@tomzhu_nz Just imagine, how much more demand would be generated with just a tiny AWARENESS CAMPAIGN aside of X 🫨 Billions of people still have wrongful perceptions of the EV

English

Viktor Ianushenko 🇺🇦

1.4K posts

Model Y was the best selling vehicle of any kind in Australia for the month of May Making it the first electric car in history to lead the overall AU sales charts across all fuel types

When to buy:

$TE ripping after Leopold Aschenbrenner`s 13F

Just in case you hate Gann, what do the bears have to say about this bullish backtest of the 20-month SMA? $TSLA x.com/matthughes13/s…

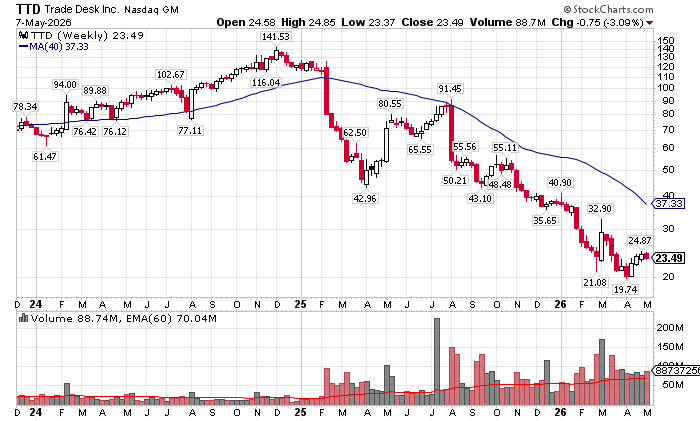

I have sold my shares in $TTD (in the spec account) ahead of earnings today for a long term capital gain (cost basis was $77.76 from October 2023). Sold $131.33 for a 69% gain.

Tesla shareholders funded the robotaxi vision through the hard part. The missed timelines, ridicule, drawdowns, and the “FSD is impossible” years. So if Tesla ever gets folded into SpaceX, the question isn’t “would that be cool?” It’s: who gets paid for the robotaxi value? Bradford breaks it down here.👇