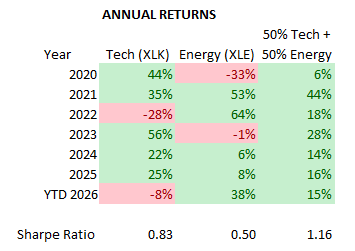

@MicropediaRJ @johnarnold @deepvest_ai Yeah you’re right. This is basically tech outperforming during this time period. XLK outperforms the equal weight

English

Toby Wade

886 posts

@tobyjwade

CEO at DeepVest | 24/7 Agentic CIO for Financial Advisors | Ex-Head of ML, BofA & Gemini | # Not investment advice

Exclusive: OpenAI is backing a new AI startup that aims to build software allowing so-called AI “agents” to communicate and solve complex problems in industries such as finance and biotech on.wsj.com/4bTvwKd

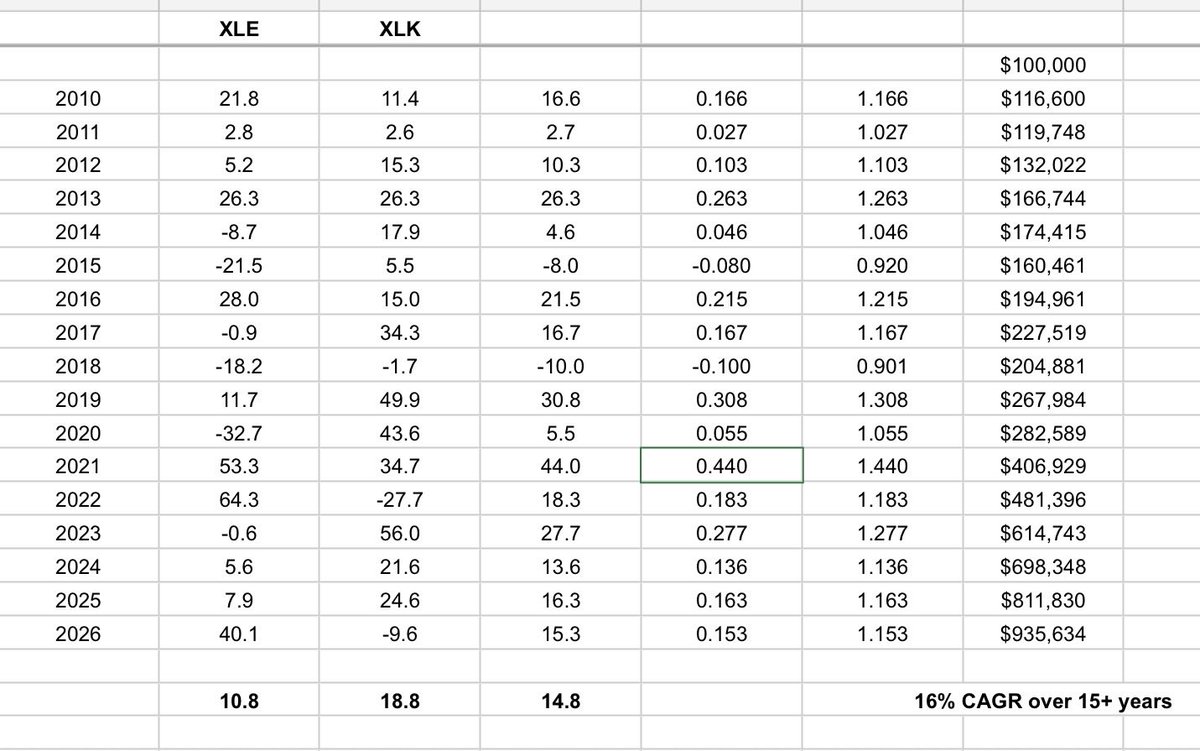

I verified the claim but went little further back in time using @deepvest_ai 🥇 Massive outperformance on total return: The portfolio delivered 651.49% vs. 389.45% for the S&P 500 — a difference of over 262 percentage points over 15 years. 📉 Higher volatility is the trade-off: The portfolio's annualised vol of 21.25% is notably higher than the S&P 500's 17.28%, reflecting the concentrated sector exposure. ⚖️ Better risk-adjusted returns: Despite the higher volatility, the Sharpe ratio of 0.74 edges out the S&P 500's 0.70, meaning the portfolio generated more return per unit of risk. 🔻 Slightly deeper drawdown: Max drawdown of -35.22% vs. -33.92% for the S&P 500 — marginally worse but comparable. 📐 Beta of 1.17 confirms the portfolio is more sensitive to market moves than the broad index — amplifying both gains and losses. here's the shared chat deepvest.ai/shared/42d96c9…

I think I finally solved the stock market.

I verified the claim but went little further back in time using @deepvest_ai 🥇 Massive outperformance on total return: The portfolio delivered 651.49% vs. 389.45% for the S&P 500 — a difference of over 262 percentage points over 15 years. 📉 Higher volatility is the trade-off: The portfolio's annualised vol of 21.25% is notably higher than the S&P 500's 17.28%, reflecting the concentrated sector exposure. ⚖️ Better risk-adjusted returns: Despite the higher volatility, the Sharpe ratio of 0.74 edges out the S&P 500's 0.70, meaning the portfolio generated more return per unit of risk. 🔻 Slightly deeper drawdown: Max drawdown of -35.22% vs. -33.92% for the S&P 500 — marginally worse but comparable. 📐 Beta of 1.17 confirms the portfolio is more sensitive to market moves than the broad index — amplifying both gains and losses. here's the shared chat deepvest.ai/shared/42d96c9…

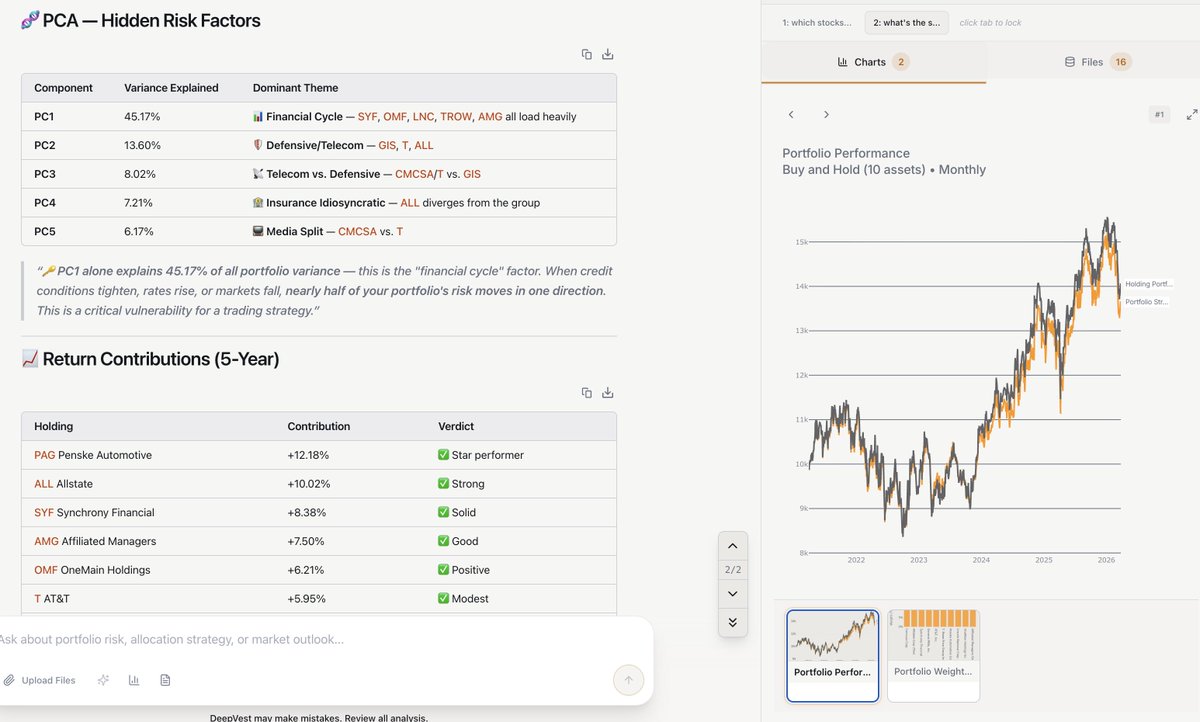

Right, did we mention you can run macro backtesting now like these? 👇

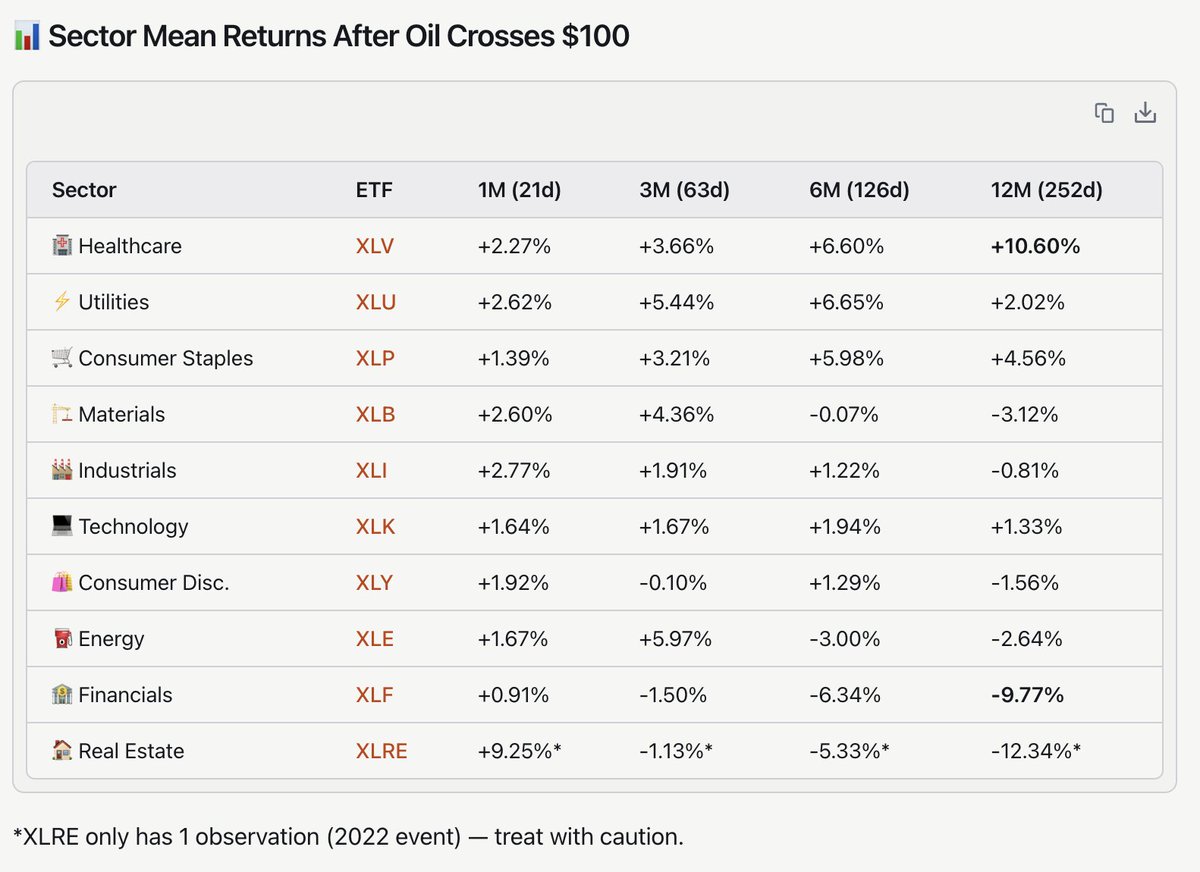

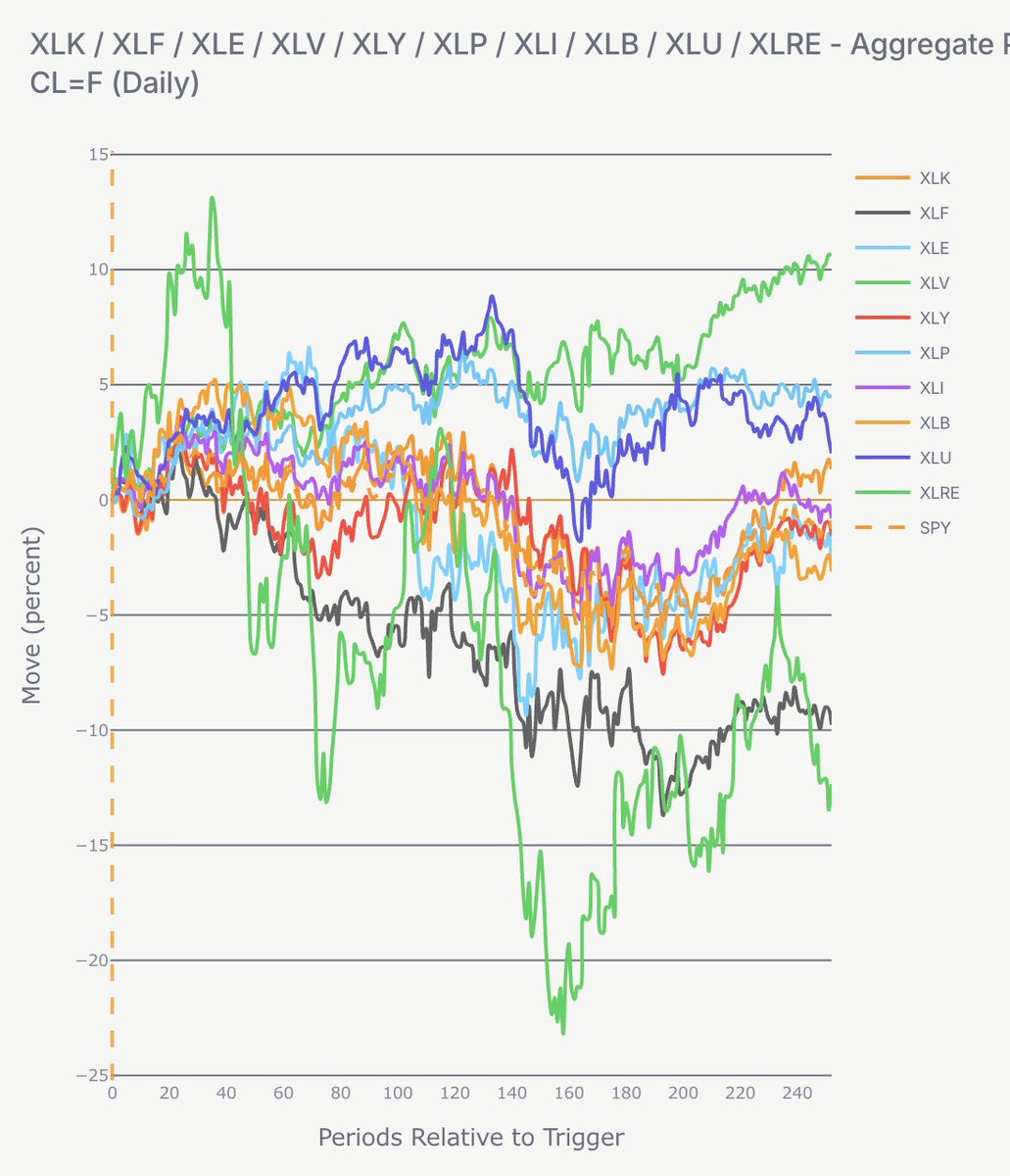

As the price of oil gets closer to $100, what has been the market reaction across the US sectors. Five times over last 15 years or so: -2008-02-19 -2011-03-02 -2013-07-03 -2014-07-16 -2022-03-01 The macro narrative is clear: When oil crosses $100, markets price in stagflation risk — investors rotate into defensive sectors (Healthcare, Utilities, Staples) and away from rate-sensitive and credit-dependent sectors (Financials, Real Estate). Energy's initial pop tends to fade as demand destruction fears take hold. My prompt to @deepvest_ai upgraded macro agent "what happens historically every time the price of oil crosses $100 across the main sectors in the SP 500?"

I packaged up the "autoresearch" project into a new self-contained minimal repo if people would like to play over the weekend. It's basically nanochat LLM training core stripped down to a single-GPU, one file version of ~630 lines of code, then: - the human iterates on the prompt (.md) - the AI agent iterates on the training code (.py) The goal is to engineer your agents to make the fastest research progress indefinitely and without any of your own involvement. In the image, every dot is a complete LLM training run that lasts exactly 5 minutes. The agent works in an autonomous loop on a git feature branch and accumulates git commits to the training script as it finds better settings (of lower validation loss by the end) of the neural network architecture, the optimizer, all the hyperparameters, etc. You can imagine comparing the research progress of different prompts, different agents, etc. github.com/karpathy/autor… Part code, part sci-fi, and a pinch of psychosis :)