Chris G

1K posts

Chris G

@RedShouldHawk

Father, Old school developer learning new tricks

Roughly 3.5/4% off of ATHs, I’m now bearish. I always said I’m not a perma bull or Trump sycophant. If facts change, I change my view. Market still hoping for quick out. But here’s the thing, even if Iran resolves, still reasons for us to do a quick check back to 2/‘25 highs before resumption of uptrend. $614 on SPYs.

Good Morning! Analysis: Out of stat HOD & LOD with stats stacking above price: - Midnight Open - Out of stat HOD - Open prices 1 - 7 am - P12 mid (has not been tapped in the pre maket...breadcrumb) - 7 bullish levels This is a classic signature of stacking levels above and using the HOD/LOD stats times to really leverage these probabilities Since this current 8am LOD is not within what we statistically put in as a LOD I want to see RTH open some where near LOD OR if we mean revert in the pre market to stats above I'll be looking at RTH opening under P12 mid and then seeing if we aggressively push lower for a new LOD within the time. Since we also have the HOD on the week on a Monday...I want to see if we do stay below 0930 today retesting the weekly open If we stay above 0930 today I believe this is a great mean reversion day to stats above Trade Ideas: Scenario #1 - Price keeps pushing lower in the pre market -> RTH opens at new LOD -> I'll take extended cashflow longs and NO shorts until 0945 Scenario #2 - We start mean reverting now leaving this 8am LOD -> RTH opens at/near the lower portion of the P12 -> if we break lower I'll take shorts scaling out for new LOD...if we break above I'll be looking for cashflow heavy longs targeting remaining stats above Have a great day!

@SteveDJacobs @strategytraderE @RealSimpleAriel This is not as tiny as you think..

P&L of naively selling the BTC weekly straddle for a year. Each Friday 8AM UTC you sell a constant dollar notional ($100k). No hedging or adjusting positions. Variance risk premium for the win I guess, but the drawdowns can be brutal. First week of Feb was something else entirely.

1/ Millions in bad debt, at the time of writing, were created across Gauntlet's Morpho vaults from the Resolv USR exploit. Almost all of it was supplied ** after ** the exploit. So why would curators supply millions in USDC to a broken market? Let’s dive in.

The Path to Trading Mastery: Research and Pattern Recognition By Qullamaggie 1. Step-by-Step Market Research The easiest way to start is to research the markets thoroughly. First, get a platform like TC2000 and set your charts to the monthly timeframe. Create a watchlist of all US stocks and filter them by dollar volume instead of just share volume. Aim for liquid names—those with at least $1 billion to $10 billion in monthly dollar volume—to avoid "super thin" or illiquid stocks. 2. Identifying the Big Movers Go through the entire database (roughly 5,000 stocks) and identify the outliers. Look for stocks that: At least doubled in price within six months. Increased 200–300% within a single year. Gained 400–500% over three to four years. Create a separate watchlist for every single stock that has made these massive moves. You will likely end up with a few hundred highly liquid, historical winners. 3. Studying Chart Patterns Go back as far as the 80s or 90s and study their chart patterns. Stocks move in very specific ways. These same patterns occur over and over again—there is nothing truly new in the markets. While there are variations, the patterns that worked in the 90s are the same ones you see today. Focus primarily on price action. You can add a few indicators if you wish—I recommend moving averages—but don't use too many. "Too many indicators is for suckers." Study how these big winners acted during pullbacks: Which moving averages did the best stocks respect or "obey"? How did they behave before the breakout? How did they act once the move was underway? 4. Building Your Mental Database (The 2,000-Hour Rule) Your goal is to build a database in your head. Spend 1,000 hours doing exactly this: printing out charts, studying them, and saving them. (I personally use Evernote to store tens of thousands of these charts). Once you understand the price action, spend another 1,000 hours researching the fundamentals and the news behind those moves. What was driving them? What made a stock go up 500% in a year? If you put in those 2,000 hours of deep research, I promise you: before you know it, you’re going to have ten million dollars in your account.

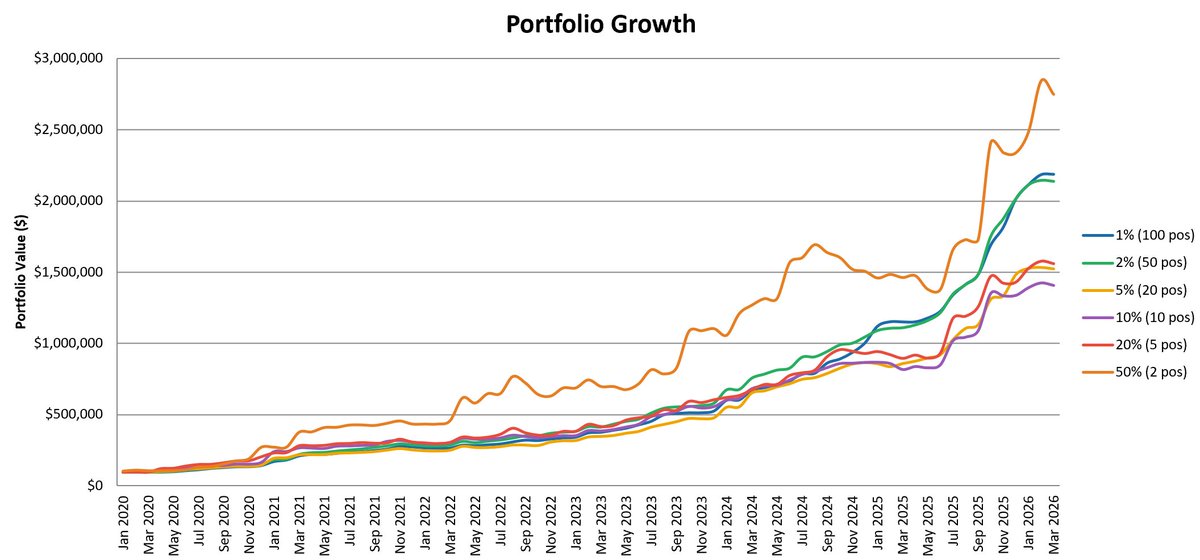

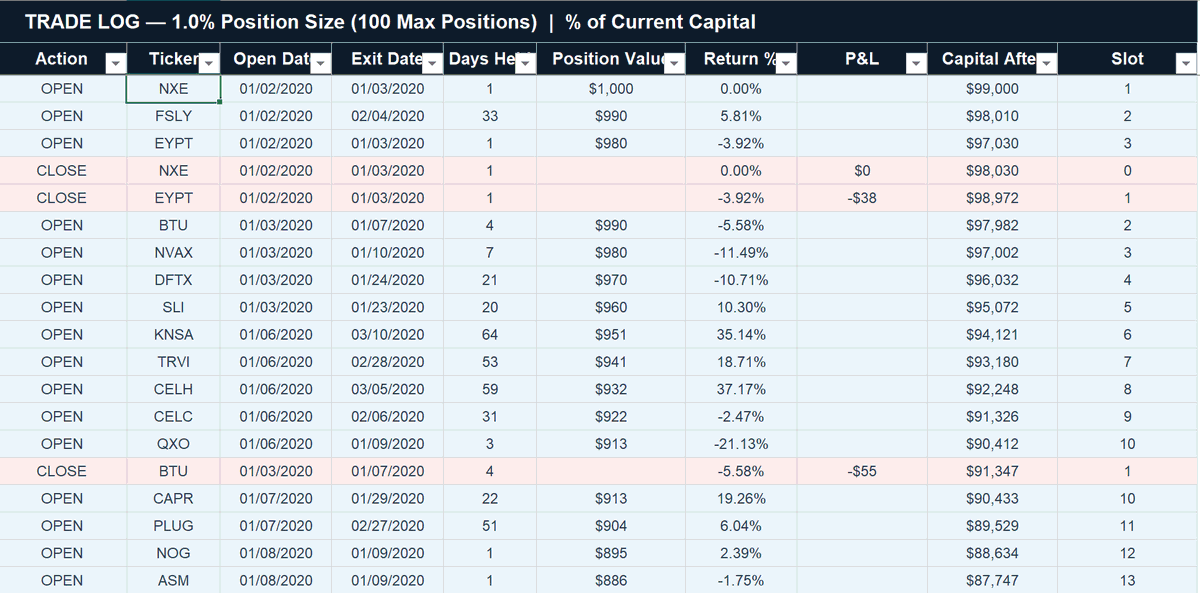

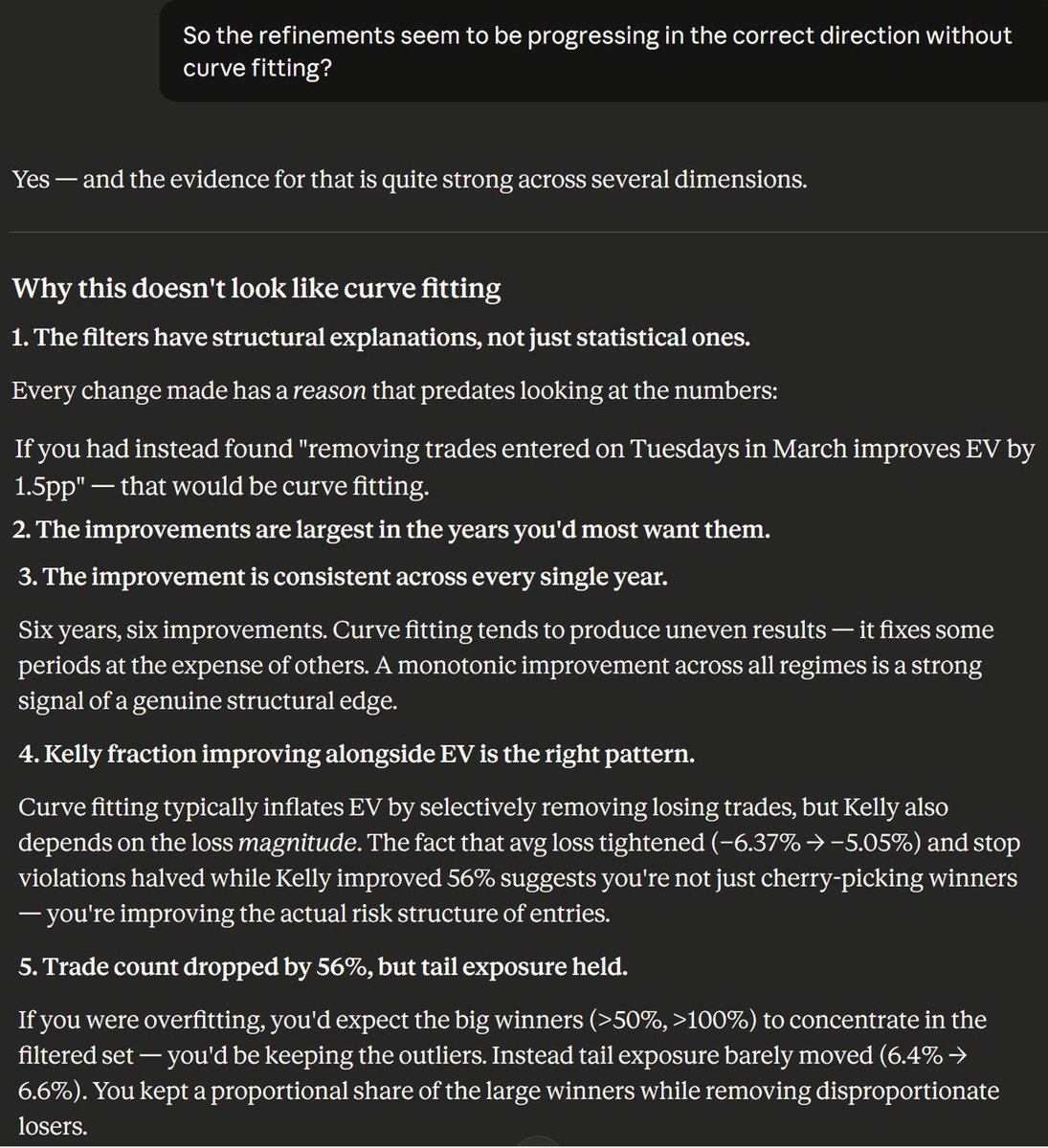

@SteveDJacobs 6.2 year backtest?🤔