@ryanlpeterman Thank you for the interview. It would be great if you could also bring Al Vermeulen out of retirement. I’m a big fan of his work within Amazon and hope it becomes more widely recognized across the industry.

English

Canh Nguyen

123 posts

software engineering in one paragraph

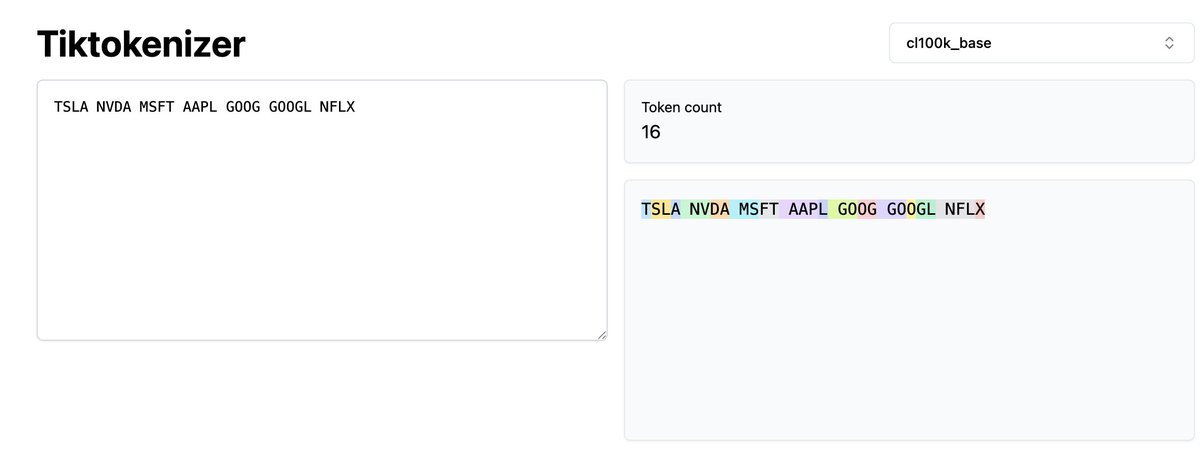

Amazon laid off 30,000 employees today, an even larger cut than during the industry contraction in 2022. The reason is simple: They don’t have enough capex left to buy GPUs. As a result, AWS growth has slowed, the market has punished them harshly, and now they must cut salaries to save money for GPU purchases—so the financials look better and they can tell a story of “AWS growth bottoming out.” Every internet company software engineer (SDE) should buy Nvidia/AMD stock as a hedge—compensating for the risk of being squeezed out of the value chain by GPUs. Entering 2024–2025, the main factor behind weak employment for American SDEs is no longer the massive over-expansion of 2021, nor the competition from lower-wage overseas engineering centers, and not yet the reduced demand caused by AI efficiency gains. A new boss has arrived: GPU capex. GPU capex is creating a strange “prosperous depression” inside internet companies: The company’s revenue growth looks strong, stock prices keep rising—but wage expenses have become immovable constraints for management. Everyone worries about their jobs. Continuous layoffs increase the workload for those who remain. Morale collapses. It feels like the Great Depression all over again. This isn’t a traditional recession. It’s capital’s radical redistribution between manpower and compute power. Amazon’s 30,000-person layoff has been rumored for two months. The mid-year performance review, usually in July, was delayed to mid- or late August. The return-to-office (RTO) policy also served as a major excuse for the cuts. The AGI group will remain untouched; PXT, Devices & Services, and Operations will be the hardest hit. By convention, AWS will likely announce its cuts later—probably after AWS re:Invent—to squeeze every bit of output first. Meanwhile, AWS’s Q2 backlog reached $195 billion, up 25% YoY. This shows customers want to buy but AWS can’t deliver—demand remains scorching hot, and they simply can’t buy GPUs fast enough. In an era where AI server supply can’t keep up with explosive demand, shifting opex (wages) to capex directly boosts company performance. Capital will ruthlessly punish any CSP or hyperscaler that fails to fully embrace this path. Meta has quietly entered a “5% layoff every six months” rhythm. Recently, it cut 600 people in its AI org and also removed many directors across departments—same logic again: AI datacenter capacity is insufficient. In the past year, Meta revised up its 18-month capacity plan three times. Each time they thought they had overestimated demand—only to painfully realize a few months later that they had underestimated it. Does this mean internet companies no longer need people? Of course not. But after the hiring budget is slashed, they’re forced to squeeze productivity internally to compensate. Big tech companies are now pulling every possible lever: building internal tools with agent functions, encouraging “one-click deployment vibes,” setting KPIs for AI usage rates, requiring departments to report AI adoption progress and use cases, and mandating periodic peer learning sessions. All these frantic moves aim for just one modest goal: ~20% efficiency improvement. What happens next? To maintain growth and competitiveness—once efficiency gains plateau and layoffs hit the bone, when opex yields no more savings—the next step will be to sacrifice cash flow. Some, like Oracle, may even take on debt to sustain growth. Nvidia and AMD, armed with huge cash reserves, will continue to push partners to invest in AI capex—just like OpenAI has done. The biggest beneficiaries of all this will be the semiconductor supply chain. A new normal may emerge: semiconductor companies’ profit margins surpass those of internet firms. But they also bear the greatest risk: Once VCs or hyperscalers notice token demand slowing—or even just growth decelerating—they’ll ruthlessly cut orders. The transmission of that shock will be far faster than semiconductor production cycles. When might that point arrive? One reference indicator: when enterprise adoption reaches ~50%. During the March 2000 internet bubble burst, U.S. internet penetration was around 52% (some data say 43%). Currently, major internet companies’ GenAI daily-user penetration is rising from 50% toward 90%, while overall enterprise AI adoption is still under 10%. That means growth is safe for now. Historically, the fastest phase of any technological revolution is when corporate adoption moves from 10% to 50%. The Cisco bubble won’t repeat itself so simply. This time, information flow is vastly richer. There will always be enough skeptics warning about bubbles—ensuring that when it does burst, it won’t be nearly as catastrophic.

While there’s no way to know ahead of time what the right architecture is (you have to discover it) there are many wrong architectures that you should avoid. “Microservice Architecture” is just the wrong architecture for any kind of problem. Period. Never even consider it.

Opinionated people on social media fall into five categories: Principled-Brave: Say what they think regardless of what's popular Principled-Timid: Say what they think when it's safe to do so Bandwagoner: Say whatever's popular Principled-Contrarian: Say what they think when others aren't saying it Contrarian As a Principle: Go against whatever's popular