Someone

42 posts

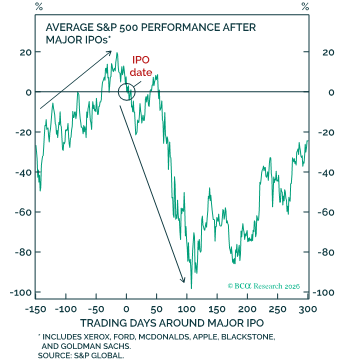

It's tough to throw me off my current bullish bias, even with Hormuz still closed. But a Monster IPO might do the trick. Beware the coming IPO-Palooza.

English

@why_a_pseudonym Please view our boarding process here: bit.ly/3FLU2Aq.

English

@DanielSLoeb1 Weird framing on her part. Isn’t the counter factual that those people are subsidizing the city by not burdening the municipality by using the services those tax payments provide?

English

@pnlcorrect Seems like this has some wisdom to it. Care to elaborate?

English

@mattyglesias Evil is a pretty strong word to describe something where the intention is positive. Stupid perhaps, but I generally don’t think advising people to use something sparingly because of potential side effects is a bad thing. It would be great to occasionally read a balanced take.

English

@JulianMI2 @JulietteJDI While I agree with your view, I think it’s a bit disingenuous to not break out return attribution by fx vs equities. Professionals would hedge or express via futures. For retail, I think it’s objectively bad advice to tell them to take a massive punt on fx.

English

We are bombarded by "S&P at new highs". But it's MONEY ILLUSION. By staying in US stocks, you are getting relatively poorer. Yes, in $ terms, the S&P is up 5% YTD, but flat in foreign currencies. As a US investor, you'd be up 20% in European stocks. This is why FX is key!

English

@DannyDayan5 @dampedspring Pretty sure that’s the point of gold/cmds being in it. Unless you think global cb’s shock tighten and improve the prospects for cash, I’d take some rpar over none

English

@dampedspring None. Absolute return only.

Gold has saved it from being even worse but the entire strategy depends on a correlation that is no longer reliable btwn stocks and bonds and also depends on a consistently low vol regime. Violent but fleeting vol shocks pretty bad for RP.

English

@AahanPrometheus None of these have outperformed ytd though. Maybe they will on a forward looking basis but simply looking at TY, IK, RX, and OAT futures reveals that. I’m unfamiliar with BWX

English

@why_a_pseudonym OATS, BUNDS, BTPS, FX hedged. Or even just look at BWX vs us treausies

English

The Big Picture For US Bonds 🌍

Often on this platform, I post short, one-line positions— usually a reflection of our Prometheus Institutional positioning. One of the things that I’ve posted frequently is:

Global Bonds > US Bonds

1/ Details on what’s driving this view…

English

@AahanPrometheus Which bonds are you alluding to? Not sure the YTD takeaway is that long RoW vs USA has been good

English

19/ Thanks for getting to the end.

The best way to leverage this account is to let me know topics you want to hear about.

Macro, process, strategies— anything goes. If I feel I have insight, I’ll share my thinking in a thread. Lmk below 👇

English

@bespokeinvest If you correlate two lines that start on the lower left and end on the upper right, regardless of their daily variance, they will demonstrate high correlations. There is no relationship between these charts other than that.

English

@BobEUnlimited Your view has shifted this firmly on 50bps of low multiplier fiscal that hasn’t passed the house yet?

English

If your favorite Fintwit personality was bullish the US economy before last weekend's shift, political preferences are clouding their views.

Same if they didn't shift more positive on the economy afterward.

And if they say they perfectly predicted this path, they are full of it

English

In a policy induced recession, you must trade policy, not data. A whole lotta nerds are about to get pwned.

English

@BickerinBrattle You’re the Yogi Berra of fintwit. Probably wise but I’m like 60% sure about what you’re trying to convey

English

Losing money today. Another factor entering risk appraisal and that is Trump is crazed. George III loon. Carney came in and held his tongue learning from Zelenskyy. Courts moving in step by step with Supreme Court cultivating iron clad "percolation".

English

@andresdrobny Right, tough call but if we had a vat tax of 20-30%, I’d like to think the fed would cut rates. Maybe that’s too optimistic given the political climate though

English

@why_a_pseudonym Makes sense. The similarity to 70s is the supply shock. Raises the question of appropriate FED response, esp with $ tide shifting.

The nature of the Supshock is also different. Then it was oil. Now it captures many more products, and various production inputs.

English

If they succeed, what happens to global capital accounts? Fewer $ imports, fewer $ reserves needed.

Europe rearms, and China consumes. More capital absorbed at home; less flow to US.

Interest rates? Not sure. Likely depends on inflation. So far, 1970s pattern persists….1/

BisphamGreen@BisphamGreen

BESSENT: REBALANCING OF CHINA ECONOMY TOWARDS CONSUMPTION ND U.S. ECONOMY TOWARDS MANUFACTURING IN TWO TO THREE DECADES WOULD BE A 'HUGE WIN' -JP MORGAN SESSION

English

@andresdrobny In summary, I think your sudden stop idea is right. I think demand destruction is inevitable with things as is and inflation won’t be an issue unless something changes behaviorally wrt borrowing

English

@andresdrobny Market expectations aside, I’m talking about the behavior of hh. We aren’t observing credit upticks in spite of that cut expectation. The free lunch was borrowing at deeply negative reals. at present that is not the behavior, arguing against the historical analog for a normal Rec

English

@andresdrobny And yes, I think that’s the counter argument to resurgence of inflation. I’d also argue that’s why (over politics even though it makes for a better story) the fed has been uniformly hawkish since April 2: to keep rates & financial conditions tight to not have a demand impulse

English

@andresdrobny I’m open minded about it but if you read accounts of the 70s, the mindset was that borrowing was an arb. If you look at hh credit creation, you had big surges in each wave. Presently, we’re flat lining at best. I’d argue that people don’t view houses, cars, goods a no brainer buy

English