daando37

4.3K posts

daando37

@daando37

side quest. always dyor. all my takes are no financial advices.

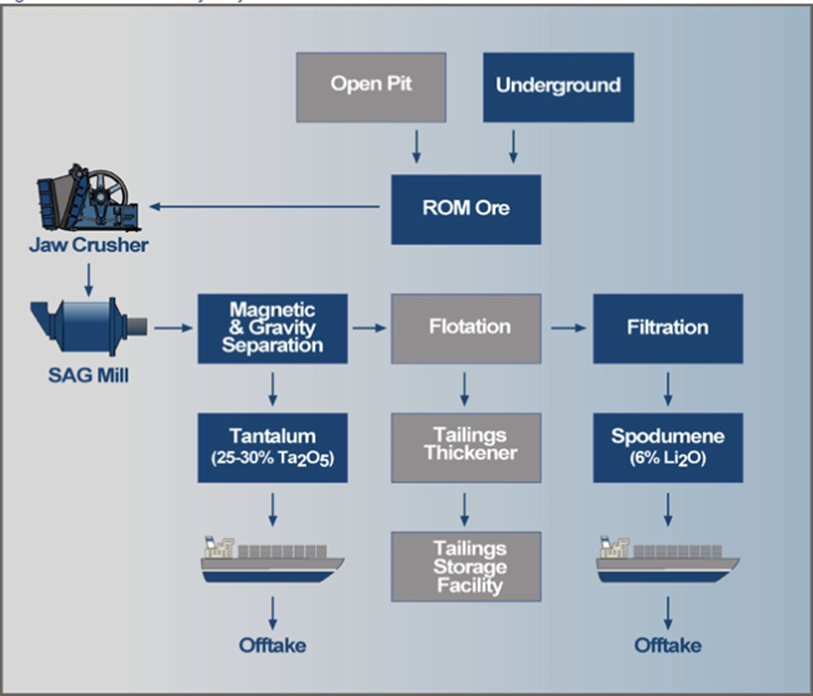

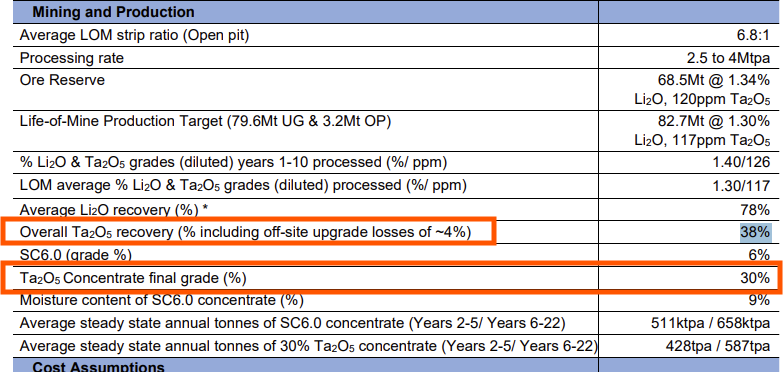

Some random thoughts on the hard rock pegmatites as I sip my morning coffee. Nobody seems to be talking about the price of Tantalum which has just reached its highest price in 20 years. A lot of hard rock lithium companies produce Tantalum as a by-product. It’s a relatively rare metal that occurs in small quantities in pegmatites. Most deposits have an average grade of around ~130ppm Ta. It’s quite easy to concentrate given just how heavy it is compared to spodumene and the typical pegmatite associated deleterious elements. Tantalite a specific gravity of ~8 whereas spodumene comes in at ~3.1. However, its worth noting, like all metals and minerals, some deposits will have higher recovery rates and better metallurgy than others. As you can see on the diagram below, given just how heavy it is, and also that it generally contains iron, it can be removed before the flotation step with gravity and magnetic separation. The recoveries are generally quite low (I note LTR’s came in at 38% in their DFS - not sure what they are in operation). Whilst it’s low, it’s not bad for a by-product and such a simple and relatively low cost process (magnetic and gravity separation after SAG). I’d imagine it would be relatively straight forward to increase the recovery rates. For example the grind size is optimised to suit the spodumene as it’s the main game. If the tantalum price increases enough I’m wondering if there’s a sweet spot where you’d ideally tweak the grind to suit the tantalum recoveries a bit. Although I’m not sure what tantalum price you’d need to warrant that. Companies generally list it as a credit against the operating costs. In LTR’s DFS for example, they were estimating a US$48 credit per tonne thanks to tantalum concentrate sales. Which equates to a tantalum price somewhere around the ~US$84/lb CIF China mark. The current price of >30% Ta2O5 concentrate is $US260/lb (this is per contained Ta2O5). So to run through an example, last half yearly, LTR produced around 591dmt of Tantalum concentrate, which equates to 1,302,930 pounds. However, this would come out as a 12% graded product as stated in their DFS and is further upgraded offsite for a 4% loss. So total contained Ta2O5 would be 1,302,930 * 12% * (0.96) = 150,098 lbs of Ta2O5 per half year. So if you crunch the math, 150,098 x ~$US230(rough realised price) x 1.43(US to AUD) x 2 = ~$A98.7 million annually. It starts to become quite a significant credit, especially if you take into account the simplicity of concentrating it. I'm not sure of the offsite concentrating costs and its not listed anywhere. I'd imagine its still largely magnetic and gravity based so shouldn't be overly high relatively speaking compared to other processes. If the price of Tantalum continues to increase, you would think companies would start to implement/tweak processing to increase recoveries given how low they are. 38% is quite low if you ask me (using LTR as an example) and I'm sure there would be ways to increase this without hurting the spodumene output. Just a benefit hard rock mining has over brines! Maybe some of the smaller lithium players could look to implement a small scale WHIMS, etc. and start concentrating tantalum to raise early stage cash? If the price of spodumene holds above US$2000, and you throw in a juicy tantalum credit, you’re going to see some pretty decent quarters for lithium producers I'd say! Thanks for reading!

As many of you know, Canada has the fourth-largest proven oil reserves in the world, representing 10 percent of global reserves. Over 97 percent of that is in Alberta’s prolific oil sands. We also have four significant producing oil fields off the coast of Newfoundland, with another, Bay du Nord expected to come online by 2031, adding an additional one billion barrels of recoverable reserves. We are the world’s fifth-largest natural gas producer, and we have nearly 1,368 trillion cubic feet of marketable natural gas reserves, which could last 200 years at the current rate of production. We are also a Tier 1 nuclear nation; a leader in CCUS; and the fourth-largest producer of renewable electricity in the world. So when it comes to conversations about the future of energy for North America and the world, let me be very clear: Canada intends to play a constructive role in delivering affordable, reliable and secure energy for Canadians, Americans and all our allies.

🚨Q2 Metals Announces Multiple 200+ Metre Intervals of Continuous Spodumene Pegmatite and Provides an Update on the Inaugural Mineral Resource Estimate at the Cisco Lithium Project, Quebec, Canada $QTWO $QTWO.V $QUEXF Read the full press release 👇: q2metals.com/news/q2-metals…

1/ $ake olaroz has an annual #lithium carbonate production target of 17,500tpa. theoretically they would have to produce 4,375t every quarter (5,059t last quarter). in the past reporting fy23 they produced 16,703t of carbonate. they started in the second quarter of 2015 with 126t

lithium argentina finally looks less like a concept & more like a company. that's a meaningful shift.

Lithium Argentina delivered a record fourth quarter, capping a year defined by operational execution and cost discipline. ✔️ Q4 production reaching 97% ✔️ Q4 costs ~$5,600, ✔️ Advanced key growth milestones With a strong operating foundation, competitive cost position and improving market conditions, we are well positioned for our next phase of growth. Read the full release here: investors.lithium-argentina.com/news-releases/…

Fertilizer prices have moved up to their highest levels since September 2022, rising 44% YoY. About a third of global fertilizer supply passes through the Strait of Hormuz. This will drive food price inflation higher in the coming weeks/months. Video: youtube.com/watch?v=L3o7T1…

can't explain the unpopularity of an entire sector that literally prints money. $whc $whc.ax #coal

MOST ACTIVE CHINA COKING COAL CONTRACT RISES 9.68% TO 1,274.5 YUAN/METRIC TON

Compelling slide from $NHC highlights the onset of a structural thermal coal supply shortfall.. ESG-driven regulatory hurdles severely limit new projects, while global demand expands robustly against consensus, creating a highly favourable setup.. IMO the energy complex remains misunderstood: focus not on shifting source percentages, but on the rapid expansion of the overall global energy pie (see quoted post).. geopolitical pressures like the US-Israel-Iran conflict add near-term strain, yet the dynamic is fundamentally structural and accelerating.. Established producers with proven reserves and operational strengths stand to benefit disproportionately, especially given the inherent valuation discounts the coalies typically trade on.. $YAL.AX $WHC.AX $NHC.AX $TER.AX $CNR $BTU #coaltwitter

One nuclear reactor. 1.9 million solar panels. Same capacity, but nuclear runs 24/7 regardless of weather. I'll take boring and reliable over expensive and intermittent any day.

same barrel. different tax stack. different pain threshold. at $194-276 brent, germany isn't dealing w/ an oil move. it's dealing w/ a consumer squeeze that turns political fast. the uk gets squeezed hard. the us still feels it, but from a much lower all-in base.

SPAIN TO REDUCE VAT ON FUEL TO 10% FROM CURRENT 21% TO MITIGATE IRAN WAR IMPACT, SER RADIO REPORTS

brent futures can sit around $107-113/bbl & still tell you almost nothing about how savage the end user shock will be. 'cause crude is just the entry ticket. once that barrel moves through real economies, the pain gets repriced country by country. at the pump, the same barrel equivalent is already closer to $372 in germany, $286 in the uk, ~$191 in japan & india, $189 in china & $140 in the us. same oil. very different trauma. so in a real disruption, you don't just get a higher chart on a terminal. you get asymmetric economic stress. high tax/import dependent systems get punished first. consumers feel it faster. politicians panic sooner. demand destruction starts earlier. that's the part people keep glossing over. oil shocks are never just about the futures screen. they're about who has the weakest downstream tolerance once crude starts climbing. & on that front, some countries are walking into the storm wearing body armor. others are walking in wearing a receipt.