Nathan Erickson, CFA

763 posts

If I were a financial advisor looking to seriously grow my book, I would give a presentation to the C-suite, investor relations, and employees of the top 10 public companies in my area. (Ditto with VCs, CPAs, and companies going public).

I would explain 351s to them and offer to hold their hand through the process.

95% of people still haven't heard of 351 and a LOT of money is in motion. We get emails every day from @spacex employees....

Wirehouses can't do it, @Fidelity won't do it. Big opportunity for the independents to raise serious $ that likely is time limited...

cambriafunds.com/351

English

@spencerjogden @MarkTMeredith @ElmWealth If you don’t unwind the strategy, losses continue to accumulate in perpetuity. You can withdraw a percentage each year tax free so you can use it…

English

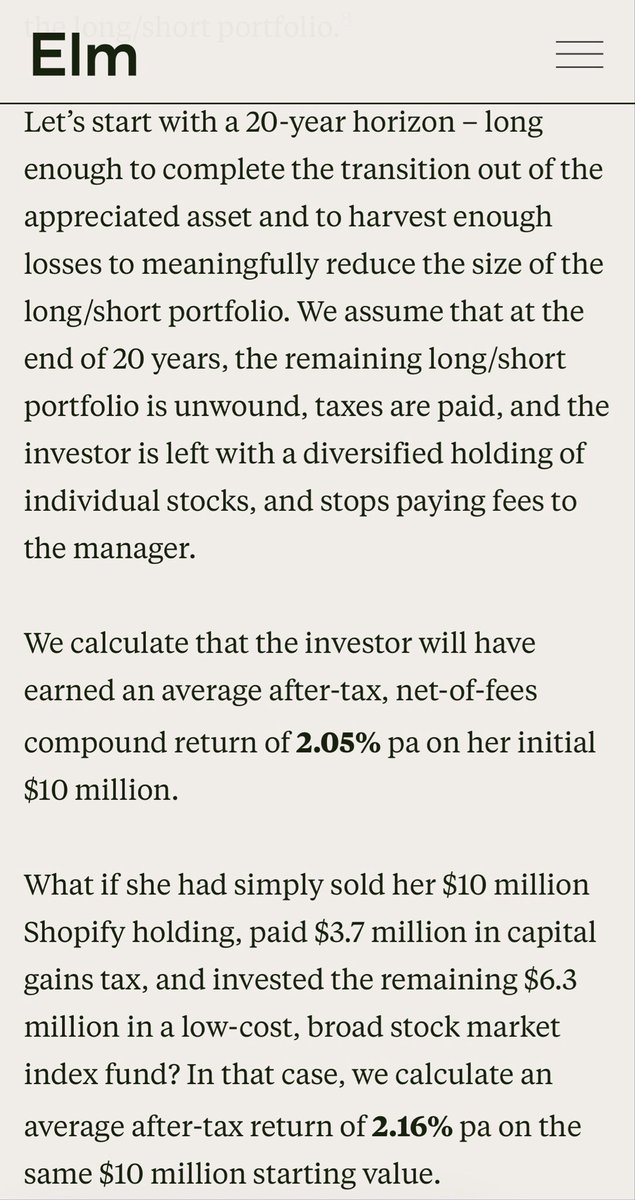

Final someone did the math.

But they left out a huge part!

After all of that (and driving their CPA insane), they are left with a diversified portfolio with just as low a cost basis as their Shopify. $10m in unrealized gains turns to $29 million.

Cap gains tax has not been eliminated, it has been deferred. Pay taxes later is always nice, and may have real value as noted (moving states or dying).

But if you are planning on actually using your money,,,

English

@justinaknope did you ask the short seller if they plan on using tax loss harvesting to defer the gains if their short position works out?

English

Big call on the future of tax alpha:

A short seller is targeting AMG for its stake in AQR, saying AQR’s recent growth “is built on regulatory arbitrage that faces immediate scrutiny"

For context, AQR's tax-aware long-short AUM is now $68.8b vs $189b firm AUM at year-end

English

@debt_serious It’s covering the risk of being a tax shelter. If there’s no economic substance (pre-tax alpha) and you’re selling a tax-deferral strategy you run the risk of being classified a tax shelter. By saying the primary draw is the alpha, then you’re not selling a tax solution.

English

@LeylaKuni $16B in exposure to retail is about 5% of all semi-liquid. He can make the number sound small but it’s not nothing. Also the Apollo S3 semi-liquid private markets fund has 80% PE secondaries in it so…

English

I attended a breakfast roundtable with $APO's Marc Rowan.

Some quotes (starting with my favorite):

> "It's not private equity. It's equity that is private" -- this is how he described an actual PE deal done with $3B in debt and $8B in equity (underwritten to 13% IRR, btw)

> they have $15B in this private equity that's not private equity, expect this sleeve to grow to $40B by EOY.

> private equity that *is* private equity is at $100B and is NOT a growth business for them.

> "There is virtually no difference between PC and BSL. BSL loans are just held by multiple lenders" -- don't shoot the messenger, guys

> APO's exposure to retail investors in semi-liquid vehicles is only $16B (against $1T in assets)

> The firm made a deliberate decision to not offer PE in a semi-liquid form, and he strongly dislikes use of NAV as practical expedient

> They see great opportunity in the 401(K) market (no surprises here)

> If you expect more transparency on the portco level, it ain't coming (I asked)

English

@patefortworth @RevGroupLLC Just because they hold the same assets doesn’t mean it’s the same investor experience. You’re adding a risk factor of market volatility. The public could stay at the same discount or decrease further. Not a guarantee that as soon as you invest it immediately returns to par.

English

@RevGroupLLC It’s a real question I’m asking you. For holders of private BDC’s, what is one reason why you wouldn’t be redeeming out your 5% per quarter at par and reinvesting those funds into public BDC’s (which hold the same assets) at the current steep discount?

English

Private BDC holders: redeem everything now if you haven’t already.

At least you’re then in the same boat with everyone else, getting money back slowly.

First it’s Blue Owl; next quarter it will be all of them. Don’t be the bag holder.

Also, if an advisor put you in… 🚩🚩🚩

English

@TaxAlphaInsider It is not easy to transfer but can be done.

English

Now, more than ever, advisers need to understand the operational mechanics of transferring an entire long/short strategy between custodians. DM if you have insight. I'll turn it into a best practices blog co-authored if it helps you.

English

"complete rug pull" ... advisers telling me Fidelity is dramatically raising financing costs for tax aware long short in coming months. DM if you have a story to share.

English

@NickNemo17 Under the assumption that the public market mark is right.

English

$BXSL and $BCRED are managed by the same Blackstone Credit team with what Blackstone itself calls “significant overlap” in investments — same borrowers, same seniority, often same origination. A 500M first-lien to Zendesk can sit in both vehicles.

The public market prices BXSL at 88 cents on book. Whether that discount reflects mark optimism, illiquidity risk, or both, the market is saying these loans aren’t worth par.

BCRED holds substantially similar loans but pays redemptions at full reported NAV — 100 cents on the dollar of Blackstone’s internal marks. No market discount applied. Redeeming investors at $24.79/share are getting a better price than the public market would assign to economically equivalent assets.

The money funding those redemptions — cash, credit line draws, Blackstone’s own 400M Q1 2026 injection — belongs to all remaining shareholders. Every dollar paid out at full NAV to a redeeming investor is a dollar unavailable to those who stay.

Any investor who believes the marks are even slightly generous has a rational incentive to redeem immediately, because the last investors out bear cumulative dilution. The dynamic is reflexive: redeeming makes staying more costly, which incentivizes more redemptions.

*Nemo’s helpers are growing by the day

English

@zerohedge Can’t believe how many people are quoting LENDX as the next shoe to drop. The 11% isn’t new, it’s literally been been 16+ straight quarters of various pro-rata. It’s a different market, all consumer loans, and hasn’t been good for awhile. But keep selling the PC story.

English

The Private Credit Crisis Is Spreading zerohedge.com/markets/privat…

English

@UnicusResearch Fund has been gated since at least 2022. It was always a pile of garbage.

English

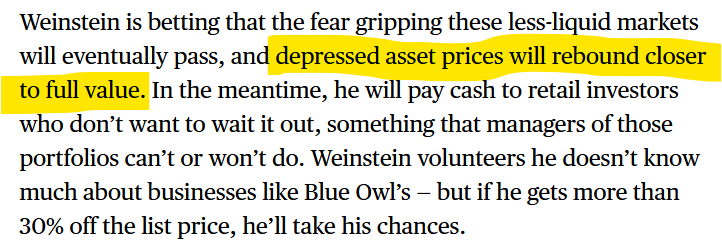

@debt_serious @boazweinstein If that isn’t a sign of what’s going on, I don’t know what is. Him and his team out here stoking fear so he can buy discounts and hold to par. In public markets that’s a crime.

English

@boazweinstein, were you misquoted in the article or you believe those BDCs loans are worth near par?

bloomberg.com/news/articles/…

English

@kieranwgoodwin Everyone complains about the marks and then when a fund marks it’s a bad sign?

English

BCRED posting -0.4% is definitely not helping redemptions for funds with open windows.

Financial Times@FT

Flagship Blackstone credit fund posts first monthly loss since 2022 ft.trib.al/xpZhm0i

English

@tyillc Just poor reporting by WSJ and Bloomberg. LENDX has been gated since at least 2022. It’s been a challenged portfolio for awhile, completely independent of any perceived risk in senior secured private credit.

English

Confirmation of my statement "once the valuation story supporting one opaque sector of the financial system is called into question, valuation stories supporting all the opaque sectors of the financial system are called into doubt" ...

wsj.com/finance/invest…

English

@UnicusResearch It didn’t “just” tell investors. It’s been gated since at least 2022 paying out partial redemptions. It’s not the next domino. Its loan book has been underperforming for years. Risky consumer credit.

English

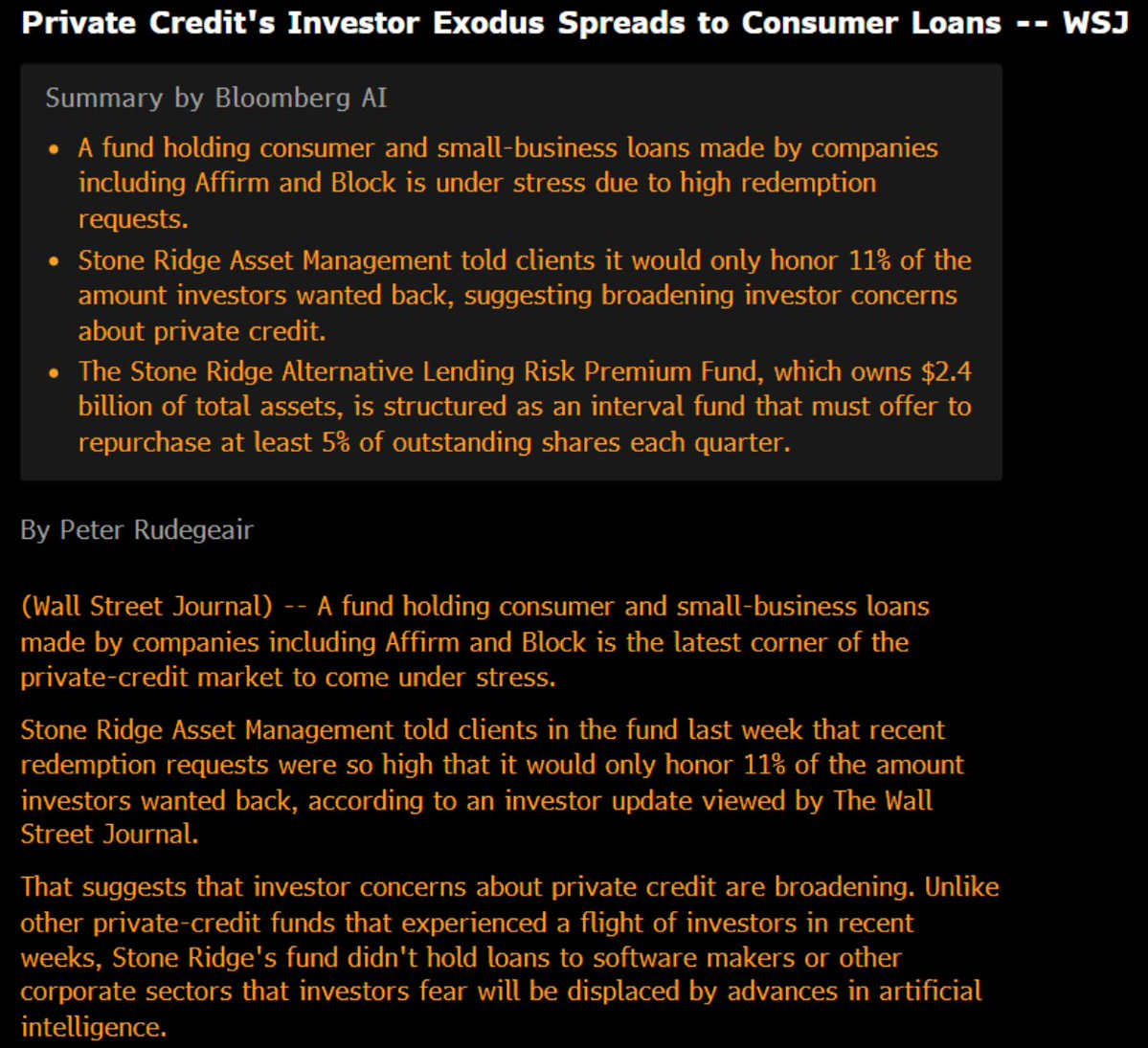

🚩🚩UPDATE: This is a problem. Stone Ridge's LENDX fund consists of tens and thousands of BNPL loans ranging from $5-$2000. Most appear to be in default.

The PDF is 8000+ pages. Our analysts are reviewing only for one BNPL firm, for now.

Now, we are determined to publish our analysis by Friday on substack just for one BNPL loan pool.

Why? because we want everyone to be aware.

These turds are in retirement account.

Unicus@UnicusResearch

🚩BREAKING: Stone Ridge's LENDX fund just told investors it would honor only 11% of redemption requests. (WSJ) That means for every $100 investors wanted out, they got $11. Here's what's actually inside the fund. 🧵

English

@BenKizemchuk @Investor_NICK_ Do your research. LENDX is not the next domino. It’s been gated since at least 2022 paying partial redemptions. Consumer lending has been garbage for awhile.

English

Contagion

h/t @Investor_NICK_

Negligible Capital@negligible_cap

Private credit’s investor exodus is spreading to consumer loans, according to WSJ Interval fund Stone Ridge Asset Management, which holds consumer loans made by $XYZ and $AFRM are apparently under stress due to redemption requests Stone Ridge honoring 11% redemption requests $XYZ, $AFRM selling off on the article

Français

@zerohedge If you’re talking about LENDX, it’s not the next domino. That fund has been gated for years.

English

Private Credit Panic Spreads As Consumer Loan Fund Gates Investors, JPMorgan Pulls Deal, Apollo Sees 20 Cent Recoveries zerohedge.com/markets/privat…

English

@negligible_cap Crazy. LENDX has been gated for years but no one’s said anything until true private credit has seen redemptions. And there is no comparison with LENDX and senior secured private credit. LENDX is all risky consumer debt.

English

Private credit’s investor exodus is spreading to consumer loans, according to WSJ

Interval fund Stone Ridge Asset Management, which holds consumer loans made by $XYZ and $AFRM are apparently under stress due to redemption requests

Stone Ridge honoring 11% redemption requests

$XYZ, $AFRM selling off on the article

English

@LeylaKuni This one warrants heavy criticism. It’s actually been pro-rating redemptions since at least 2022. Last payment was 11% of requests (Request $100, get $11). Performance has been low single digits for at least five years. All consumer credit. Multitudes worse than any other PC.

English

@TaxAlphaInsider @HankRobertsIV That’s true regardless of what you put in the IRA. If you’re doing asset location and looking at accounts at a portfolio level, the IRA is a great home for private credit.

English

In IRA, you're gonna withdraw at ordinary rates, right? So, no tax drag, but a tax pain this generation or next will have to solve.

And for HNW+ marginal rate probably isn't going down. For retirees... well now you're saying a retiree should have private credit. I don't know if that's highest/best use. Maybe it is. But I'd want to chase that down.

In roth, I think I'd rather have my hyper growth assets there.

Let me know if I missed any nuance on the matter. I could have.

English

Why do people invest in private credit?

A little extra (tax inefficient) return in a tiny slice of the portfolio in exchange for really annoying diligence, and all of the terrible content people are creating about it.

Oh yeah. And the risk.

English

@tyillc @LeylaKuni 86% of companies with over $100M are private. If no one invests in PE/PC again, the U.S. economy will crater.

English

Hopefully investors will learn the lesson of never investing in opaque Private Equity/Private Credit deals again ...

The multi-year slow loss of their investment should be a constant reminder to both this and the next generation of investors to avoid opaque deals like the plague ...

English

There is every incentive to keep the machine going - and PE/PC managers have a number of tools that will allow them to do so

It will be a slow bleed, with LP money stuck in some vehicles for a while, only to generate dismal returns on exit..

Great read:

Mojo@MrMojoRisinX

This is a work in process (call it a journal entry), but this is where my head is at re private equity, private credit, and whether or not there will be an actual recognizable cycle... If you are looking for a trading implication, it is early from my perch, it is selective, and it is not an asset class call. More on that here: x.com/MrMojoRisinX/s… Nobody Is Lying. That's the Problem: The debate over private market marks gets framed as a question of accuracy. That is the wrong frame. The real question is who has the standing, the incentive, and the mechanism to force a reckoning, and when. The answer to all three is: nobody, not yet, and maybe never cleanly. The reason is structural. The ecosystem includes the PE sponsor, private credit manager, BDC, auditor, and leverage provider, etc. Every one of them has asymmetric incentives that point toward deferral. The auditor signs off because GAAP allows fair value estimation using income approaches when comparables are deemed not directly applicable. The credit manager says the loan is current. The BDC says NAV is supported by discounted cash flow on performing assets. The bank continues to provide the leverage facility because the BDC hasn't breached its borrowing base. Everyone is technically correct. Nobody is lying. And the capital structure of the 2022 LBO is quietly underwater on an equity-value basis. The comp tables and stock charts say so. There is no mechanism to force that into the books. Two Different Questions: For private equity, the mark question is cosmetic in the short run. The LP gets a depressed quarterly NAV, doesn't love it, but the GP isn't selling so there is no realization event. The fund hasn't failed. The management fee runs on committed or invested capital, not NAV. The carry is impaired on paper but the GP is not writing a check back. The LP is locked up. Nobody forces the trade. For the BDC, the mark question has real-time consequences. The BDC is a public vehicle with a disclosed NAV, a leverage facility tied to that NAV, and shareholders who can sell. When a BDC trades at a 20% discount to NAV, the market is saying it doesn't believe the NAV. But not believing it and proving it are very different things. The board's valuation committee, advised by an independent third-party valuer, has blessed the marks. The auditor has signed off. The leverage provider hasn't accelerated. The BDC sits in a strange purgatory: the equity market has already priced the impairment, but the book hasn't moved. What Actually Breaks the Logjam: There are only a few forcing functions, and they operate on different timelines. The first is a payment default or PIK election on an underlying loan. The moment a borrower starts PIKing interest or misses a payment, the valuation committee has no choice but to move the mark, the auditor has no choice but to agree, and the leverage facility gets tested against a new borrowing base. This is the most direct trigger and the one everybody is working hardest to avoid, including the borrower, who is often getting help from the sponsor to stay current. The second is a leverage facility redetermination. Banks do periodic borrowing base reviews. If they tighten advance rates against certain asset categories, and they have been doing this quietly, then the BDC suddenly has less liquidity and has to either sell assets or reduce the facility. Selling performing assets at par while marking nothing else creates a contradiction the valuation committee can no longer explain away. The third is a portfolio company refinancing or sale process. Sponsors will sell the winners, the companies that performed and can clear at strong multiples, both to generate DPI and to demonstrate the fund is working. The weeds stay. Marked wrong, unlikely to be sold at a loss, and with no covenant or maturity pressure forcing the issue, they sit on the books indefinitely. The exits that do happen create comps on record for similar assets, but nobody is required to use them. The gap between realized prices on the good assets and carrying values on the bad ones widens quietly, and the bad ones never come to market to prove it. The Covenant-Lite Problem Is Deeper Than It Looks: The standard critique is that cov-lite loans removed the early warning system. True, but it understates the problem. Covenants were never primarily a restructuring tool. They were an information and renegotiation trigger that forced the borrower to the table before the hole got too deep. Without them, the creditor has no standing until cash stops flowing. Cov-lite combined with no amortization combined with PIK optionality creates a structure where a company can be economically insolvent on an enterprise-value basis for years while remaining technically current on all its obligations. Interest coverage might be 1.2x, but it's positive. The equity cushion might be negative on a comp-adjusted basis, but nobody has marked it that way officially. The company is performing. In any prior credit cycle, covenants would have fired, a restructuring would have happened, and the capital structure would have been right-sized. In this cycle, you can paper over it indefinitely as long as the business doesn't shrink. EA is a live illustration of this dynamic. Silver Lake and its consortium signed at a price the public comps have since moved well below. The debt will get syndicated, the business will perform, and if the broader software market recovers the credit looks fine in hindsight. Reflexivity works in both directions. What the EA situation actually illustrates is that there are three distinct outcomes in this environment: narrative compression that reverses, real fundamental deterioration that doesn't, and a third category where the rational move is to walk from the deal entirely. EA is in the first bucket. Not every deal is. Where This Goes: The most likely path is a slow-motion grind rather than a sharp dislocation. PE sponsors will start selectively realizing their winners both to generate DPI for LPs demanding distributions and to demonstrate the fund is working. This is already happening (look at lower middle market). The weeds stay on the books. BDC managers with dual roles in private credit and PE will face increasing shareholder pressure on the incentive structures. The conflict, where the BDC's slow liquidation damages the same portfolio the affiliated PE fund is managing, is becoming hard to ignore. Governance activists will push on it. They are commercial animals pursuing their own interests while performing concern for all holders. Credit quality bifurcation will widen. Large-cap, well-covered, sponsor-backed loans will stay performing. The middle market, where coverage is thinner and the equity cushion was smaller to begin with, will see the first real defaults. When a payment miss forces a mark in one lower middle market company, the contagion risk is sector-specific and real. Similar companies, similar sponsors, similar structures. The question is whether anyone in that chain is also missing payments. Then the macro does the rest. If rates stay elevated longer than the models assumed, if AI genuinely compresses multiples rather than temporarily suppressing them, if the revenue growth baked into 2020 to 2022 underwriting proves to have been a COVID pull-forward rather than a structural step-change, then the earnings power assumptions holding the marks in place become increasingly difficult to defend. Not that anyone will be asked to defend them. The system has been engineered so that no single party has the standing or incentive to force the issue. What breaks it is the accumulation of realized exits, tightened borrowing bases, and middle market defaults that collectively make the existing marks indefensible. That process is already underway. It just doesn't have a name yet. There are other mechanisms worth noting. Continuation funds, insider buying patterns at both the manager and BDC level, LP secondary market discounts, dividend recaps, and the insurance capital channel into private credit all deserve their own analysis. We chose not to go deep on any of them here. What matters for this argument is that every one of them is another way to mask the same problem, extend the timeline, or obscure the gap between book and market. None of them change the structure of what we are describing.

English