@AISavvyCapital @Gubloinvestor can you please explain? :)

English

BuffettMunger

57 posts

Great optics piece by Citrini. Few comments before people do stupid things at open... Do not touch HiMax or Poet. Aixtron is best foreign pick. Furukawa second best foreign pick. Nokia is best domestic pick. I was on the fence with Soitec and now a buyer.

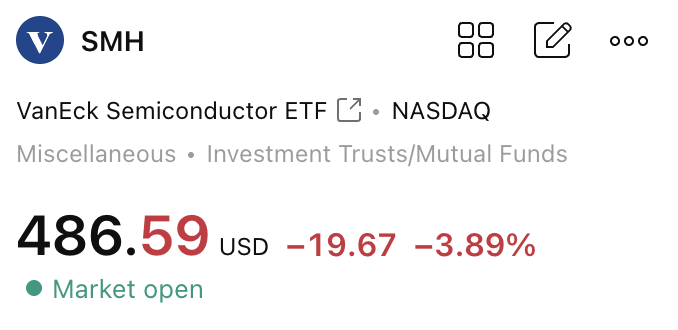

Now $4.20 $INDI

800 VDC Architecture for AI Data Center Economics $POWI $VRT $BE $FLEX The video provides a comprehensive overview of the emerging 800 VDC architecture for high-density AI data centers, positioning it as the necessary successor to traditional AC power distribution to support 1 MW-class racks. This architecture shifts power conversion to a facility-level rectifier, distributes power at 800V DC to reduce current, resistive losses, and copper usage, and then steps down locally within the rack. The adoption of 800 VDC is closely tied to NVIDIA's Kyber rack-scale system, which is targeted for a full-scale production rollout beginning in 2027 and leverages wide-bandgap semiconductors like SiC and GaN for high-efficiency conversion. Economically, the move promises substantial recurring savings through improved power efficiency and lower maintenance costs, alongside capital expenditure gains from reduced copper mass and increased revenue-generating white space. However, the transition presents safety and integration challenges, requiring new DC-rated protection gear and a phased, greenfield-first approach for operators.

$MXL +76% in one day. As I posted before Friday’s open: this was the inflection point. Why the massive re-rating? 1⃣Optical DSP Ramp:Management raised 2026 Optical revenue guidance by ~50% (from $100M-$130M to $150M-$170M). The Keystone (5nm) family is no longer "in testing" - it is in a massive production ramp with US and Chinese hyperscalers. This validates MXL as a legitimate peer to Marvell in the 800G/1.6T cycle. 2⃣The "Wafer Signal": Negative OCF (-$8.9M) was driven by aggressive wafer capacity prepayments. In a high-rate environment, you don't prepay unless you have firm, non-cancelable orders for H2 2026. This is the ultimate leading indicator for a massive revenue jump. 3⃣Liquidity Risk Removed: Extending the credit facility to 2028 and stabilizing Broadband revenue ($44M) killed the "distressed debt" thesis. This forced a violent short squeeze as the bankruptcy narrative evaporated. ⬇️Market Context: ➡️The Pivot: MXL shifted from a "cyclical cable play" to a high-margin "AI Infrastructure" play. ➡️Second Sourcing: Hyperscalers are actively moving volume to MXL to break vendor lock-in.