Mark Taylor

232 posts

@tvmetguy Wait, am I stupid? Are you arguing this is bearish or bullish? 😂

That sounds like a super-bull argument to me. Is it possible we’re actually on the same side and I just misunderstood your tweet?

English

Therein lies possibly the biggest thread I've seen on $BETR. As soon as the market realizes output is up to a 7x earning multiple of software in on 10x TAM.

Palantir DoD software contract is at $2.28B rev 82% margin or $1.9B gross profit. But, Labor + Software ( output) is up to a 60% margin on 10x revenue.

It's like if Palantir had a $25B per annum DoD deal profiting $15B or 7x their current profits.

This is what happens when you not only optimize data analytics for decisioning, but also provide efficient expert labor.

Nobody at Palantir is jumping in a F-15.

From Q4 2025 CC

"It just depends on that, you know, what the revenue per loan is gonna be and what the margin is gonna be. As the revenue per loan kinda comes down, the margin actually expands because it becomes more and more where they're just using the platform. You know, the platform alone business can be 60% margin. You know, the D2C business, as you can see from a contribution margin perspective, is a 20%+ margin business on a contribution margin basis. You know, we're gonna get to know that and define that. We feel very confident in the guidance we're giving, and particularly the growth that we're manifesting."

@GrantCardone @jakebrowatzke @SidotiResearch

Vishal Garg@vishal_better

Totally true. Labor cost plus software cost in mortgage market is over $200bln per annum vs software alone which is $20bln per annum. There is no VC funded labor + software stack in the industry as engineers don’t want to get licensed as loan officers and underwriters and loan officers and underwriters are mostly trained on a system that has 85% market share built in the 90s that in 2026 permits only one person in the file at a time (those of you old enough to remember Sharepoint knows what that’s like). Therein lies the opportunity for @tinmanAI $betr

English

Ya mate, Im not mixing anything. Better supplies actual people to close loans or UW when needed in a layer. Output includes any work needed for the outcome. Its a much larger market than software alone. Some industries like mortgage are going to do better than others. Its a multiple of software here.

English

You’re mixing business model with economics. If $BETR software lets it process far more loans per employee, touching “labor” doesn’t make it less software-like. The real bear case is falling take rate or no operating leverage - not that it monetizes a bigger workflow.

If Palantir’s software could fly an F-15 better than a pilot, it would be worth more, not less.

English

@FelixKern2 @CedarStResearch @danielsethlewis @jakebrowatzke @mortgagetruth True, not needed, but true nonetheless!

English

English

@GrowthThesis Tis interesting nobody ever says no to my posts, its like they are insightful 😀

English

It'll allow for far larger share and profits is why. They have created 2 new channels. Mortgage in a box with Credit Karma using data in CK to make pre approved offers which Better closes. No upfront CAC. Volume can make CK the largest originator in the country due to their size. They are adding Sofi or someone like that to this channel now TBA. 30% margin is on 100s of thousands of annual loans. CK gets a small rev per loan (per the last call). Then platform as a service with ChatGPT. This is the up to 60% margin channel. Users, including the largest banks and LOs all over can use the platform immediately, no install and Training. The users get the majority of the revenue, but $BETR gets, from what I can tell, $2k to 3k per loan at 60% margin (per the last call). This new output as a service model brings 1500 to 2000 profit per loan, far higher than a software alone profit of about 400 per loan. So they are 5xing the profits by offering the UW and loan matching on top of the end to end software. Users have 0 cost, and get 5k or 6k per loan to pay their LO and profit. Banks today lose thousands per loan. This will take them into the black. Its $200b labor + software up for grabs. To give an example its like if Palantir not only did software for the Department of War but also supplied fighter pilots, and each pilot flew 10 planes at a time. It puts a multiple on Palantir biz model, for Better. A few million loans per year size here potential. Add in the Coinbase partner for down payment help and the Sky partnership coming to lower the offered rates to anyone by up to 1%, and you have the backbone of the mortgage industry formed by Better. Its just way more profitable this way. So 2030s can see 500k to 700k loans from CK and Sofi? And D2c plus Neo, and 1m+ output as a service loans a year. Take that for data lol. @jakebrowatzke @CedarStResearch

English

$BETR bulls

Can you help me understand why $BETR essentially rents out Tinman, their AI and rules based underwriter, to their competitors?

I may not be fully understanding the dynamic of it, but why not just maximize it yourself to take more market share over time?

English

Mark Taylor@tvmetguy

It'll allow for far larger share and profits is why. They have created 2 new channels. Mortgage in a box with Credit Karma using data in CK to make pre approved offers which Better closes. No upfront CAC. Volume can make CK the largest originator in the country due to their size. They are adding Sofi or someone like that to this channel now TBA. 30% margin is on 100s of thousands of annual loans. CK gets a small rev per loan (per the last call). Then platform as a service with ChatGPT. This is the up to 60% margin channel. Users, including the largest banks and LOs all over can use the platform immediately, no install and Training. The users get the majority of the revenue, but $BETR gets, from what I can tell, $2k to 3k per loan at 60% margin (per the last call). This new output as a service model brings 1500 to 2000 profit per loan, far higher than a software alone profit of about 400 per loan. So they are 5xing the profits by offering the UW and loan matching on top of the end to end software. Users have 0 cost, and get 5k or 6k per loan to pay their LO and profit. Banks today lose thousands per loan. This will take them into the black. Its $200b labor + software up for grabs. To give an example its like if Palantir not only did software for the Department of War but also supplied fighter pilots, and each pilot flew 10 planes at a time. It puts a multiple on Palantir biz model, for Better. A few million loans per year size here potential. Add in the Coinbase partner for down payment help and the Sky partnership coming to lower the offered rates to anyone by up to 1%, and you have the backbone of the mortgage industry formed by Better. Its just way more profitable this way. So 2030s can see 500k to 700k loans from CK and Sofi? And D2c plus Neo, and 1m+ output as a service loans a year. Take that for data lol. @jakebrowatzke @CedarStResearch

English

@GrantCardone Take a look at $BETR I outlined yesterday their $2b+ profit/year path

English

Prepare for avalanche of refinancing activity mid year. 10 year rates will fall below 3.5% once Trump ends Iran campaign. 30 yr rates will go to 4.5% before going lower end of year. Great time to be a mortgage broker & even better for real estate investors.

English

Wait til the market realizes this ChatGPT channel is 5x software total profits because they will get a 60% margin on the roughly $3000 in revenue they get per closed loan for labor + software rather than 80% of a $500 revenue per loan for software alone. And that it's a $200b market they are going for and they are the only 1. Dm me...@ericjackson this is how they get to a $200B MARKET CAP. What they are about to to is like Palantir for data but then also taking on the labor of the industry at high margin.

English

So this is like if Palantir supplied fighter pilots, missiles, and boots on the ground to the Department of War. Thats how you'd turn their 1b/year contract in to more of the 700b/year defense budget. Good to know $BETR can take banks from -5000 per loan to a 500 profit by handling almost all labor + software other than the sale. And that nobody else has this. I thought the software channel was about $2b up for grabs, was off by 100x per Vishal. @danielsethlewis @CedarStResearch @Mabiverse123 @mortgagetruth

Vishal Garg@vishal_better

Totally true. Labor cost plus software cost in mortgage market is over $200bln per annum vs software alone which is $20bln per annum. There is no VC funded labor + software stack in the industry as engineers don’t want to get licensed as loan officers and underwriters and loan officers and underwriters are mostly trained on a system that has 85% market share built in the 90s that in 2026 permits only one person in the file at a time (those of you old enough to remember Sharepoint knows what that’s like). Therein lies the opportunity for @tinmanAI $betr

English

This gets implemented second half of this year as relief for those who are signed up as partners. Will be interesting to see the actual results. Starting to hear rates may be high for years. But 6m loans will still occur this year and next anyway regardless because people have to live.

businesswire.com/news/home/2026…

English

This is the weekend when the real estate market gets interesting. Inventory begins a steady build from here through July...and many buyers out shopping who were pre-approved in January - early March, will begin experiencing the rate shock when they find a home.

Today, three calls went from all-in for writing an offer to complete hesitation. Why? For many, rates are 0.75% higher than this time last month. On a $600k home, that's almost $300 per month.

At a 6.50% rate, every $10k financed is $63/month. A $300 payment increase is roughly a $50k price reduction to achieve the same payment goal.

Fortunately, loan officers are numb to the discussions because we've had several of these shocks since 2022. It's now an every year occurance.

English

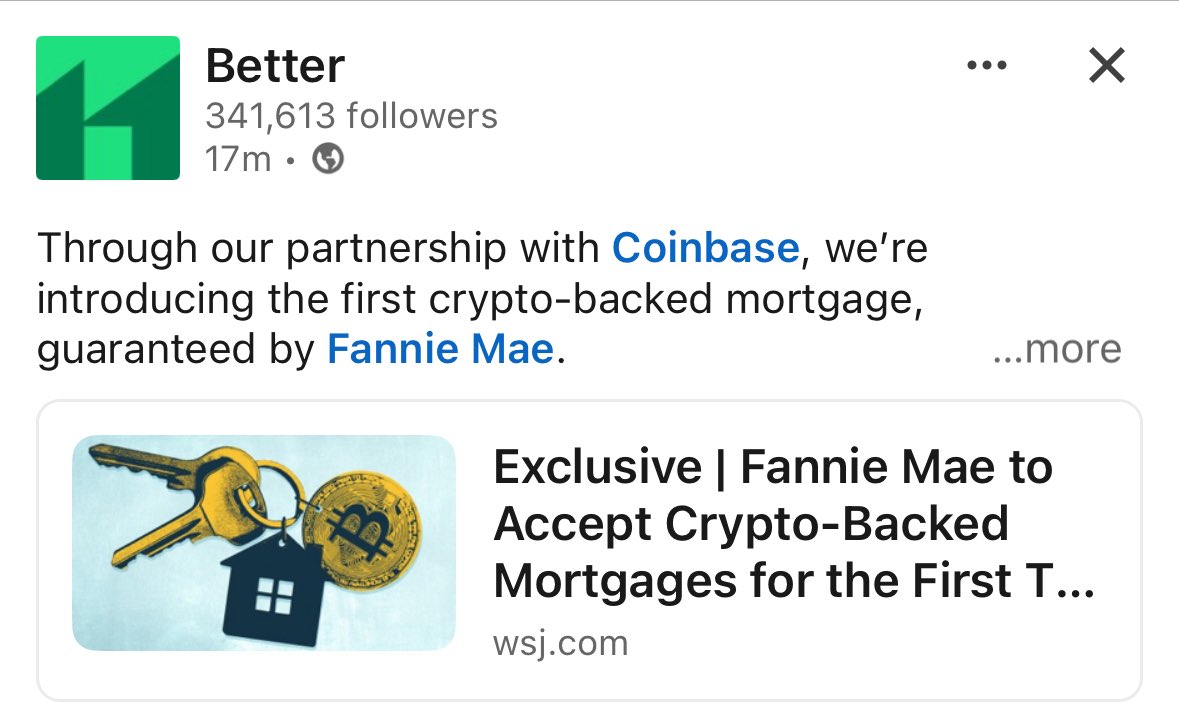

Any mortgage! So smart man! Coinbase one is like 10 bucks a month.

@mortgagetruth

All Coinbase One members who procure a token-backed or regular mortgage product through Better will be eligible for a rebate worth 1% of the mortgage value, capped at $10,000, to cover closing costs and fees. For example, a Coinbase One member securing a $800,000 mortgage through Better would be eligible to receive a $8,000 rebate.

English

I’m admittedly not a big crypto guy outside of Stablecoins, and I’ve held 1 BTC for sometime now, but the pace at which things are changing has been evident. $BETR

Store of value, any value etc… it’s sort of like the robinhood concept in a sense. If the next generation has these assets as a meaningful allocation, we should probably figure out a way to adopt them early in their LTV journey in order to service them for life.

English

Any mortgage! So smart man! Coinbase one is like 10 bucks a month.

@mortgagetruth

All Coinbase One members who procure a token-backed or regular mortgage product through Better will be eligible for a rebate worth 1% of the mortgage value, capped at $10,000, to cover closing costs and fees. For example, a Coinbase One member securing a $800,000 mortgage through Better would be eligible to receive a $8,000 rebate.

English

Any mortgage! So smart man! Coinbase one is like 10 bucks a month.

@mortgagetruth

All Coinbase One members who procure a token-backed or regular mortgage product through Better will be eligible for a rebate worth 1% of the mortgage value, capped at $10,000, to cover closing costs and fees. For example, a Coinbase One member securing a $800,000 mortgage through Better would be eligible to receive a $8,000 rebate.

English

Any mortgage! So smart man! Coinbase one is like 10 bucks a month.

@mortgagetruth

All Coinbase One members who procure a token-backed or regular mortgage product through Better will be eligible for a rebate worth 1% of the mortgage value, capped at $10,000, to cover closing costs and fees. For example, a Coinbase One member securing a $800,000 mortgage through Better would be eligible to receive a $8,000 rebate.

English

Any mortgage! So smart man! Coinbase one is like 10 bucks a month.

@mortgagetruth

All Coinbase One members who procure a token-backed or regular mortgage product through Better will be eligible for a rebate worth 1% of the mortgage value, capped at $10,000, to cover closing costs and fees. For example, a Coinbase One member securing a $800,000 mortgage through Better would be eligible to receive a $8,000 rebate.

English

Mark Taylor retweetledi

🎉 Better is proud to welcome Hugh Frater, former CEO of @FannieMae and founding partner of @BlackRock, to its Board of Directors.

Frater's decades of experience at the center of housing finance and global markets will help guide Better as we leverage AI to make the mortgage experience, faster, easier, and cheaper for Americans through the Tinman AI Platform. $BETR

Read more: businesswire.com/news/home/2026…

English

@CedarStResearch Is ChatGPT a software or origination sale for Better?

English

Listening to the $BETR Roth Conference was an interesting one for sure. Vishal has no problem telling you how he sees the market, even openly discussed how we’re likely headed towards a recession. The interesting take with this investment is his commentary on ability to process volume and how much volume the actual platform sees, the number might surprise some folks even if all deals are not actually cleared by mortgage brokers they all seem to certainly use it. Vishal goes into detail on the new partnerships and how explains the scaling laws of training loan officers (how GPT interface now ramps that up) and how fintechs move much faster all things considered on the integration and go to market side. Top 2 banks in the country reached out to $BETR after the GPT launch, not hard to guess who those are. Everyone seems to want to try Tinman and take him for a test ride. I “think” it’s the only end to end fully agentic system out there so props to team $BETR for building out the LLM over the ML base to get to where the tech stacks sits in the market today.

English