Volatile Value

243 posts

Volatile Value

@valueandvol

Family office advisor, investor. Completed CPA, CA, CFA designations. Opinions are my own and not the views of my employer.

Katılım Nisan 2012

944 Takip Edilen223 Takipçiler

Q1 letter is out ICYMI.

Also took the paywall down from my $FOUR post, for those interested.

poundtherockinvesting.substack.com/p/shift4-payme…

Adam Wilk@AKWilk

The Greystone Capital Q1 letter is now available on the site. I talk a bit about investing in this environment and discuss Secure $SES.TO and the $GFL deal. …4-4b58-95a2-873503998297.filesusr.com/ugd/47fd79_341…

English

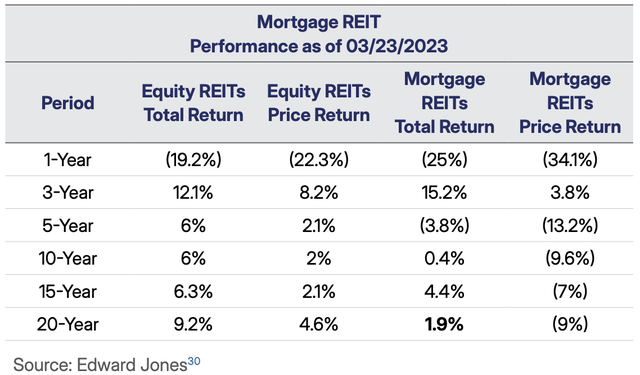

Mortgage REITs have performed very poorly over the past 20 years, despite offering high dividend yields. Do not fall for it! $NLY $AGNC $ABR

English

@JamesJstuartb Their own stock is trading at >5.5% implied cap

English

@JamesJstuartb I hear the concerns, but their own stock is trading at an implied cap rate. I agree on no more new acquisitions but think NCIB is appropriate versus pay down debt.

English

Would have preferred they keep the leverage ratio low and not take on debt. Not a fan of the idea

Vancouver Island Guy 🌊@VanIsleInvestor

$CAR.UN Canadian Apartment REIT - Investor Meeting

English

@JamesJstuartb Nice to see them supporting share price though and acting with conviction.

English

@BrownMarubozu Agree with that. I was saying your comment of giving employee cash and letting them decide when to buy is tough given the tax drag.

English

@valueandvol They are doing RSUs and options. What would you do instead?

English

I agree with John on paying employees cash and have them decide when to buy stock. $SCR.TO and $CSU.TO do it this way. $FFH.TO has a unique way of doing SBC. They have options and RSUs but they buy shares as SBC is issued and hold them in treasury until they vest.

John Huber@JohnHuber72

@dnbrwnjr @BenBajarin @kheksheyal I’d always prefer the alternative. Employees can always buy stock with their own money. SCR.to is a great example here. Pay employees in cash, some choose to buy shares but share count is unchanged. Regardless, paying employees in stock is a real expense

English

@BrownMarubozu Giving employees cash is the worst (54% tax). RSU is better (3 year vesting deferral) and options can be best if structured properly.

English

I looked back and ACFO payout ratio has never been this high, since 2017.

I want to like the name, but just shitty business when rents are capped on upside, you take all the downside in rent declines, and capex hard to control. But it is cheap.

English

$CAR.UN

I want to go long, but the cash flow pictures has looked worse than it has in many years.

We haven’t seen the benefits of capital recycling thru reduced capex yet.

English

@NelsonXLee @canada_spends Love the work Canada spends is doing.

English

Canadian Budget is out. Main Headline News 🧵

Deficit comes in $6B more than we predicted at @canada_spends at $78 Billion

English

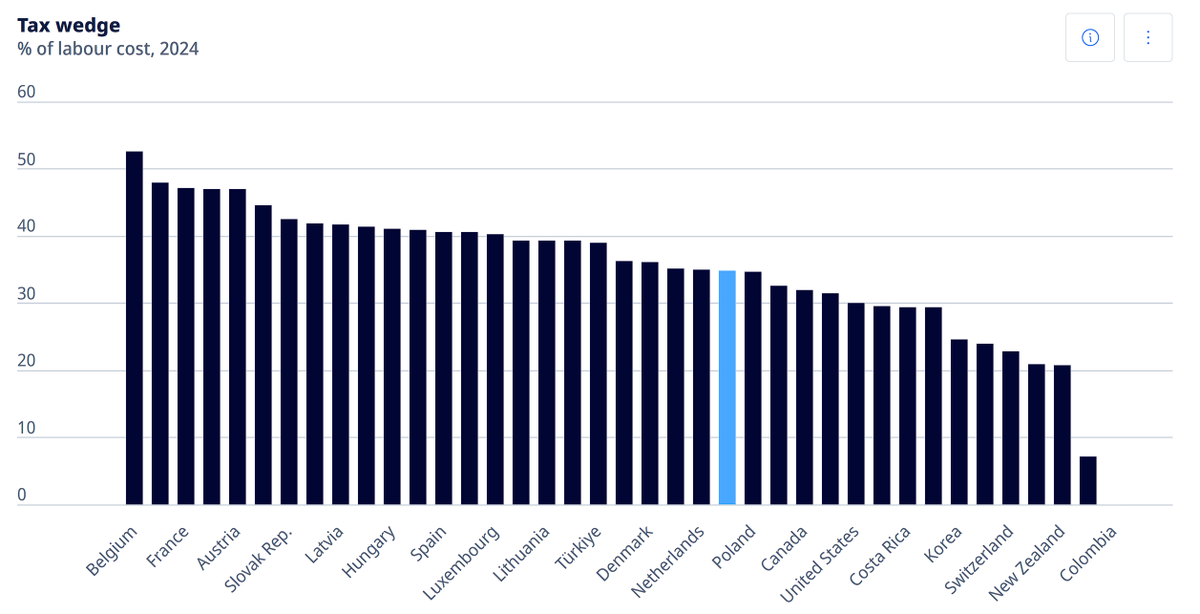

@valueandvol @NelsonXLee Huh, would you look at that--Canada has below average personal taxes.

English

My biggest insight (and double take) from today’s Budget:

A lot of the narrative about Canada’s tax rates being “uncompetitive” is just that… narrative. 🇨🇦

English

@NelsonXLee Fair.

But your caption says that Canada being uncompetitive on tax rates is “just narrative”.

Objectively, Canada is not competitive on taxes. That is fact. We can agree/disagree if that’s good or not, but let’s not twist the facts.

English

@NelsonXLee This is highly misleading. How much cherry picking required and creating new terms like METR to get the right graph.

Compare average tax burden for personal income, and for businesses - and let’s see how the graph looks.

English

@JulianKlymochko I think its low probability in buy-out, but definitely possible in venture. Overall, I'm with you that high quality BDCs are a good bet.

English

Cutting through the noise and negative sentiment on BDCs, here are some interesting insights from a recent call with leading BDCs and sell-side analyst:

- BDC sentiment completely disconnected from reality. 15-25% NAV discounts imply defaults that “far exceed” what happened in the GFC, with far lower implied recovery rates. Current discounts imply credit conditions unprecedented even in the worst recessions.

- Baby out with the bathwater dynamic, as idiosyncratic issues in BSL market has nothing to do with private credit. This has driven investor nervousness and a snowball effect from bad headlines.

- Narrative around death of software has reached fever pitch. However, fundamental performance across software lending book has been strong, revenue growth rates accelerating, currently around 10% and EBITDA growth higher.

- AFFE is a hurdle preventing many institutional investors from doing the work on the space, so trading can be inefficient.

- Historically, BDCs only traded under 80% of NAV (where they are now) for 8% of trading days, and NAV discount has always mean-reverted. Analyst thinks late Oct / early Nov Q3 reporting catalyst will prove out fundamentals that credit concerns and BDC prices aren’t realistic.

My thoughts are that current BDC prices imply roughly 20% of PE portfolio companies going bankrupt - effectively an extinction level event for private equity. I don't think this assumption is realistic.

English

@ArrakisGlobal @Bonhoeffer_KDS @pvtcreditguy @LeylaKuni OCSL has been a dog, and I'm down significantly also.

That being said, in 2021 NAV was $22 - down to $16.75 now. Decent margin of safety at $12 per share, but difficult to tell how deep the drawdown could go. May already be stabilized.

English

@Bonhoeffer_KDS @pvtcreditguy @LeylaKuni $ocsl has been total disaster 🤦🏻♂️

Poster child for how BDCs go wrong. Lost a decent amount in it

English

This is a good thread, and some interesting points about public/private credit.

Here's the POV from the seat of a retail investor (let's assume one that has access to both):

1. We don't know who the good managers are. Most of our wealth managers/RIAs don't know either. The sales brochures all look the same.

2. None of the financials filed with the SEC provide any detail into the granular level of the financial health of underlying borrowers.

3. There is absolutely no way to tell whether the diligence done by any given lender is better than that of another lender.

So let me ask you guys a question: who are the good stewards of money in the private credit space? And which asset managers are known for taking more risk than others?

High Yield Harry@HighyieldHarry

So this isn’t really First Brands specific - I just don’t think ppl outside of Credit fundamentally understand the diligence dynamics of Public Credit vs Private Credit. And that ppl will try to correlate the problem of poor managers to broader and systemic issues. Let’s dive into it. My ultimate view is the problems in Credit are with poor managers and those with risk-on mandates. The most important thing I can say is that you can’t define all lenders in the same bucket. Some groups are better educated, higher compensation, more diligent, have more thorough processes, have low risk parameters, and have competitive dynamics that give them higher quality deals. Meanwhile some firms have lower comp, a less experienced team, quicker processes, higher risk parameters to deploy quality, a willingness to focus on relationships over deal quality, or because of where they sit in the market they have to take on lower quality deals. Credit Suisse in particular, was a high risk culture and long before its eventual demise there were a lot of questions about what it was financing and the quality of the deals it was agent on or heavily exposed to. But just because Credit Suisse is Credit Suisse, it doesn’t mean JP Morgan is Credit Suisse. Jefferies has also fallen into the bucket of generally being pretty risk on, which has helped them in a lot of instances, obviously not here. So i’m not a believer in ‘private equity is a bubble” or “private credit is a bubble” and instead of you need to more so call out the firms that aren’t performing - they have to do continuation funds because they can’t fundraise, their deals are constantly going through LMEs, etc. Let me go through how i view diligence in Public Credit and Private Credit. Unfortunately, asset-based finance isn’t really where I spent my time, but I can opine a little there. I just think it’s important to distinguish where the risks could be and what could generally be fine.

English