OneGrittySeed

1.7K posts

OneGrittySeed

@OneGrittySeed

Interests: games, value investing | CFA

New York, NY Sumali Ekim 2017

521 Sinusundan365 Mga Tagasunod

The Top Ten Athletes of All-Time:

1. Michael Jordan

2. Tom Brady

3. Tiger Woods

4. Shohei Ohtani

5. Michael Phelps

6. Usain Bolt

7. Muhammad Ali

8. Wayne Gretzky

9. Deion Sanders

10. Cristiano Ronaldo

Do you agree with this list or na??

English

I'm a huge fan of the drama series "Midnight Diner." It was recently announced that a new series will be broadcast on Japanese television for the first time in seven years. The lead actor, Kaoru Kobayashi, is now 74 years old, and the comforting flavo will be even deeper.

English

@AutismCapital What about dogs? I wipe my dog’s feet after every walk.

English

Can we all agree it's disgusting to walk into your home with outside shoes? That's the whole point of a foyer. The shoes go off in the foyer, your household shoes go on, clean house, peace of mind. If you don't have a foyer, the entryway is fine. The only reason to be against this is either laziness, because it's something new/different, or you feel anxiety asking guests to adhere to your rule structure.

Do not fear. They must adhere.

You are the master of your domain.

Andra@BioavailableNd

Wearing outside shoes inside the house. According to Dr.Gerba, Microbiologist, there's a 96% chance there's fecal matter on your sole and +400k units of bacteria.

English

@rohanpaul_ai I wonder if they would change patent rules. It would be interesting rug pull.

English

🇨🇳 China's patent filing rose by 67.7x between 2000 and 2024.

From 26,553 patent applications in 2000 to 1.8mn in 2024.

The US sits at 503K and Japan at 421K.

A very different IP battlefield than the one people were used to in the 2000s.

Rohan Paul@rohanpaul_ai

NeurIPS 2025's top 50 paper contributors show China and the US neck-and-neck. In the US, corporate labs—Google DeepMind, Meta, Microsoft—now rival top schools like Stanford, CMU, MIT, showing a major shift to industry-led AI research. China’s leaders remain academic: Tsinghua, CAS, Peking, SJTU, HKUST. Singapore (NUS, NTU), Korea (KAIST), UAE (MBZUAI), and Canada (Mila) hold strong. Europe trails, with only Oxford, EPFL, ETH Zurich, and TUM from the EU-27 making the list. --- Source: linkedin. com/posts/pierre-alexandre-balland-20b75b13_who-pushed-the-ai-frontier-at-neurips-2025-activity-7403119036496162817-vRPE

English

@BourbonCap @grok Which ones have the strongest moat that is expected to last through time? Rank by strongest.

English

Wonderful companies near 52 weeks low

Palo Alto Networks $PANW

S&P Global $SPGI

Intuit $INTU

Axon Enterprise $AXON

Fair Isaac Corporation $FICO

Spotify Technology $SPOT

ServiceNow $NOW

TransDigm Group $TDG

Intuitive Surgical $ISRG

Blackstone $BX

Intercontinental Exchange $ICE

Booking Holdings $BKNG

Copart $CPRT

Synopsys $SNPS

Netflix $NFLX

Cadence Design Systems $CDNS

Microsoft Corporation $MSFT Not yet, but it’s heading there.

English

@michaelxpettis So Ricardo’s model is not realistic. It’s a fictional world constructed to illustrate a concept.

English

David Ricardo showed in 1817 that if each country produces according to its comparative advantage, global output is maximized. Many analysts argue today that China's trade surplus reflects its comparative advantage in producing everything, and so its trade surplus is good for global growth.

But that's not true, and that is certainly not what Ricardo showed. China has a competitive advantage, not a comparative advantage, largely for the same reason that it has such weak consumption – large direct and indirect transfers from the household sector, in the form of an undervalued currency, cheap credit, restricted labor, overspending on infrastructure, land and other subsidies, etc., subsidize production across the board at the expense of household consumption.

The point is that these lower production costs give China a competitive advantage in producing most things, but this not the same as a comparative advantage. The former means you are able to produce more cheaply than your trade partners. The latter means that the relative "cheapness" with which you produce some goods is greater than the relative "cheapness" with which you produce other goods, so that you can only have a comparative advantage in roughly half the goods you produce. This is because comparative advantage is about relative costs, not absolute costs, and while you can have lower absolute costs in most or even all things, by definition you cannot have lower relative costs in more than half of what you produce.

Ricardo's example shows this very clearly. In his model. Portugal produced both textiles and wine more cheaply than England, which meant that Portugal had a competitive advantage in all goods, and England a competitive disadvantage in all goods.

But Ricardo did not argue that the world would benefit if Portugal produced both wine and textiles, with England producing neither and acquiring them by running trade deficits with Portugal. Instead he showed that because the relative "cheapness" with which Portugal produced wine was greater than the relative "cheapness" with which it produced textiles, Portugal only had a comparative advantage in producing wine, and England had a comparative advantage in producing textiles.

He showed that if Portugal only produced wine, and exported some of it to England to buy textiles, and if England only produced textiles, and exported some of it to Portugal to buy wine, trade would be balanced and total output would be maximized even with Portugal's competitive advantage in both.

If you do the math in Ricardo's model, you quickly see that global output is maximized only when global trade is balanced. For global production to be maximized, countries should not be net exporters of all goods in which they have a competitive advantage. They should be net exporters only of those goods in which they have a comparative advantage, and they should use the proceeds of those export revenues to import those goods in which they have a comparative disadvantage.

Once you allow trade to become persistently unbalanced, you run into the problem that Keynes identified in the 1930s – trade imbalances allow countries that have become more competitive by suppressing domestic demand to export weak domestic demand to the rest of the world. When that happens, either total global production is reduced and unemployment rises, or debt must rise in the deficit country to make up for the weak demand in the surplus country and to prevent unemployment from rising.

Economists often cite David Ricardo's model of comparative advantage as one of the few, great, non-trivial models in economics, and so it is worrying that so few academic economists understand the math behind the model. Ricardo's whole point was to make the unintuitive point that competitive advantage is not the same as comparative advantage, and that the world benefits from balanced trade even when one country can produce everything more cheaply.

This becomes more obvious when you realize that just by changing the value of the currency you can shift competitive advantage from one country to another, whereas comparative advantage is structural, and does not shift so easily. The main point, which surprisingly few academic economists understand, is that Ricardo's model of comparative advantage is a model of balanced trade.

Hongshen Zhu@HongshenZhu

The reality is that China has the unparalleled comparative advantage in manufacturing consumer goods so any meaningful increase in domestic goods consumption are just devoured by domestic producers. You can’t count on goods to balance trade. The West still has comparative advantage in service. Convincing China to allow censored Netflix?

English

@shanaka86 Maybe input value for imports is lower than output value-added products?

English

China's $1.189 trillion trade surplus looks like strength.

It's the signature of collapse.

Exports +5.5%

Imports +0%

The surplus isn't foreign demand pulling goods out. It's domestic demand evaporating so completely that factories dump production globally at any price that clears.

No economy in recorded history has sustained 5% growth through 10 consecutive quarters of deflation.

Rhodium estimates actual growth at 2.5-3%—half the official claim.

The recognition catalyst arrives in days.

Vanke—the "safe" state-backed developer everyone thought had implicit government support—faces RMB 9.4 billion in bond maturities.

Bondholders rejected a one-year extension: 78.3%

Shenzhen Metro, the state-owned backstop, just issued this statement:

Support has "surpassed its risk comfort zone."

Cannot provide "unlimited guarantees."

The backstop just told you there is no backstop.

January 22

January 27

February 10

Three dates. Three bond deadlines. One forced recognition.

$4 trillion in China-exposed global assets was allocated based on an assumption the data no longer supports.

The bondholders already know.

The allocators discover it next.

Read the full deep dive story

open.substack.com/pub/shanakaans…

English

USA has NVIDIA

China has ALIBABA

Japan has TOYOTA

India has?

Español

@aakashgupta Meta will catch up. They have a lot of personal data too.

English

Google just revealed the AI moat nobody can replicate.

Every AI company is racing to build “memory” and “personalization.” Claude remembers your conversations. ChatGPT stores your preferences. Perplexity knows your search history within their app.

Google connects to a decade of your Gmail threads, every photo you’ve ever taken, your complete YouTube watch history, and every search query you’ve made since 2005.

The surface announcement is “Gemini gets personal.” The real announcement is that Google is activating a personalization layer built on 20 years of user data that no competitor can access.

OpenAI can’t read your Gmail. Anthropic can’t see your Google Photos. The data required to truly personalize AI already exists, and Google owns it.

This is why the AI race isn’t just about model quality anymore. The models are converging. The differentiation is in the data pipes. And Google has been quietly building those pipes for two decades while everyone else was focused on GPT benchmarks.

The question for every other AI company: how do you compete on personalization when your competitor has the user’s entire digital life and you’re starting from a blank conversation?

Google@Google

Today, we’re introducing Personal Intelligence. With your permission, Gemini can now securely connect information from Google apps like @Gmail, @GooglePhotos, Search and @YouTube history with a single tap to make Gemini uniquely helpful & personalized to *you* ✨ This feature is launching in beta today in the @GeminiApp. See Personal Intelligence in action 🧵 ↓

English

I used grok to turn pic into steampunk style and added Leonardo DiCaprio from Gangs of New York.

English

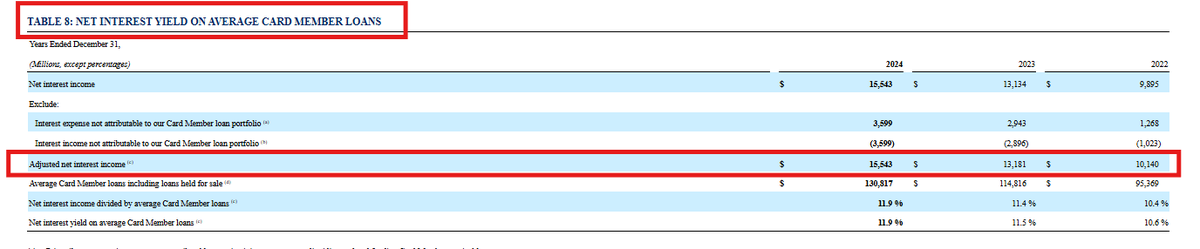

in 2024, Amex paid Delta $7.4 billion

in 2024, Delta's Operating income was $6.0 billion

The card program is hugely important

Amanda Orson@amandaorson

Your credit card rewards exist because someone else is paying 25% APR. Cap that at 10% and the points don’t survive. I spent years working inside fintech and card programs. That interest margin is the invisible buffer that makes rewards, lounges, and credits pencil out. Capping credit card APRs at 10% sounds like an obvious consumer win. Cards charge 20 to 30%, many consumers revolve balances, and the system feels punitive. But credit card economics are not just about interest rates. They are a cross-subsidized system where revolvers subsidize transactors, rewards rely on behavioral inefficiency, and risk-based pricing subsidizes access. Remove one leg of that stool and the system does not become fairer; it rebalances. And the costs show up where consumers notice most. Lets look at how this would impact 3 programs 1. AMEX Platinum A 10% credit card APR cap would not make your card cheaper or better. You would still have access, but you would almost certainly get less value for the same or higher price. The Platinum brand survives because its customers are affluent, pay in full, and tolerate high annual fees. What quietly supports that ecosystem is portfolio-level profitability, which allows AMEX to tolerate loss, overuse, and inefficiency in premium benefits. When that margin shrinks, the cost shows up directly in your (lesser) benefits. In a world where: - Rewards economics tighten - Devaluations become more likely - Flexibility is reduced Points become a liability to the issuer, and liabilities get repriced. So what this likely means for you as a Platinum cardholder: - Lounges do not expand to fix crowding. Instead, access tightens or amenities are reduced. - Statement credits become harder to use, more fragmented, or less generous. - Annual fees go up - New approvals become more selective, even for high earners. Your card still works, but the value proposition shifts. Platinum becomes more explicitly pay-to-play, with fewer hidden subsidies propping up premium perks. You pay the same or more, and you get a little less in return. Which is why some people are already warning that points devaluations become more likely in this environment (like @BowTiedBull this morning saying "Dump ALL your credit card points. All of them.") 2. Bilt Card This program is the canary in the coal mine for what to expect. Bilt’s super popular rent rewards worked because Wells Fargo was willing to subsidize them. The card offered 1 point per dollar on rent with no fees because Wells Fargo paid Bilt roughly 0.8 percent (80 bps) of each rent payment to fund rewards... despite earning little or no interchange on those transactions. But that is some actuarial level math with a number of variables at risk that proved wrong/ unsustainable. Wells Fargo was getting hosed $10 million a month on the program, so they exited the partnership years before the original end date and forced Bilt to restructure its rewards with a different bank What does that teach us? - When interest and interchange margins shrink, banks stop tolerating loss-leading reward programs. - Interest income does not fund every reward directly, but it provides the buffer that allows experiments like Bilt to exist at all. - Remove that buffer and rewards must be paid for explicitly. Bilt’s shift to a three-tier lineup with annual fees is not an anomaly. It is the direction rewards go when credit stops quietly absorbing losses. Pay-to-play rewards. What feels like consumer protection will shows up as fewer perks, pay-to-play rewards, and less room for innovation. 3. Credit One & other Subprime Cards Now the least glamorous corner. Subprime cards get criticized for high APRs, annual fees, low limits, minimal rewards. But they exist for a reason. They serve thin-file borrowers, damaged credit, people shut out of conventional loans, households using cards for liquidity not perks... but they charge high APRs because charge-offs exceed 8-10%, fraud and servicing costs are higher, and credit limits are small while fixed costs remain significant. A 10% cap makes these products mathematically impossible. These cards don't become cheaper. They cease to exist. As @sytaylor noted this morning - "You realize this will push many more customers towards loan sharks?" The demand for credit doesn't disappear... it migrates to BNPL with opaque effective APRs, chronic overdraft usage, fee-heavy installment loans, and less regulated lenders like loan sharks/ payday loans. So who WOULD win? Debit-First Fintechs One of the least discussed consequences: where would reward customers migrate? I think 1% cashback programs are an obvious winner. Chime, Varo, Current and niche cards like Greenlight and Privacy. (If you have not worked in a fintech or a bank you probably don't know what the Durbin Amedment is - but the TL;DR is that very large banks (BoA, Wells, JPMC) have capped interchange rates of around 27 bps on debit swipes. Small banks with < $10B AUM, however, do not - they can earn 1-2% on interchange (avg was 160 bps or so last I checked). Which is why all of the debit card fintech companies you've heard of are partnered with these smaller banks - they can offer rewards like 1% cashback programs and still have margin sufficient to build a business around.) In a world where credit rewards shrink, access tightens, and annual fees rise, debit-based fintechs look better by comparison. But consumers lose: credit protections, payment float, stronger dispute rights, credit-building opportunities. TL;DR An APR cap feels like consumer protection. In practice it reshapes the market in ways that are easy to miss: - It will shrink access to credit - Eliminate rewards programs that aren't tied to high annual fees - Force risk into less regulated channels - Unintentionally advantages debit over credit - Help affluent transactors more than vulnerable borrowers Credit doesn't become cheaper. It becomes scarcer, less flexible, less transparent. But banks will adapt. Fintechs will adapt. Consumers caught in the middle do not get protected. They get fewer choices, worse products, and priced out.

English

@ShowdeerArt @TheCinesthetic I have not seen this. Probably would never see it, until this post. I’ll check it out.

English

What movie is 10/10, yet hardly anyone has heard of it?

English

To actually see music, we built a real magic piano! This is our DIY video of the Year, hope you guys like it!

@redmagicgaming #REDMAGIC11Pro #GamingPhone

English

@HedgieMarkets This is a good take. Apple is making the right capital move. If Google raise prices, there are lots of competitors + open source. And R&D costs for Siri ai will decline over time as more graduates come into this market.

English

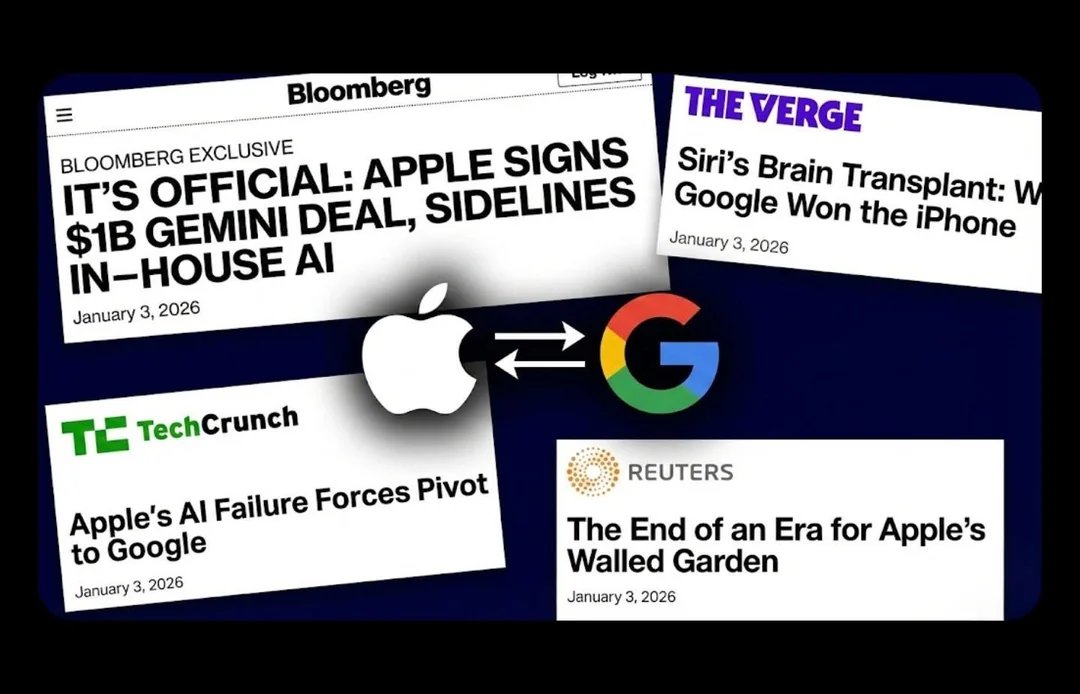

🦔 Apple is reportedly paying Google over $1 billion to use Gemini for Siri instead of building their own AI. After two years of marketing "Apple Intelligence" as the future, this is basically admitting they can't keep up with the LLM race. The partnership means Google now powers AI on both Android and iOS, which is a pretty remarkable position.

My Take

I actually think this might be the smartest move Apple has made in a while. Everyone else is lighting money on fire trying to build their own AI. OpenAI is losing $12 billion a quarter. xAI lost $1.5 billion in a single quarter while making $105 million. Meta is spending $70 billion on AI capex. Apple looked at that and said no thanks, we'll just license the best one for a fraction of the cost.

The optics look like a surrender, but the balance sheet says otherwise. They get a working AI assistant without the R&D burn, and if LLMs become a commodity in a few years, they haven't wasted hundreds of billions chasing something that might not differentiate them anyway. Google gets a nice revenue stream, Apple gets a product that actually works, and everyone burning cash trying to compete with both of them has to keep spending to stay relevant. Sometimes the best move is letting someone else win the arms race and just buying the weapons.

Hedgie🤗

English

@garyleff @BillAckman Help me understand this. I agree that financing customers subsidize reward customers to a degree. But how does this benefit the merchant? Is cash cost to merchant greater than the 1.5-3.5% interchange fee?

English

This is backwards.

Cost of cash acceptance is higher than credit cards (incorrect change, employee theft, insurance for holding large cash amounts) so any subsidy goes the other way.

Card purchasers spend more per transaction and cards bundle financing so this benefits merchants.

The actual subsidy is from card customers who finance their purchases to those that don't. Rewards cards often rebate the full value of interchange to the customer in search of financing customers.

Where interchange has been capped prices to consumers have never gone down! It redistributes away (steals) from consumers (rewards) to merchants by force of law.

English

On the topic of credit cards:

It seems unfair that the points programs that are provided to the high income cardholders are paid for by the low-income cardholders that don’t get points or other reward programs with their cards.

Points and rewards programs are in effect a rebate on every purchase. The higher the reward benefits, the higher the discount fee the card company charges the retailer to cover the cost of the benefits. The greater the rewards, the higher the discount fee.

Discount fees can be as low as ~1.5% for cards without rewards but as high as 3.5% or more for ‘black’ or ‘platinum’ cards.

Since the retailers or service establishments charge all consumers the same price for the same items or services, the millions of lower income consumers with no reward benefits are in effect subsidizing the platinum cardholder when he uses his card. In other words, the low income consumer is paying an extra 2% on his credit card purchases to cover the rewards points for the platinum cardholder.

This doesn’t seem right to me. What am I missing?

English

@SlLENTPRINCESS It sounds roughly same to me. Other music experts are just envious that he pointed it out.

English