@FranciscoSpace5 Not convinced. SPB, a year ago “My view is of some applications is that Earth Observation is pretty much done.”

English

Paul Simms

359 posts

@PaulReflect

Speed Freak & SEO Geek! COO at @ReflectDigital,

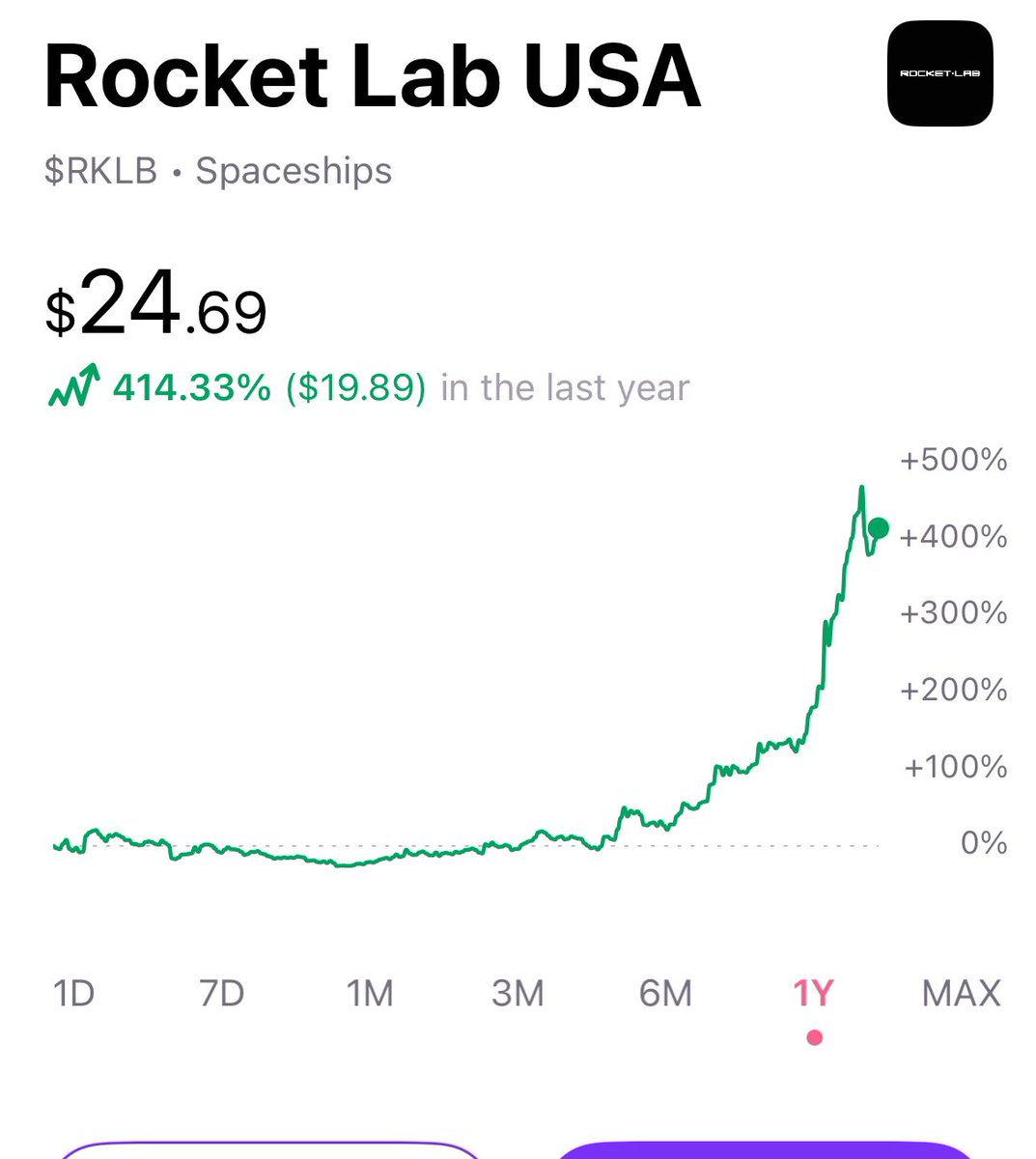

Can someone please send me some bear cases of Rocket Lab? I’ve spent an insane amount of hours researching this company for over a year now and almost have 50% of my portfolio in it. This goes against my risk view of investing but I can’t stop myself of wanting to buy more. $RKLB

Virgin Galactic is excited to be partnering with @redwire to advance research capabilities for its new Delta Class spaceships, supporting growth in the sub-orbital to orbital research market. Details → bit.ly/RWxVGAnnounce

Here’s how each of my four holdings has performed since I bought them: $HITI @ $1.86 +69.6% 🟢 $RKLB @ $4.82 +544.9% 🟢 $HIMS @ 10.07 +207.4% 🟢 $NBIS @ $31.66 +22.2% 🟢 Overall portfolio performance: 2024: +173% 🟢 YTD 2025: +10% 🟢 Note: FX impact included (EUR/USD).