Michael Ryan me-retweet

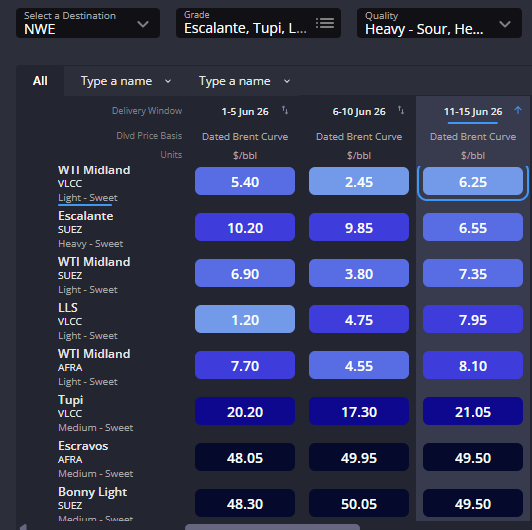

Week seven of the crisis. The US has declared a blockade on Iranian vessels transiting Hormuz, but the situation on the ground remains unclear.

In this episode, @NGCanalyst, @JuneGoh_Sparta, and @SpartaFreight break it down:

> What the blockade actually means for tanker movements and what owners are seeing

> Why Asian refiners are drawing down SPR and commercial stocks for now

> The second-order effects hitting secondary refinery units, from VGO to bitumen

> Where freight rates go if a peace deal lands, and how long it takes for tankers to reposition

The crisis isn't over. Supply chains are fractured. Even if talks succeed, the market faces months of rebuilding.

🔴 Full episode here: spartacommodities.com/insights/podca…

#oott #oilmarkets #crudeoil #freight #commoditytrading

English