Sabitlenmiş Tweet

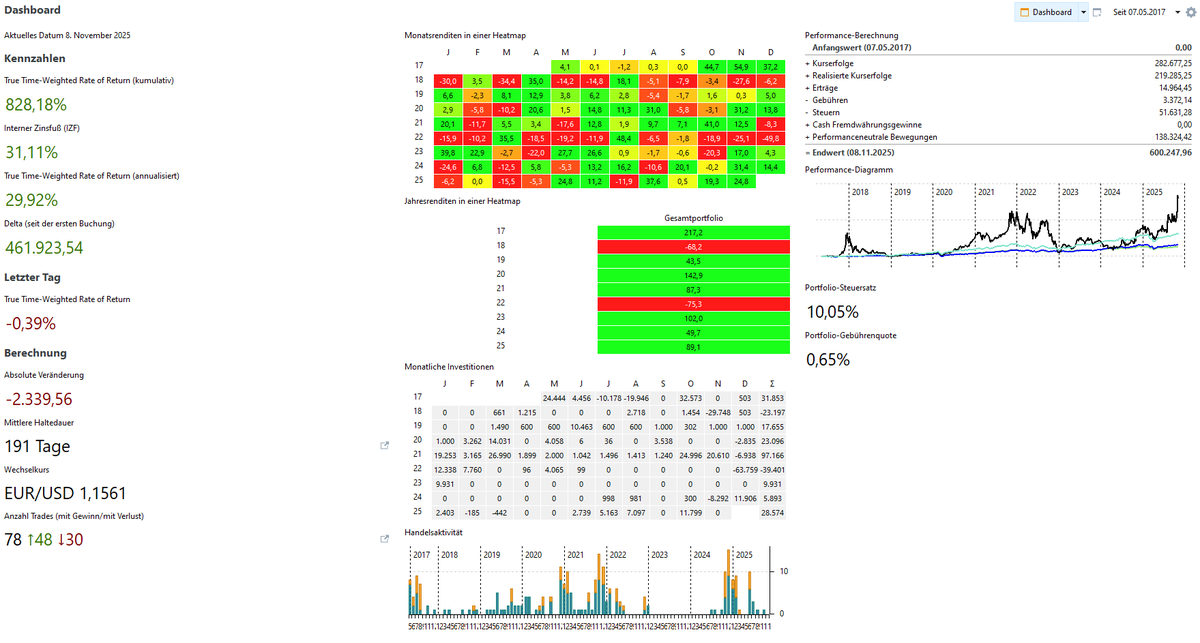

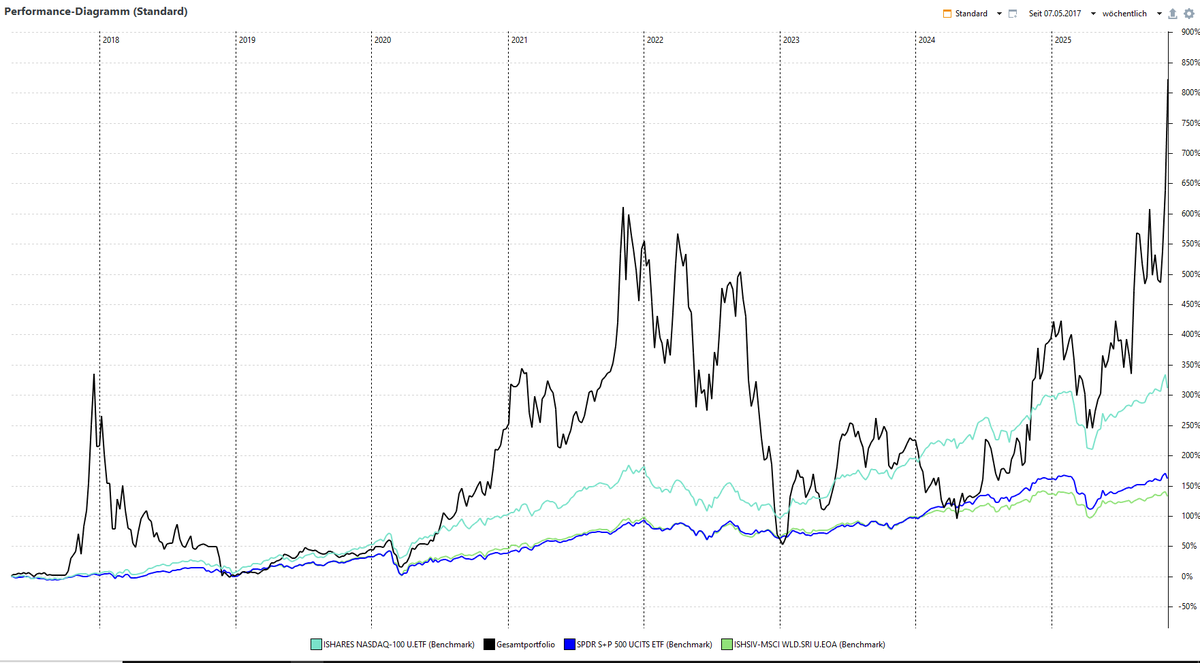

Portfolio-Update:

Mit 21 Jahren angefangen, heute 29 Jahre alt.

2017 - heute.

IRR: 31,11%

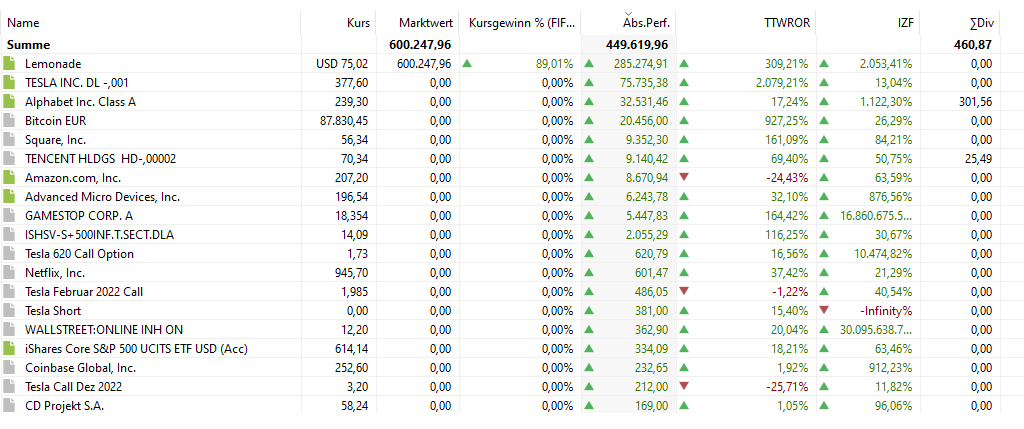

138.324,42 € investiert

461.923,54 € Gewinn (teilweise bereits versteuert)

600.247,96 € Depot

Größten Gewinner: $LMND $TLSA $GOOGL $BTC

Darstellung ist nicht 100% korrekt, zum 31.12.2025 werde ein paar Korrekturbuchungen vornehmen müssen, durch den Wechsel auf Interactive Brokers und den recht häufigen Verkauf von Optionen, ist es aktuell sehr schwierig dies in Portfolio Performance zu erfassen. IRR und Gesamtwert ist allerdings richtig.

Mein Portfolio besteht aktuell nicht aus 100% $LMND und die Aktienanzahl ist auch nicht richtig.

Ich habe durch Optionen aktuell auch noch ein Exposure in: $DUOL $META $NFLX $NVDA $PATH $ROOT $UBER $UPST

Bin gespannt wie es am Ende des Jahres aussieht und am 31.12.2026.

LG Felix

Deutsch