Sabitlenmiş Tweet

FINDING WINNING INVESTMENTS 🔍

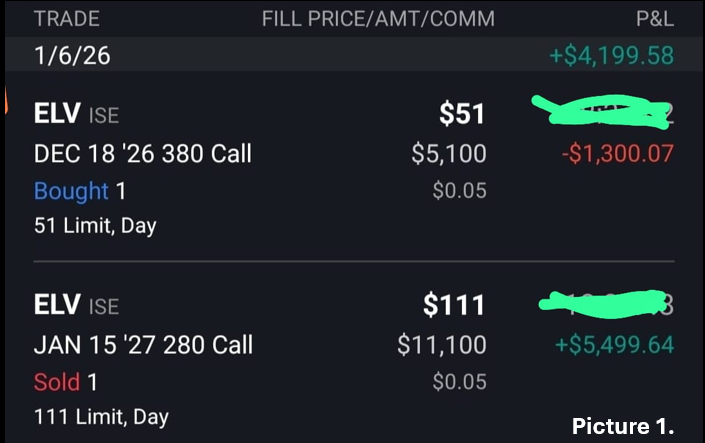

A real example using options on Elevance Health (Picture 1)

After closing my option trade on Elevance Health, I wanted to step back and review my decision-making process:

♦️What I did well

♦️Where I made mistakes

♦️ What can be improved next time?

The goal of this breakdown is education. Bookmark it so you can return to it later.

If you are new to investing or still learning, this is an example of how a full investment thesis can look in practice, from:

idea ➡️execution ➡️ mistakes ➡️lessons

Elevance Health is part of the healthcare insurance group, together with names like UnitedHealth Group and Humana.

WHY DO I USE OPTIONS (ESPECIALLY LEAPS)?

I primarily use long-dated options (LEAPS, 1+ year to expiration) because they offer leverage.

Example from this trade:

♦️Capital invested: $5,600

♦️Profit realized: $4,200

♦️Return: ~75%

♦️Stock price move: ~36% (from ~$275 to ~$375)

If I had bought shares instead:

♦️Same capital ➡️ ~20 shares

♦️Profit on the same move: ~$2,000

Why options can make sense:

♦️You control more shares with less capital

♦️Returns are magnified when the thesis plays out

Key risk (important):

♦️Options have a time limit

♦️If price moves against you, losses can also accelerate

👉 Lesson for readers: options are powerful tools, but only when paired with a strong thesis and risk control.

MY FILTER: WHEN DOES A STOCK BECOME INTERESTING?

A company must pass multiple filters.

1. Technical setup (weekly chart only)

I want:

♦️Price trading at multi-year lows;

🏹Minimum: 2 years

🏹Better: 4+ years (ELV met this)

♦️RSI oversold at the same time

♦️All signals confirmed on the weekly timeframe

👉 This tells me pessimism is already priced in.

2. Fundamentals vs price

Next, I compare operating performance vs market value (Picture 2)

What I check:

♦️Revenue growth

♦️Operating income

♦️Net income

♦️Market cap at each year’s closing price

What I want to see:

♦️Business metrics are higher than several years ago

♦️Valuations below historical averages

👉 If fundamentals improve but price collapses, something is mispriced.

3. Sector logic (big picture)

Every sector has its own drivers.

For healthcare insurance, my thinking was simple:

♦️Healthcare demand is a necessity, not an option

♦️An aging population = rising healthcare costs

I did a deeper TAM (Total Addressable Market) analysis (can be found on my free Substack, link is in my bio).

TLDR ➡️ The long-term demand is structurally strong.

👉 This reduces the risk of a broken thesis.

CHOOSING THE BEST COMPANY IN THE SECTOR

Once the sector passed my filter, I compared companies side by side:

What I looked at:

♦️Valuation ratios

♦️Cash vs debt

♦️Operating margins

♦️Stock-based compensation

Why I chose Elevance Health:

♦️Fewer regulatory concerns than UnitedHealth

♦️Better operating margins than Humana

♦️Cleaner balance-sheet profile overall

Important insight (in hindsight):

♦️UNH, ELV, or HUM would all have worked

As the saying goes: a rising tide lifts all boats, the tide here being the sector, and the boats being individual companies.

👉 Sometimes being “right on the sector” matters more than picking the perfect name.

DEFINING A REALISTIC PRICE TARGET

Before entering, I checked if my expectations were reasonable.

♦️Entry zone: ~$275

♦️Target: $375

♦️Required move: ~36%

♦️Timeframe: ~1.5 years (option expiry)

♦️Break-even at expiration: ~18%

Even at $375:

The stock would still be ~30% below all-time highs

👉 This told me the target was realistic, just personal preference.

WHAT WENT WRONG ( AND WHY IT MATTERS)

The stock rallied sharply to $360+ by October.

Drivers included:

♦️Rotation into defensive stocks

♦️AI bubble fears

♦️Government shutdown rumors benefiting healthcare

My first mistake (Picture 3)

I did not hedge near resistance.

♦️The weekly chart printed a bearish doji

♦️Price hit upper resistance

♦️I ignored it, thinking: “just a bit more.”

Result:

♦️Drop from ~$360 to nearly $300

♦️Textbook pullback to 0.618 Fibonacci

👉 Lesson: strong conviction does not replace risk management.

WHAT I DID RIGHT

♦️I did not panic

♦️I reassessed the thesis

♦️Fundamentals and sector logic were unchanged

♦️I stayed in the position

The uptrend resumed in December.

HEDGING: RIGHT IDEA, WRONG TIMING

When the price approached $360 again:

♦️Resistance was broken and held

♦️Political uncertainty (midterms) increased

♦️I decided to hedge the position

One week later:

♦️The target of $375 was hit

♦️The hedge reduced my final profit

👉 Final lesson:

Hedging is not about being safe, but about timing and structure, something I still need to improve.

KEY TAKEAWAYS FOR READERS

♦️A good investment starts before the trade

♦️Combine technical + fundamentals + sector logic

♦️Options amplify both gains and mistakes

♦️Have a plan for entries, exits, and risk

♦️Mistakes are part of the process; reviewing them is

the edge

This is how my Elevance Health thesis was built, tested, challenged, and ultimately closed.

Congrats if you made it to the end. 🎊

If this breakdown helped you understand how an investment thesis is built, a retweet helps others learn too.

DISCLAIMER:

This post is an educational breakdown based on my own experience, not financial advice.

English