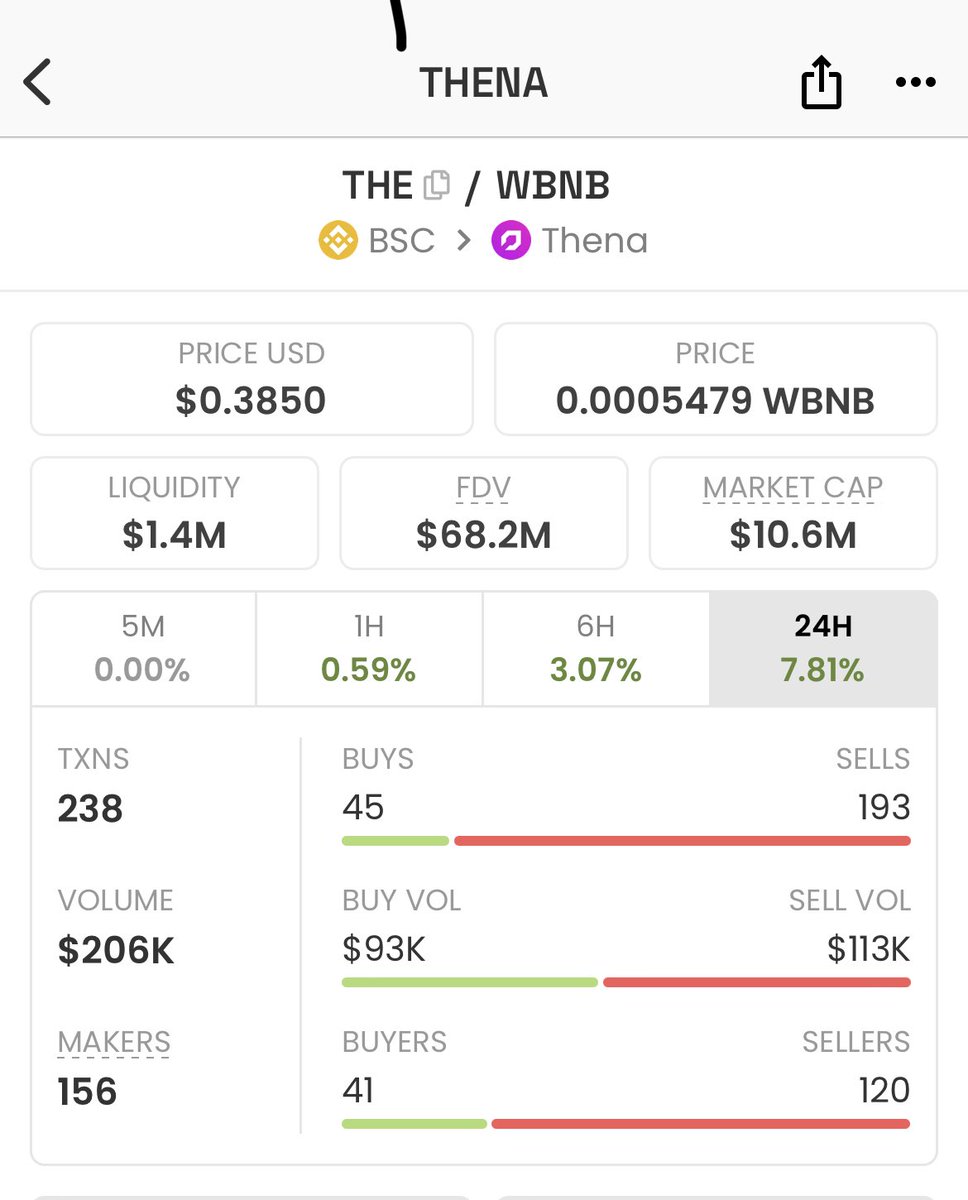

Sabitlenmiş Tweet

(💜,🏛️) THREAD COMPETITION (💜,🏛️)

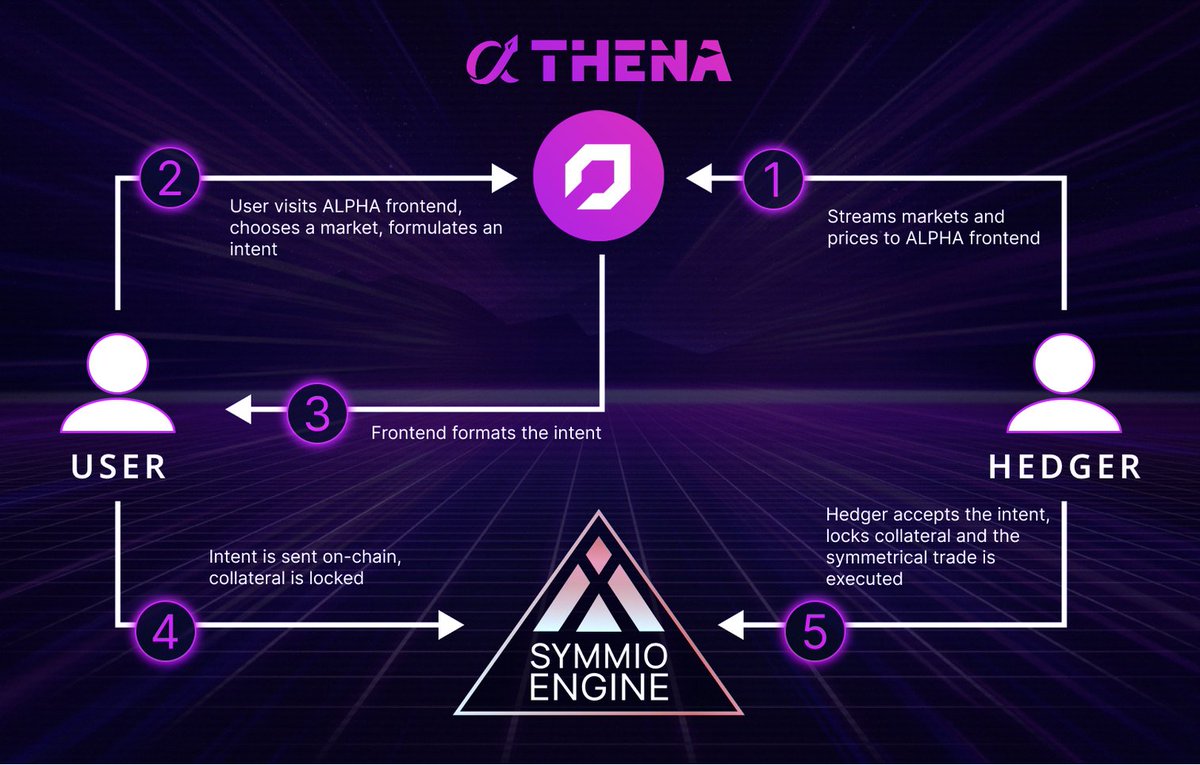

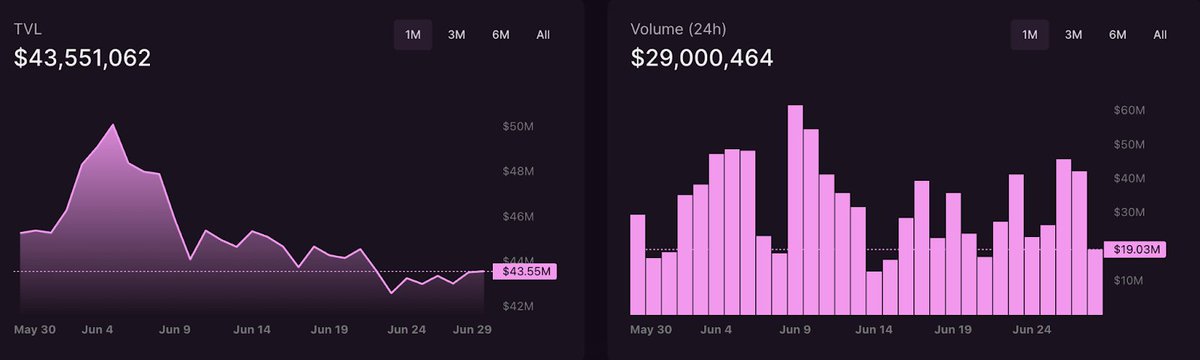

$the Scribe challenges all Thenians to show the CT empire how data proves @thenafi is $the superior and most undervalued DEX token!

Win 250 $liveTHE if you are a gladiator who’s up to the challenge.

GIF

English