Be

225 posts

$AXON very strong Q1:

• Revenue: $807M vs Est. $779M

• EPS $1.61 vs Est. $1.60

• Net Retention 125%

2026 outlook:

• Revenue growth 30-32%, Capex $160-$190M

• Future contracted bookings +44%

English

@InvestingVisual I do not mind this weakness if it is temporary because of the shift on strategy to reach their 2028 DAU goal. my issue if this is permanent. what do you think?

English

Booking are looking really ugly here. Growth already dropped significantly but guiding for just 10% bookings growth means a slowdown from >30% to 10% in just a few quarter.

Not good.

English

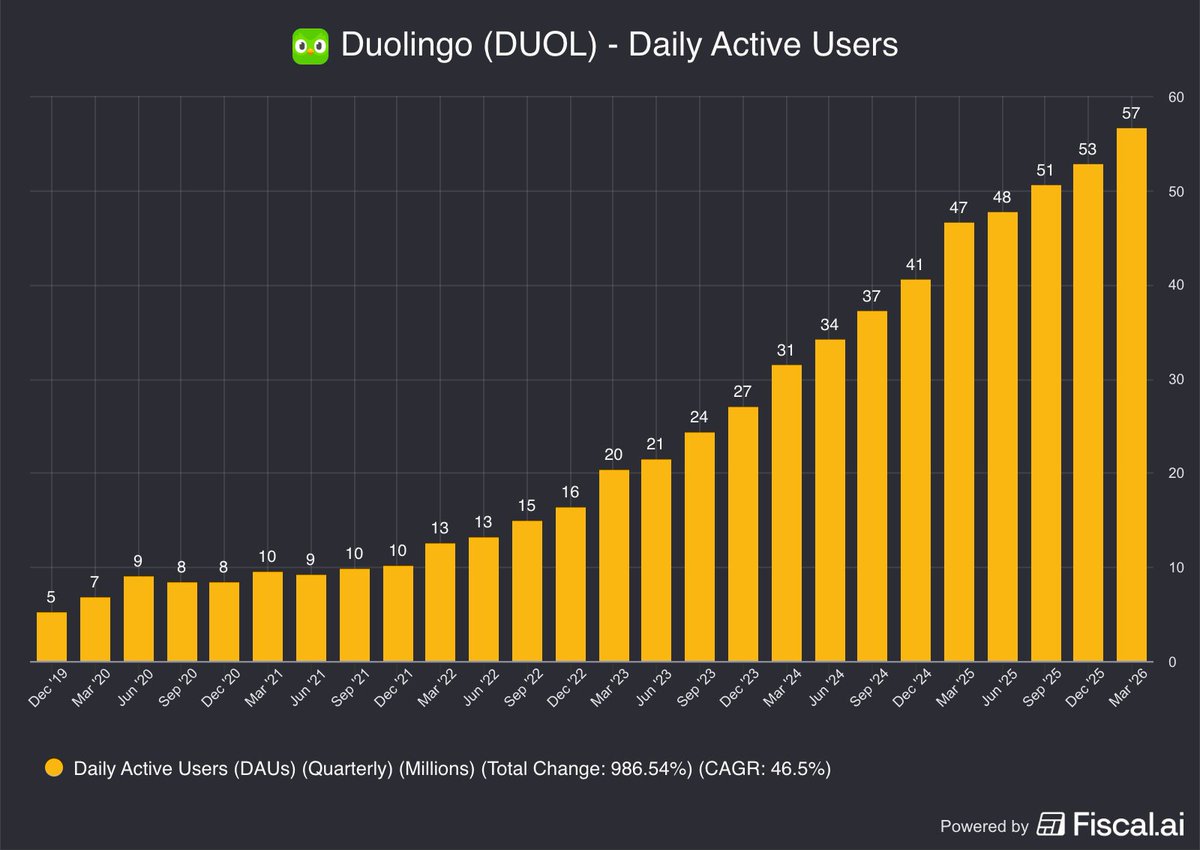

$DUOL Q1 2026 earnings:

• Revenue: $292.0M vs Est. $289M

• EPS: $0.89 vs Est. $0.75

• DAUs: 56.5M (+21% YoY)

• Total Bookings: $308.5M (+14% YoY)

FY Guide:

• Revenue: $1,205M; +16.1% YoY

• Bookings: $1,280M; +10.5% YoY

English

$DUOL: market reaction sucks, but thesis unchanged.

Generative AI is clearly accelerating the business and only widening the data / AI workflow moat.

(Not investment advice.)

Dr. Tomislav Marinovic@DrTomsLens

$DUOL CEO Luis von Ahn, on scaling learning content: “We’ve now launched content up to Duolingo Score 129 (CEFR B2) across courses teaching our 9 most-learned languages, so learners can use Duolingo to reach professional proficiency. Given the number of language combinations we teach, expanding to this level required building an enormous amount of content. In Q1 2026 alone, we published 20,500 course units across our language courses, up from 7,100 per quarter in 2025 and 1,800 per quarter in 2024. Automating more of our content creation process also lets us iterate in ways that were not possible before. We can now push changes across many courses at once and improve quality more quickly and consistently. This is already improving engagement among new users.” Generative AI is accelerating $DUOL. Content creation and iteration are going vertical. This might take a few quarters to fully kick in, but over time it should translate into better teaching, stronger user growth, and eventually monetization. (Not investment advice.)

English

@shey2007shey Btw. I sold all my shares around $9. Not bad for an avg cost of $1.3. I sold because i do not believe in the new CEO. Something is off about him.

English

@shey2007shey I’ve been accumulating since 2020😅. Over 60k shares now. Let’s hope we are right on our bet.

English

Fed cut rates by 50 bps, first reduction since 2020. Two more 25 bps cuts are expected soon.The Fed is confident inflation is approaching 2% and projects 100 bps cuts in 2025 and 50 bps in 2026. If by 2026, $OPEN reaches $12 it could yield a 5x return for long-term holders $open

English

Good thoughts on $LMND SBC. I think the SBC is one of the biggest concerns on investors minds after Q1. I’ll be looking into it in more detail.

Andreas Schulz@ASchulz888

I do have some thoughts on SBC as well. There were some special circumstances this Q, as you point out. And there was the recent expiry of the 2021 incentive plan (granted near the all-time peak), which removed a lot of upside optionality for management. The board may have felt compelled to do something to offset that impact. Also I feel that the senior leadership team is doing a hell of a job and deserve to get paid. It is also worth pointing out that $LMND has continued to leverage SBC (i.e. SBC / revenues has been on a steady downward trend). So as long as SBC continues to scale like opex and not like revenues I don't think there is a problem long-term. In my mind, the main problem here was one of optics. In an environment where investors are asking a lot more questions about SBC their guidance for a higher run rate of SBC invites questions like the ones I was responding to. If $LMND wanted to put these questions to rest permanently they could do what some other companies have done and set clearer targets around continued SBC leverage. But that is up to them. And to reiterate, in substance I don't think there is a problem here.

English

English

Lemonade’s Q1 results are 🔥. So much to share, where do I start?

First, get into the AI mood, click this, + volume ⏫

open.spotify.com/track/20HCH8XT… (by @kidfrancescoli)

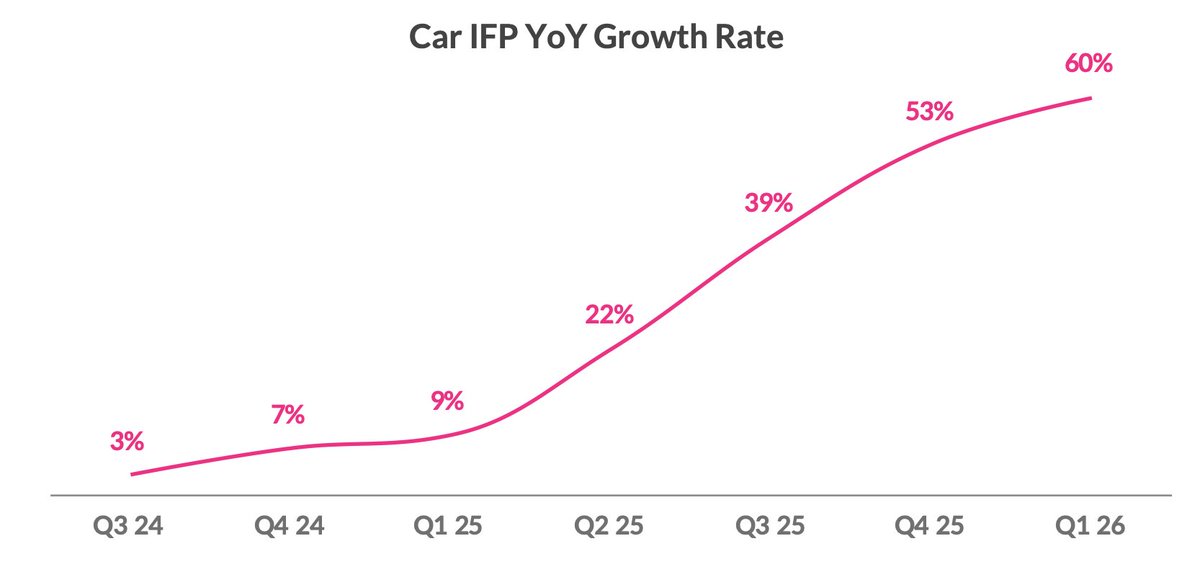

🚀10th consecutive quarter of accelerating IFP growth

🔥 Topline at $1.33 Billion (IFP +32%)

🔥 Revenue grew 71% to $258M

🔥 Gross Profit increased 159% to $100M

🔥 3.14M Customers

🔥 Adj. Free Cash Flow $17M

Lemonade Pet exploding!

✅ Surpassed $500M top line early in Q2

✅ #1 most searched pet insurance brand in the U.S.

✅ @lemonade_inc is now the 4th largest pet carrier in the U.S.

✅ AI-powered automation drives record claim handling efficiency (LAE: ~4%)

✅ Our data + tech edge lets us lower prices while boosting profitability

Car picking up speed

✅ Now at 60% YoY growth, $214M IFP

✅ Loss ratio improved to 74% (14 pts better YoY)

✅ Autonomous Car for @Tesla FSD conversion rate 70% higher than standard

And more...

↗️ Raising 2026 top & bottom line guidance

↗️ IFP per employee > $1M (3x improvement in 4 years)

↗️ Positive Adj. EBITDA in Q4

↗️ Investor Day in NYC November 17

English

Be รีทวีตแล้ว

Over the past 12 months, I've written 10 deep dives.

$HIMS

$ZETA

$SOFI

$GRAB

$RELY

$KLAR

$SE

$ONON

$NBIS

$LMND

Which company should I do next?

English

@Brian_Stoffel_ Assuming salesforce and adobe in here, maybe SE is the other…..?

English

I've completely sold out of 3 stocks I thought were great deals, but I lost faith in quickly

English

تشرفت بالظهور مع الصديق العزيز فيصل للحديث على الوضع الاقتصادي لدول الخليج والعالم بعد الحرب في حلقة سريعة..

من هم الأكثر تأثرا، من الأقل تأثرا، من المستفيد، ما هي الحلول المالية أمام دول الخليج لتخطي هبوط الايرادات، سياحة الخليج إلى أين، و أمور أخرى

مشاهدة ممتعة

بدون ورق@bidonwaraq

أغلقت إيران #مضيق_هرمز، الممر المائي الوحيد الذي يربط الخليج العربي بالمحيط المفتوح، وتوقفت مع هذا الإغلاق حركة النقل في الساحل الشرقي للخليج. تابعنا أولى ملامح تأثر اقتصاد العالم بهذا الأمر، فما هو القادم؟ و كيف يبدو المستقبل في ظل هذه الظروف؟ نلتقي الليلة حمد الماجدي، الاقتصادي المتخصص في المالية والمصرفية والمحاسبة. youtu.be/cXfBiMvsuEg?si… مشاهدة ممتعة!

العربية

Bought more $DUOL today in the big portfolio.

My new average is $186.4.

English

@Brian_Stoffel_ Amazon actually does facilitate this exact dynamic, though they often use partners. They lean heavily on Affirm for consumer "BNPL" financing at checkout to drive sales, and Amazon itself directly loans billions of dollars to its 3rd-party sellers to help them buy inventory.

English

On one hand, the dynamics pointed out about $SE are important -- keep an eye on the Monee loan book

At the same time, saying "Shopee is lending to customers that buy from it" isn't quite right.

Shopee is almost entirely a 3rd party marketplace. It has data on buyers that others don't. It's loans are small and very short term...for now

Thomas Claugus II@tclaugus2

I exited $SE I just got one very , I think, reasonable observation. They are lending to the buyers on their marketplace. This is a difficult model to pull off when you lend to customers that buy from you. 80% of the Y/Y growth in the ecommerce topline can be attributed to Shopee Pay loans through Monee. Hey, I will loan you $20,000 to buy my jeep and I'll book a profit on the lending and the sale. Look, as long as you get the $20K back it is ok. But what if they want to keep sales momentum and they make loans they shouldn't . I just don't like this setup... You should never be the lender and the seller at the same time imo. But I guess auto dealers are the same. Seems odd to me... Amazon doesn't do this. I just wanted to point these things out. Bye!

English

*IF* merchants don’t balk, a massive sign of strength for the moat

If they do….

$SE

Zack Zhu@the_zack_zhu

Just in: Shopee $SE is adding a 5% technical support fee on all cross-border sellers from China to Singapore, Malaysia, Thailand, and Vietnam, starting 2026.02. Shopee will also give out ad credits in return, although the ad credit amount will be lower than 5% of the overall sales. — Before this fee change, they already announced a massive increase in commission across all 6 countries in SEA + Taiwan (excluding Indonesia).

English

Interesting perspective on the capital and talent influx here. With everything that has developed recently, do you still see the momentum accelerating in the exact same direction?

Bipul Sinha@bipulsinha

MIDDLE EAST MOMENTUM The Middle East is a new Europe. After travels in both the Kingdom of Saudi Arabia and the UAE, I am even more convinced. Like Europe, the Middle East offers enormous growth potential and tremendous market size. More specifically, it brings three elements of success to the table: 1. Political will. All through the Middle East, there is state-level alignment to accelerate technology adoption and infrastructure. 2. Capital. They have money to spend on new technology adoption, including next-gen infrastructure like AI. 3. Talent aggregation. By inviting pioneers from around the world, including Europe, Australia, and the U.S., leaders in the Middle East are creating a local pool of global, ambitious talent. These three elements form a unique foundation for the Middle East to emerge as a global powerhouse. I look forward to the continued momentum of this region. #AI #GlobalMarkets #MiddleEast

English

English

@dcarballoAI @TheLongInvest If $DUOL hits $115 I’m selling the furniture, the car, and possibly one kidney. Fundamentals don’t care about your fib lines

x.com/KarelMercx/sta…

Karel Mercx@KarelMercx

Today’s reason, because $DUOL is still trading below $180: Duolingo and the Math Nobody Seems to Understand Chart 1 shows the cash Duolingo generates, and that is ultimately why you invest in a company. Last year there were two quarters where cash didn’t increase. That’s when you pay attention. Management explained that this pause came from higher AI expenses during the rollout of Duolingo Max, their premium tier designed to help you learn a language faster and better. Those temporary AI expenses pushed margins lower for a short period. But here’s the key point: the price of using AI always comes down. Duolingo benefits from that trend more than almost any company. Either their costs fall as models get cheaper, or they can buy far more AI capacity for the same dollar. They don’t need to invest billions in chips or datacenters, and they don’t carry the risk of wondering whether those investments will ever pay off. By listening to every earnings call and studying the numbers each quarter, you already know in advance when margins will dip. So when this temporary margin pressure appeared, it wasn’t a surprise. Yet almost no one seems to do their homework, and a single datapoint is enough for people on X to tell me I’m wrong. Chart 2 shows this margin dip. Once Duolingo Max was launched and AI costs started falling, and AI costs always fall quickly, margins recovered. Go back to Chart 1 and you immediately see how much cash the company added again. Margins will dip again, because Duolingo has openly said they can already see the point where the product becomes as good as a private tutor. And reaching that level requires more reinvestment. What do you think margins will look like once Duolingo is as good as a private tutor? Doing your homework is the common thread in investing. While Duolingo is racing toward a level comparable to a private tutor, people still reply under my posts claiming that the app teaches only simple sentences you can’t use in daily life. That view is years out of date and clearly shows they haven’t looked closely. Chart 3 is Spotify. The only reason this chart is here is to show what happens when a company grows 50 percent per year and then sees its percentage growth slow sharply into single digits. Cash flow tends to explode during that transition. The reason is simple: margins improve, and absolute revenue keeps rising. Many people told me Duolingo’s growth is “slowing,” but what they mean is percentage growth. And percentage growth is irrelevant without context. Fifty percent growth on 100 million adds 50 million. Ten percent growth on one billion adds 100 million. So nominally the growth isn’t 80 percent lower, it’s actually 100 percent higher. 😉

English

$DUOL has lost the 0.78 FIB too AT $164....YIKES!!

Next potential support is at $115

Anyone that recommended this and does not understand how technicals work should not be taken serious.

English