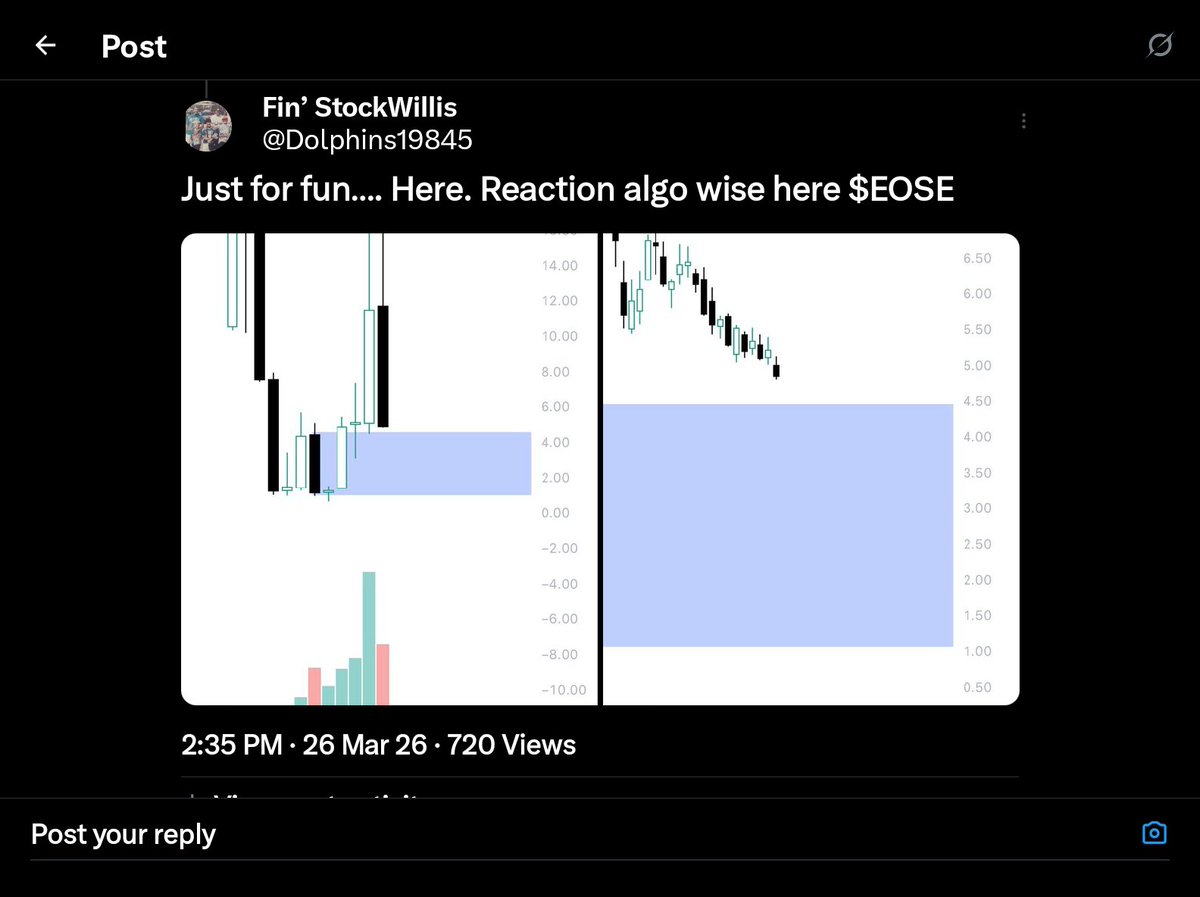

@FreemyerGreg @OBGInvestments @TeslaJLP Is there any way it could be 1.9M worth of material being reported (COGS) and not ASP worth? If that was the case, I think that would be a lot more than 10 cubes

English

AdventitiousDrummer

969 posts

@Maxonation

Follower ✞, Investor, Drummer & Software Dev Grid Scale storage $EOSE - Next Gen Batteries $ENVX

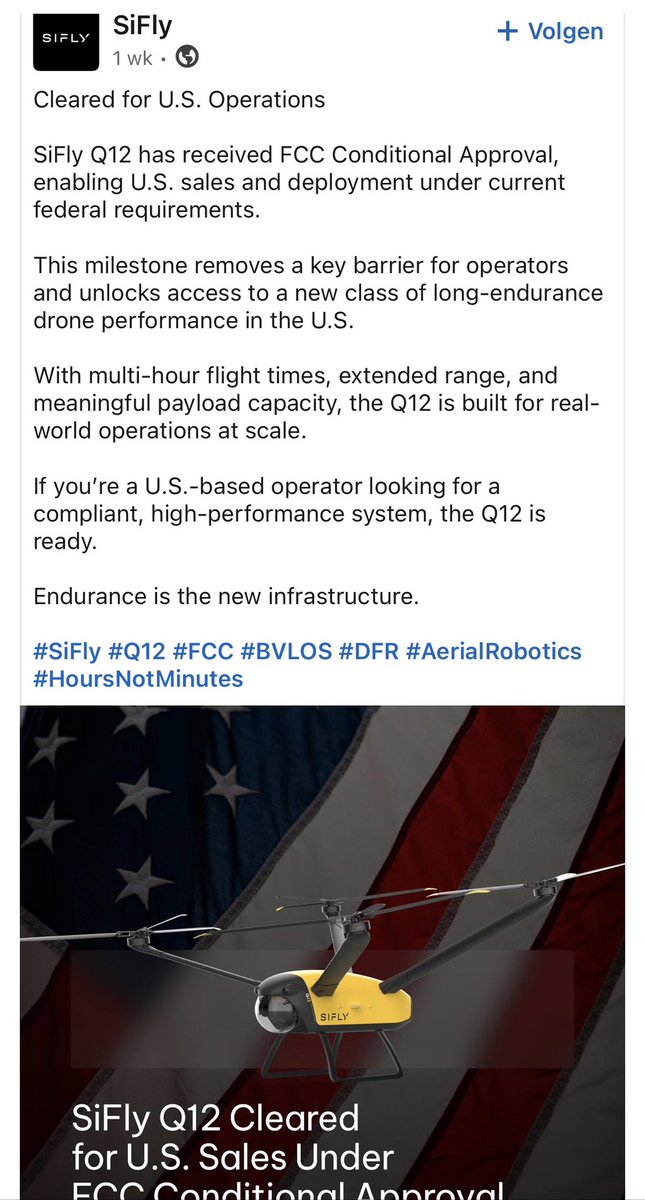

1/2 $ENVX 🕹️ SiFly : "A new drone company based in California has exploded out of stealth mode with incredible claims about its first product, saying it'll fly 4X longer, 10X further, 10X quieter and carry 5X more payload than leading competitors – while competing with China on cost." Contrary to what is said in the comments, these drones are "fully electric and autonomous" (see sifly.co), which implies that advanced battery technology is used. newatlas.com/drones/sifly-q…