robert

237 posts

robert retweetledi

robert retweetledi

Knowledge Snippet

What is a factor?

I feel I never quite understood this idea until I started trading them very actively.

Factors are not anything special, they are just important alphas - NOTHING MORE.

You use factors to say:

Hey these alphas explain a large chunk of the variance and I don’t want to find them again. In crypto that might be a momentum factor so to avoid finding 20 versions of the same effect we use a xs regression to remove our momentum feature from returns and can then test against specific factor returns (returns minus the returns explained by factors basically).

The first factor is always the market, so in equities we take the beta to the S&P500 and then remove the return of the S&P * beta from the asset. This gets the idiosyncratic return. From here we can further remove factors.

In the end, a factor is just an alpha you think explains lots of the variance, there’s nothing “fundamental” or special about it other than that it’s very core to a lot of the things you find.

Alphas depend on what you research. If you are researching HFT and are predicting 1 min ahead you can still have factors. The best known is orderbook imbalance. As I said, a factor is just an alpha which explains lots of the variance and it’s well known that orderbook imbalance is a lot of the variance much like past ret * -1 is a lot of the variance for 1h timeframe. It’s also an alpha you’ll often accidentally find. In the HFT context it’s not like orderbook imbalance explains any risk adjusted returns, it’s simply an effect we’ll often find in our other alphas so hence its important to factor out of returns so we don’t confuse factor exposure (read as factor exposure = alpha we already found) for new alpha.

If you multiply the positions vector to the specific factor returns vector then you’ll get a flat line for an orderbook alpha since it’s already explained but a great line for idiosyncratic or raw returns — basically it shows you the performance in excess of what you know! Really useful!

They also are used for portfolio construction as a regularisation technique and few more applications but I want to explain that alphas and factors are really not that different. Factors are just the ones that we believe the most in and explain the most variance (and are at the biggest risk of being found in other alphas).

English

robert retweetledi

介绍两个我常用的指标(比布林和MACD好用):

Guppy=顾比复合均线(看趋势),

VWAP=成交量加权均价(机构成本锚)。

一、Guppy(顾比复合均线 GMMA)

全称:Guppy Multiple Moving Average

发明人:澳洲交易员 Daryl Guppy

构成(两组EMA):

• 短期组(6条):3、5、8、10、12、15周期 → 短线资金情绪

• 长期组(6条):30、35、40、45、50、60周期 → 长线趋势方向

用法(你说的“看大趋势”):

• 短期组 在长期组上方、同向发散 → 上升趋势强

• 短期组 在长期组下方、同向发散 → 下降趋势强

• 两组 收敛/粘合 → 震荡、趋势弱、可能变盘

• 多周期(周→日→4h→1h)都顺 → 高确定性共振

二、VWAP(成交量加权平均价)

全称:Volume Weighted Average Price

本质:带成交量权重的平均价(大成交量价格影响更大)

公式:

VWAP = Σ(价格 × 成交量) / Σ(总成交量)

特点:

• 通常 日内重置(也可设长周期)

• 代表 市场当日/周期内真实平均成本(机构常用基准)

用法(你说的“关键位置选点”):

• 价格 持续在VWAP上方 → 强势(牛市偏多)

• 价格 持续在VWAP下方 → 弱势(熊市偏空)

• 回踩VWAP支撑/遇VWAP阻力 → 上下车参考点

三、一句话记

• Guppy:看 趋势强弱与方向(多周期均线 ribbon)

• VWAP:看 资金成本与强弱(量价合一的动态中枢)

华尔街观察 Xtrader@cnfinancewatch

对一个企业怎么估值? 一是价值投资估值,估值都是相对的:牛市估值和熊市估值;行业平均净资产收益率对标下的个股相对估值;只有企业生命周期创造的现金流总和估值是大致可以绝对…… 二是技术走势估值:反弹比例、突破后上涨比例、箱体横盘压力承托位、通道压力承托位…… 三我更倾向于用上面两者结合后的“时间轴”相对空间估值。一定要计算时间。

中文

robert retweetledi

robert retweetledi

Agent 正在批量制造不会思考的人。以前不思考是有痛感的,你会写不出来、做不下去。现在 Agent 把所有卡住的环节都跳过了,给你一个面面俱到的结果。痛感消失了,思考也一起消失了。

到处下载别人的 Skill、问AI建议、让 AI 直接给结论。看上去很勤奋,其实全程没有动过脑子。

我看 Dovey 写 skill 才知道差距在哪。她定义的是:每一步的判断标准是什么,什么不做,优先级怎么排,输出锚定在哪。这些全是她自己的判断,换个人用同一个 Agent 写不出来。

Agent 是放大器。有判断的人用它放大判断,没判断的人用它放大无知。

Dovey "Rug The CNY" Wan🪐@DoveyWanCN

看不同人train agent, 差异巨大, 可能总结下来是 系统思维 vs 任务思维的差异. 系统思维的人会定义问题, 有架构的能力, 先架 (scaffolding) 后构 (interaction): 这件事的边界是X,最佳输入是Y,预期输出是Z,失败条件是W, 测试置信区间是I. 任务思维就是很单项的I/O“帮我做这个事, 我来验收” 所以还停留在把LLM当作更好的搜索引擎和对话框的水平

中文

TIL that in the 90s, HTTP defined status code 402: "Payment Required," reserving space in the protocol for digital payments.

Over the next 30 years, the internet evolved with closed payment systems instead.

And now, x402 revives that original idea: a universal open standard for sending value across the web for apps, APIs, and now agents.

@base and @coinbase join the x402 foundation today along with @cloudflare @awscloud @google @Shopify @Visa @Mastercard @Microsoft and more.

Coinbase 🛡️@coinbase

English

robert retweetledi

robert retweetledi

robert retweetledi

🚀 In just 2 weeks, $OWL is soaring:

🌟 No.1 on Binance Alpha: 85%+ of daily volume

🥉 No.3 in market volume, just behind $BTC & $ETH

🔥 Trending #1 on CMC & CoinGecko

…More ⬇️

We’re just getting started 🦉

English

robert retweetledi

Breaking: massive movement detected in the sky 🌪️

The $OWL rush is coming🦉💥

English

robert retweetledi

New X Launches: @Owlto_Finance & @spacecoin

🏆 Prize Pools:

5,724,098 $OWL

134.4M $SPACE

Register to claim by Jan 24, 10 AM UTC: web3.okx.com/boost/x-launch

Claims go live on Jan 24, 12 PM UTC. Open to Cedefi users as well.

English

$OWL bridge is LIVE 🚀🦉

You can now bridge $OWL between @BNBCHAIN ↔ @ethereum

👉 owlto.finance/owlbridge?from…

Welcome to the $OWL Roads!

English

robert retweetledi

Trading is Math:

Math is the language of profitable trading because successful trading is fundamentally about managing probabilities, edges, and risk — and math is the only language precise enough to describe these things accurately and consistently.

Here are the main reasons:

1. Edge exists only as a statistical/probabilistic phenomenon

→ No math → no way to prove or measure an edge exists

2. Risk management is pure mathematics

Position sizing, stop placement, R-multiples, maximum drawdown, ruin probability, Kelly criterion, volatility scaling → all math

3. Profitability = Expectancy × Trade Frequency × (1 – Commission/Slippage drag)

If you can’t calculate expectancy mathematically, you don’t actually know whether you’re profitable or just lucky

4. Most market patterns are illusions until quantified. Beautiful chart patterns become profitable (or unprofitable) only after statistical validation (win rate, avg win/loss, profit factor, Sharpe/Sortino, etc.)

5. The market speaks in distributions, not predictions

Profitable traders think in terms of

• probability distributions

• fat tails

• skewness

• serial correlation

• regime changes

All mathematical concepts

English

robert retweetledi

1/ $𝐎𝐖𝐋 𝐢𝐬 𝐠𝐨𝐢𝐧𝐠 𝐥𝐢𝐯𝐞.

Today marks a major milestone for Owlto Finance: the launch of $OWL, our native token.

Read to learn more about our story 👇

English

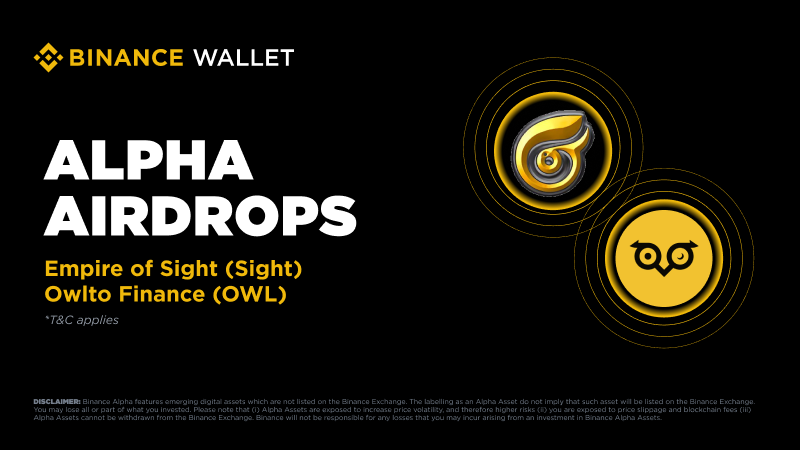

币安 Alpha 将成为首个上线以下项目的平台:

1 月 14 日 Empire of Sight (Sight) 空投

1 月 15 日 Owlto Finance (OWL) 空投

符合条件的用户可于 Alpha 交易开放后,前往 Alpha 活动页面使用币安 Alpha 积分领取空投。具体详情将另行公布。

敬请关注币安官方渠道,及时获取活动最新动态。

中文

Binance Alpha will be the first platform to feature:

Empire of Sight (Sight) on January 14

Owlto Finance (OWL) on January 15

Eligible users can claim their airdrops using Binance Alpha Points on the Alpha Events page once trading opens. Further details will be announced soon.

Please stay tuned to Binance’s official channels for the latest updates.

English

Don't feel bad if you can't swim

You might be the bird that was born to fly

GM, $OWL 🦉✨

Binance Wallet@BinanceWallet

Binance Alpha will be the first platform to feature: Empire of Sight (Sight) on January 14 Owlto Finance (OWL) on January 15 Eligible users can claim their airdrops using Binance Alpha Points on the Alpha Events page once trading opens. Further details will be announced soon. Please stay tuned to Binance’s official channels for the latest updates.

English