Convexity.eth

305 posts

Convexity.eth

@0xPatBateman

Look at the subtle off white coloring #NGMI

The Waystone Inn Katılım Ocak 2022

291 Takip Edilen44 Takipçiler

Almost 100% De-escalation Priced in to SPX vol...options provide the right to change your mind...

Below, the termstructure of SPX implied vol as of Friday's close. Right next to it, the two trading days before 2/28, when the the conflict began.

It's been a frenetic 2 months, to be sure. SPX 2m realized vol rose from 12 to 16. The VIX surpassed 31 on an intraday basis. The Oil VIX reached its highest level ever, outside of the GFC and Covid crashes. The correlation of crude to major macro proxies surged as crude became the VIX across markets.

The readthrough on the negligible increase in implied vol is that this conflict is quickly fading into the background. Is that too optimistic? Current vol on the SPX, nearly back to where it began, is essentially a free option that expresses doubt that that can happen.

English

English

Moontower #307

🌙math in the car with kids

🌙subway platform riddle for demographics

🌙trader quick math

🌙from straddle to gamma

moontower.substack.com/p/subway-platf…

refs:

@Alpha_Ex_LLC

@_MathAcademy_

English

If you sold long stocks on Friday and bought 10d 3 month calls at equal notional you are going to underperform badly in most right tail events.

Doing it delta neutral is highly likely to get destroyed in most right tail paths.

These sorts of trades need a right tail event something that rivals 4/9/25 taco like melt up. Otherwise they need left tails.

Buying 1-6 month OTM calls is NOT the trade. And my whole feed is doing that trade at spiky vols

English

Convexity.eth retweetledi

Convexity.eth retweetledi

I’d like to contribute $100 directly to Nigel James’ NIL fund next year.

@mooof23 will donate $100 for every RT this gets. This is legally binding.

English

The US is bombing Venezuela in an actual unprovoked attack. Many excuses will be given over the next days: Narco-terrorism; Hezbollah, Hamas, Iran and others "operating" in Venezuela; democracy promotion backed by the Nobel Peace Prize etc.

English

Chamath, you couldn’t grasp munis, CDS, or capital markets if they were lubed up & shoved into your ass. States can’t file Ch.9. CA would raise taxes, strip services, and crush vendors and pensions before skipping a GO coupon.

Your “10-30% tax fraud” point is just All In podcast slop for high finance incels. You’d be bleeding negative carry in a CDS pit and betting against the United States, Fed, and Treasury. There is no “asymmetric 10-1000x trade”. You’re trying to cosplay as Soros but you just look like a poser.

Chamath Palihapitiya@chamath

I think this is the most asymmetric upside bet in the market now. Position yourself smartly and you can make 10-1000x with relative ease. How? Even if politicians try to bury the fraud, the bond market can’t ignore it. Their math will show that even if the fraud is only 10% of total state and municipal budgets, it’s already way too much and should go to paying back debt holders. Right now spreads don’t reflect this and are too tight - ie look at California Credit Default Swaps - it doesn’t reflect any fraud, budget shortfalls or the billionaire exodus. There is little chance these spreads don’t move as the bond market comes back to work and processes the events of the last few days. Now, if instead of 10% fraud, they believe that fraud is 20-30% of all tax dollars, the cost of borrowing will escalate sharply until federal, state and local governments are forced to act. This is when the CDS trade becomes the most asymmetric profit opportunity of our lifetime. Buy the CDS -> wait for politicians to try and bury it -> ie in California -> see the bond market increase borrowing costs -> see the CDS blow out -> asymmetric bet pays off. The takeaway here is that the bond market lives in an alternative and adjacent universe from the politicians and media. The latter group can try to bury an issue but when the former group is asked to fund it, a reckoning happens and the former group always wins.

English

@0xPatBateman it depends on a LOT of things and it's more helpful to think in terms of impact than edge, but here's a place to start:

cfm.com/wp-content/upl…

English

because despite what some options traders incorrectly think customers are not putting on vol trades! they are putting on trades with packaged risk - both delta and vol in tandem - and there is juice in providing to both. moreover, there is a lot MORE juice in the delta piece

sunny@sunny91752655

@DeepDishEnjoyer @VolaDuck @yskewu Could you please explain a little bit more why the book are not hedging? I thought market maker was not in a business to make direction bet

English

@DeepDishEnjoyer Help me picture the size/edge curve for delta and Vega risk? How does the edge each charged for each scale

English

@KrisAbdelmessih What type of gamma exposure are you left with ?

English

@DeepDishEnjoyer I’m going to go with: then no one would make markets on or probably ever use Kalshi because it is perfectly efficient

It’s like paying $1 for a chance to win $2 betting in heads in a coin flip

English

junior trader interview question: why is this a nonsensical argument! provide a token example to illustrate your case

Alex@adf_energy_twt

@DeepDishEnjoyer Spent a few hours with the Kalshi api yday and it appears that contracts are pretty fairly priced. Your contract that costs 90c settles at yes just about 90% of the time. Same pretty much all the way down the curve +/- 2%

English

For the options nerds and galaxy brains, what’s the clean way to express “silver blows off” from here?

Straight naked puts feel like lighting money on fire when IV percentile is this elevated. So what’s the better expression, sell call spreads into the froth, or buy put spreads?

Chart from moontower.ai

English

Convexity.eth retweetledi

The whole thing where Lane Kiffin has to decide on LSU prior to the bowl games seems totally absurd.

English

@intangiblecoins @tether @galaxyhq @maplefinance @Two_Prime @coinbase @hodlwithLedn @sygnumofficial @unchained @ArchLending @glxyresearch Who and what does tether lend too? I thought they mostly bot USTs with deposits

English

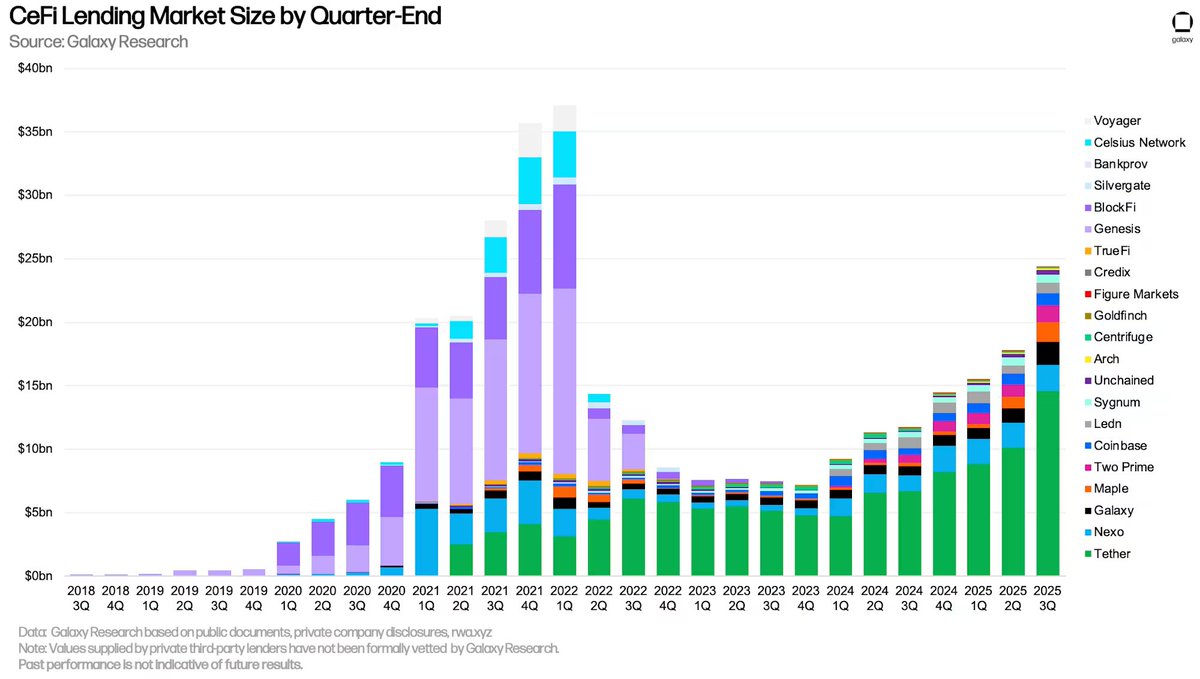

the cefi crypto lending league table is out 👀

crypto lenders had an aggregate loan book of nearly $25 billion outstanding at the end of Q3 2025, the highest since the Q1 2022 peak

proud of this chart and the transparency of its contributors. big change from prior market cycles

tether 🥇

nexo 🥈

galaxy 🥉

maple

two prime

coinbase

ledn

sygnum

unchained

arch

+5 others

English

@Alpha_Ex_LLC No one wants to be short the winner of the AI race and the subsequent move higher that the decisive winner would undergo

English

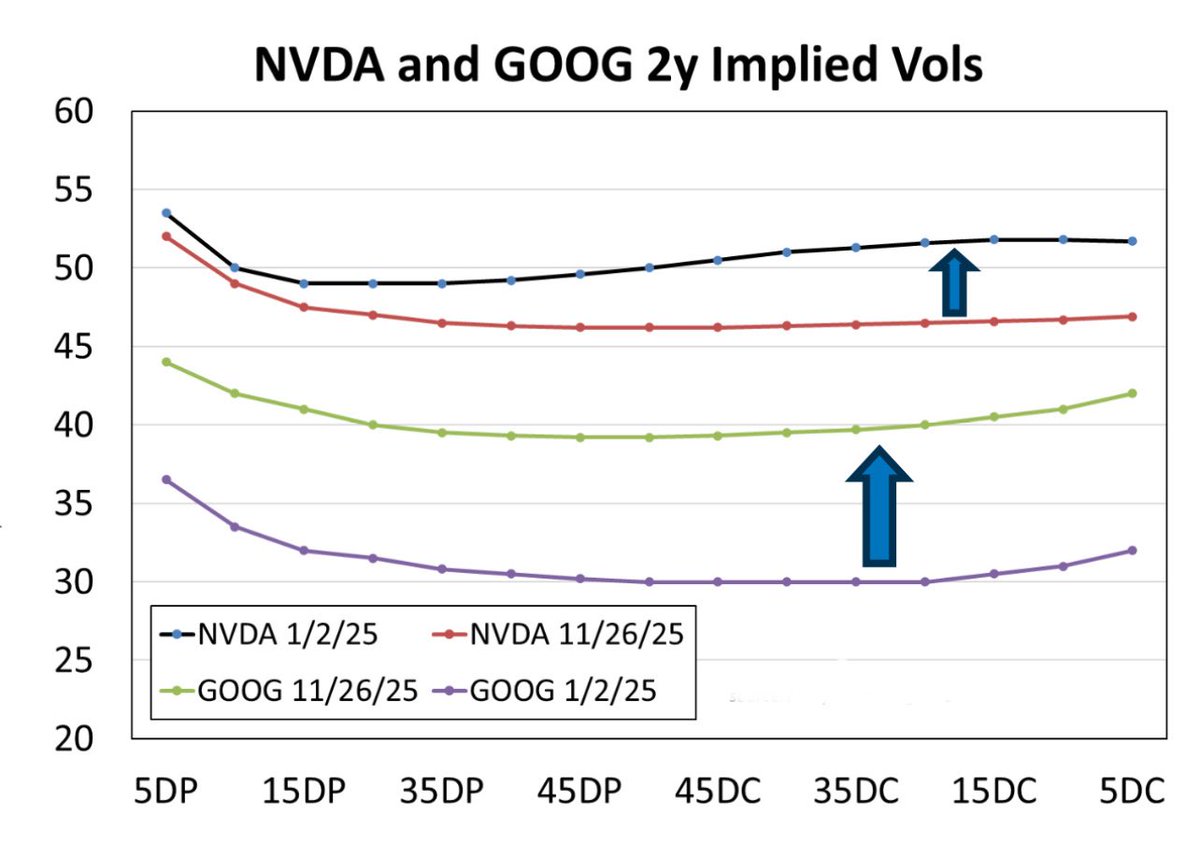

Below, a chart of the 2 year implied volatility by delta for $GOOG and $NVDA …8.3T of combined market cap and both have Aa2 ratings from Moody's with tons of cash and FCF. Credit risk, often a driver of volatility in an equity, is not a thing that comes to mind.

But 2 year implied vol for NVDA is 46, for GOOG it's 39. Why are these long-dated option prices so high?

NVDA's market cap is 40x that of GM and F. Their 2 year implied vols are around 34. The carmakers are rated BBB, the bottom rung of IG. For these companies, unlike the tech megacaps, debt can be an issue.

GOOG is up 68% this year, adding 1.6T of market cap. Two-year 120% implied vol is up 12 at the same time. This is a MASSIVE increase. To give you a sense, a 2y 120% call at 39 vol costs 64% more than it does at 27 vol (at the start of this year).

Why the huge increase in premiums even as the stock is doing so well? My take is that the market cap of the tech behemoths is so large and has increased so quickly that the options market is struggling to provide insurance against loss on them.

The option price may clear at a high level because there’s not enough natural capital ready to bear risk of loss. All else equal, a higher premium is needed to bring sellers to the table.

There's almost an options market equivalent of what's happening in the broader insurance industry ... Premiums are simply higher and it's not necessarily a result of risks that are materializing today. It's more about compensation for future uncertainties and, related, a shortage of capital.

English