Moody@MoodyWriter13

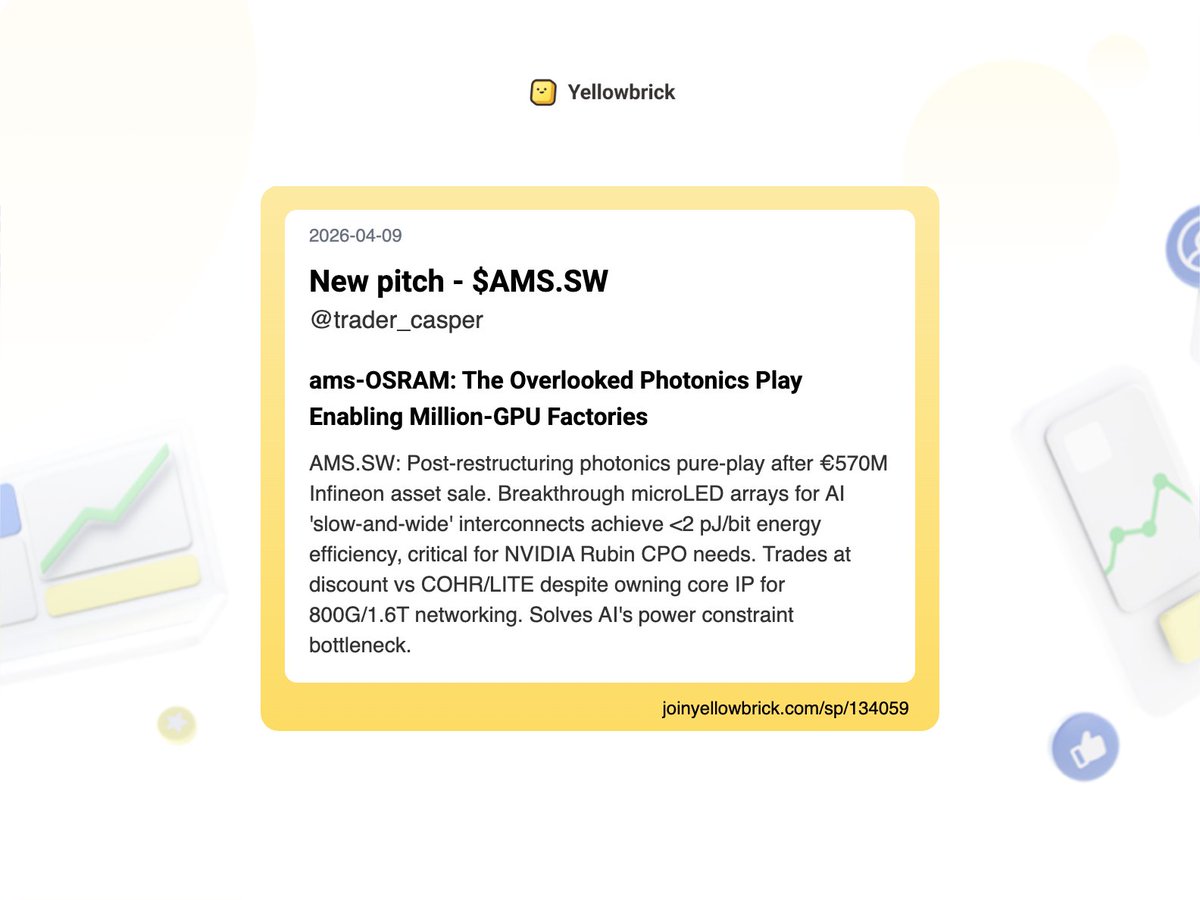

Right now, virtually every European company with a photonics angle is being hyped, even when it has little or nothing to do with the actual demand driver in AI data centers. All the more remarkable that this isn’t happening to Germany’s premier photonics company, ams OSRAM (€1.16bn Market Cap). Upfront: there is currently no meaningful exposure to AI data centers, but there is a technologically compelling pipeline. Together with AMS, OSRAM commands one of the broadest competence bases in photonics and especially sensing, from automotive through MedTech to industrial applications. It also appears well positioned in VR/AR, and prospectively in robotics.

On March 18, ams OSRAM unveiled a microLED prototype: hundreds of tiny LEDs, each roughly half the width of a human hair, transmitting data in parallel between servers. Instead of a few extremely fast lasers, the approach uses many slower channels with a significantly better energy profile. They call it “slow-and-wide optical interconnects.”

Microsoft and MediaTek announced their own microLED AOC collaboration on March 17 – one day before ams OSRAM. Doug Burger, Technical Fellow and CVP at Microsoft Research, calls it “a major leap in AI datacenter efficiency.” Hyperscalers see microLED as a serious path forward, not an academic experiment.

According to MediaTek/Microsoft, the approach enables up to 50% energy savings versus VCSEL-based solutions – and energy is the central bottleneck in data center expansion.

Beyond energy, reliability matters. Microsoft Research’s MOSAIC paper (SIGCOMM 2025) reports that an optical link fails every 6 to 12 hours in a 100,000-GPU cluster. Particularly problematic for training large models.

Important: this isn’t a pure lab solution. The technology is derived from EVIYOS, which has been running in production vehicles since 2023 and won the German Future Prize in 2024. The bottleneck isn’t the microLED itself, many players master GaN epitaxy, but the combination of high-frequency epitaxy (>1 GHz), monolithic microLED-CMOS integration, and automotive-qualified volume manufacturing, which means scalability and reliability are already proven. ams OSRAM also makes emitters and photodiodes in-house. MediaTek and Microsoft had to assemble their partners from different vendors.

Most importantly from a hyperscaler perspective: EVIYOS has been running in cars for three years. Automotive qualification is harder than any lab demo.

In large AI clusters, optical link failures are a real operational problem. Copper is more robust but limited to short distances. MicroLEDs address exactly this gap: greater reach at copper-like reliability and better energy profile.

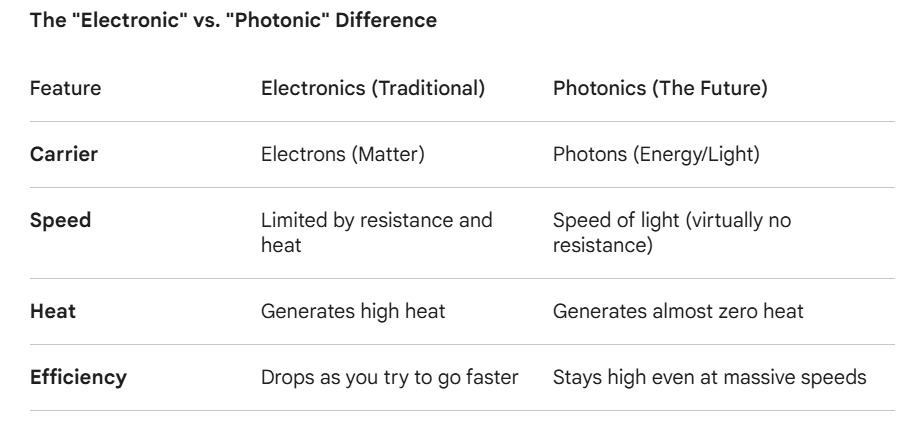

The efficiency advantage also comes from integration itself, precisely where CPO is struggling today with the extreme precision required, as I explained earlier this week: laser coupling and testing need sub-micrometer to micrometer precision. MicroLEDs as surface-emitting devices with a larger spot are mechanically far more forgiving, across hundreds of channels, that’s what decides the economics.

That said, this remains a long-term case. Broader adoption is realistic no earlier than 2029/2030, and the application is limited to short distances (intra-rack / rack-to-rack). For longer reaches, VCSEL and silicon photonics remain dominant – and continue to evolve.

ams OSRAM is addressing a real weakness in data center design with differentiated technology. But: it remains a niche for now. Anyone investing here is betting on optional upside, not near-term AI revenues.

The company is strong in its core markets and carries significant optionality. However, it also carries high debt. Apart from the debt load, the business is qualitatively well positioned. I don’t have complete research on the name. Anyone considering an investment should do their own research first.