@mr_deepvalue No, because their working capital is highly volatile. Big swings in (f)cf because of it. Dont pin me on the exact numbers but I think the FCF for 2025 is 4.6m whereas OE are 2m. For 2024 its something like 1.6m FCF and 2m OE. EV/OE is imo cleanest

Found a Japanese business trading at 40% of TBV.

It's also a net net (0.9x).

The business is mediocre, though probably not 'dying'.

They actually control a few little niche sectors, which have proved to be resilient.

What makes it interesting is that the management have recently pivoted towards returning capital to shareholders.

This could be a decent catalyst over the next 1-3 years, and there is room to double or even triple back to TBV.

It would likely do well as part of a basket of dirt-cheap stocks, for those that invest this way.

The ownership structure and the capital-intensive nature of the business put me off.

I'm not going to buy it so sharing here in case anyone else likes it...

The business is Xebio Holdings (8281).

@thestockdigger I think the magic is in the portfolio dynamic.

Each stock might go nowhere or double, but a group of them does well pretty consistently.

@mr_deepvalue I really feel like japan deep value is the lottery right now.

I found NIX $4243 which cash excluding debt covers the entire market cap.

It can pop up anytime but also can be a long time waiting 😅

Another Japanese stock with cash alone covering 98% of the market cap.

The business is asset-light and cash generative.

The problem is that revenues have halved in the last 3 years(!)

The biggest issue tho, is that management have never paid a dividend or shown any hint of buybacks.

Plus the founder controls 67% of the votes, so a no-go for me...

Sharing in case anyone likes this type of set up.

The business is Premier Anti-Aging Co (4934)...

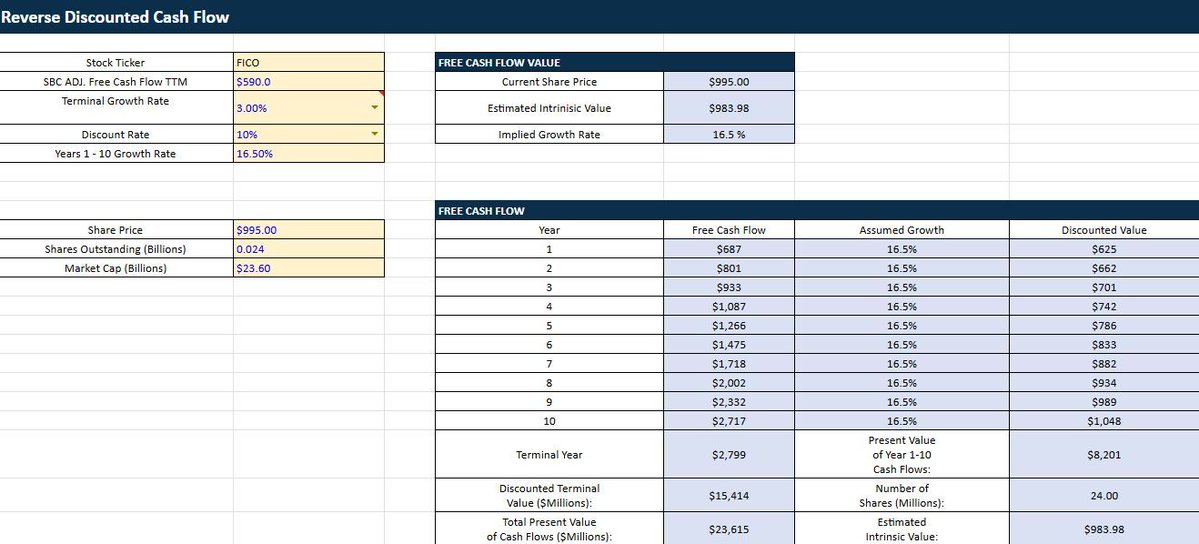

I ran a reverse DCF on $FICO.

At $995, the market needs just 16.5% FCF growth annually for 10 years to justify the price.

SBC-adj. FCF: $590M

Implied intrinsic value: $984

For context, this is a business that:

• Scores every American's creditworthiness

• Has no credible competitor

• Raises prices because it can

16.5% priced in.

For a monopoly.

The bears built this valuation. Not the bulls.

Very nice write up, I agree with almost everything except, I think the multiple you use to get to the valuation is a bit aggressive. If we say normalized owner earnings are 2m-ish then it trades for 6.5x OE. With margins at 2.7% and such client concentration I'm doubtful we can justify much more than perhaps 8x OE. Add 4m-ish in cash you get to 20m valuation or 160-170p/share.

This is watchlist material for me also: The liquidity, lack of growth, client concentration and razor thin margins require a higher margin of safety imo

Found a pretty compelling Japanese business trading at 3x FCF.

The operating business is robust and cash generative. The balance sheet is stacked with (too much) cash.

Adjusted ROE is 100%.

Crucially, the ownership structure is wide open for an activist to take a controlling stake.

I'm going to write this one up...

Took my first real vacation in 3 years - only worked for fun, no trading, no Twitter despite my earlier intentions. Hard to gain perspective when you are always working / thinking about work. Feeling refreshed for first time in awhile.

Investing is a job where you can do a lot of busy work, but get little of value done. What are the biggest time wasters you’ve observed ppl do? Curious analyst vs PMs, keeping in mind some things that are wastes of time to some may not be to others. Some thoughts below:

Here's another Japanese stock that looks interesting as a deep-value idea...

The most recent Q3 results showed an 8.5% revenue increase, and a 46% growth in operating profit.

Margins are over 40%.

It's trading at TBV which protects the downside.

The business is also a little cash machine, with very low capex needs.

The annual reports show a fundamentally profitable, highly cash-generative market leader that is sequentially growing again.

But, it's being given away for virtually nothing.

I don't like it because the ownership structure is too locked up.

No chance of an activist doing anything and a chance of a squeeze out also in play.

This is the type of set up I like, if it wasn't for the concentrated ownership.

Sharing in case any deep-value people here like it.

The business is J-Stream Inc (4308)

@TiagoDias_VC Yeah it is.

Whether or not it gets unlocked or what happens in the future is speculative.

I personally don't like it, but shared in for those that like dirty Japanese deep-value....

@mr_deepvalue Is it?

With no control there is no way to unlock the cash that comes with closing the business and returning the assets to shareholder, so that cash needs to be discounted...

Which it isn't given it's trading at book value.

There are better options I think ie: 5984

@mr_deepvalue Trading at book value. Down 95% since going public 5 years ago. With revenues halving and net negative Cashflow.

Is there even any viable business here?

@orrdavid $CEE, Mostly Polish stocks that benefit from reopening. But also some Russian stocks that can't be traded until sanctions against Russia stop. A quick double if sanctions come off.

Is there some way to bet on the Ukraine war ending soon?

I don't see how it can go on now that Ukraine is able to kill Russian soldiers faster than Russia can replace them.

When you understand how deeply uncomfortable the average human being is with uncertainty, you'll understand why the market frequently misprices things...