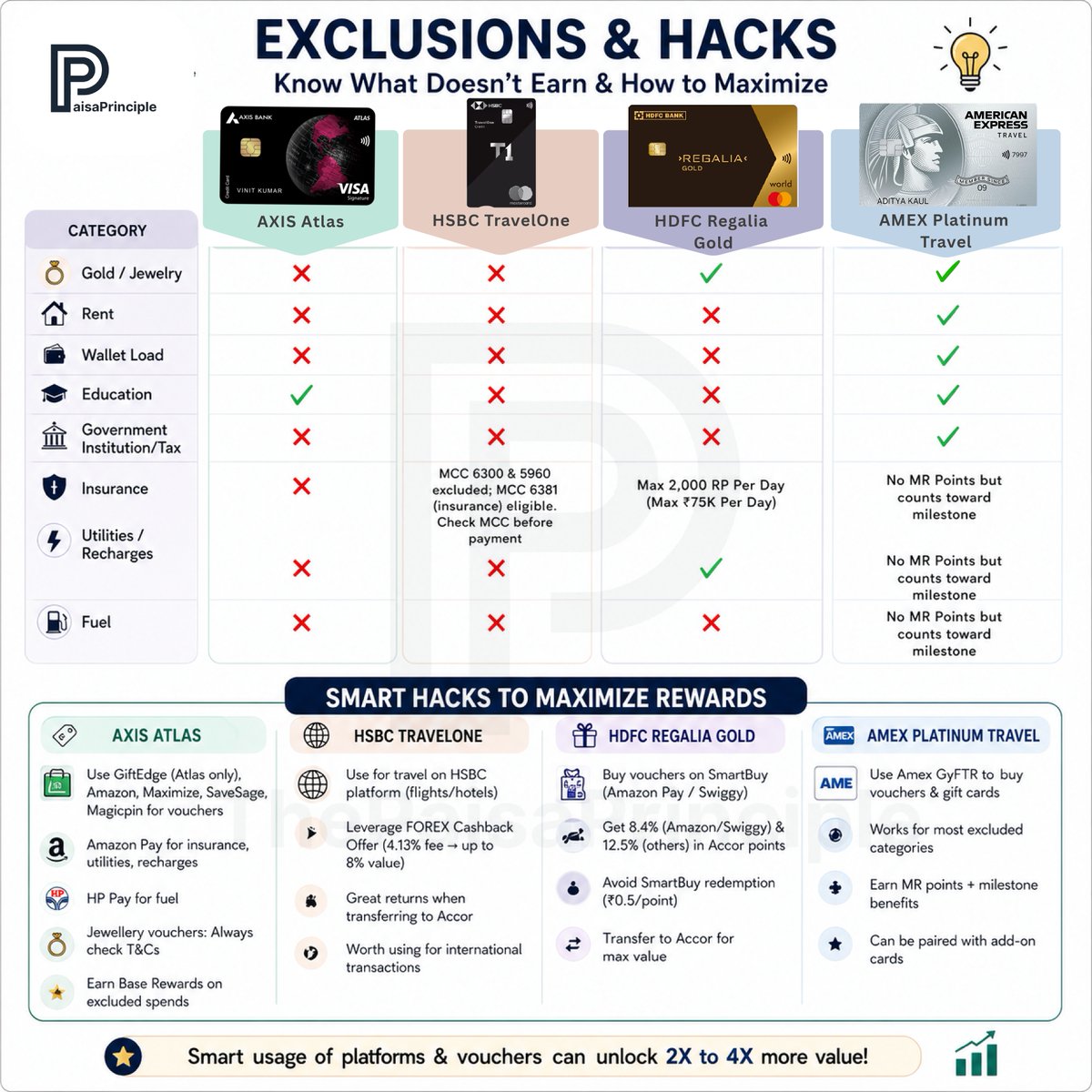

This is the ultimate comparison of 4 travel focused credit cards: 1️⃣ Axis Atlas 2️⃣ HSBC TravelOne 3️⃣ HDFC Regalia Gold 4️⃣ Amex Plat Travel Swipe through visuals to see: 📌 Key Features 📌 Exclusions 📌 Lounge Access #CCGeek #CreditCards #CCGeeks #TravelOnPoints

Completely incorrect argument, For many, many years, The entire life insurance industry has sold life insurance products as tax-saving products, In March, In a rush to complete targets, People made crazy sales on life insurance, Now, The government has completely done away with tax deductions on life insurance. The entire life insurance industry is struggling to sell! The primary purpose of life insurance is not to save tax, Life Insurance is a product to mitigate the life risk of the earning members, Tax incentives were just an added tool, Life insurance is also an investment tool, It is a tool to hedge life risks of the earning members, At Hercules Insurance, We sell only term plans and no other products. We have seen nearly 100% growth in the number of term plans we gave to customers. A plain vanilla term plan until retirement is the only life insurance product u need. Rest all prodcuts only make the agents and the life insurance company rich Selling and buying the right life insurance is the key to covering the risks correctly!

🇮🇳 Indians are so desperate to buy US tech that there are ZERO sellers on MON100 today. ETF is trading at 20% premium People are paying ₹316 for something worth 264. That's desperation tax. 💸 Go direct. Buy the actual US ETF. Join our webinar to learn how. Comment global.

Wife had been admitted for a small surgery and there has been a very negligent response from the team of Health Insurance TPA of India Ltd who have rejected a claim, which as not even in lakhs, by simply sending a denial letter without any clarification for a policy that has been there for nearly a decade now. There has been no response whatsoever and no questions asked. This has been my first experience of dealing with a TPA and found this one a very unprofessional organisation.