Nick Davis

925 posts

Nick Davis

@123ndcd

Parent. Lawyer. Optimist. Free thinker. Random mixture of mundane and profound Tweets on law, politics, family. #StrokeSurviver

Altrincham, UK Katılım Ocak 2011

1K Takip Edilen374 Takipçiler

Ratcliffe is incoherent - all of the oil and gas we produce here in Britain is sold at the global market price. No amount of oil produced here can in that case save us a single penny. Importing fossil fuels does not mean we pay more. Drilling in the north sea will take years to deliver globally priced fossil fuels and Rosebank will cost nearly £3 Bn in tax payer subsidies to it’s Norwegian owners - and….none of the oil will land here in Britain. So what sense is Ratcliffe making here, other than to shareholders in Rosebank and other oil companies.

This is another fossil fuel crisis and we can’t solve it or help ourselves at all - by pouring more oil onto it.

telegraph.co.uk/business/2026/…

English

@jacques_davey I think out of the 9k it subsidies the science/medical courses.

English

The larger problem is that crooks at universities charge 9k for an English Lit degree. I doubt student below will have had more than 3 hours contact time a week. Many complain about the loan system but you are being ripped off at every level.

BBC Newsnight@BBCNewsnight

“I graduated from my undergraduate degree last summer… and I have £90,231 of student loan debt.” Gina Tindale, 22, who went to university from a low income background, says the necessity to take out a larger maintenance loan has significantly added to her debt. #Newsnight

English

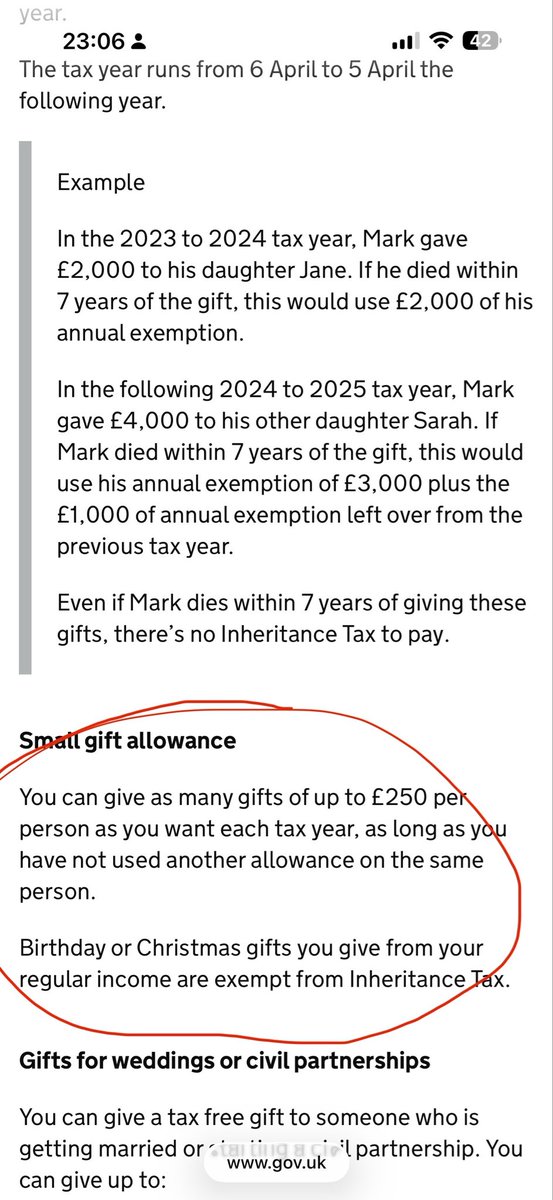

@MartinSLewis Please deal with the fact you can do what you want with your spare income it's not restricted by gift limits , my dad has a surplus income of £25k pa but he says he can only spend £100 on birthday presents as it's the law, his savings just increase exponentially

English

Do you have practical questions on Inheritance tax?

I'm planning to cover it in detail on my podcast this week (with specialists). So please suggest your questions by reply here (or email martinlewispodcast@bbc.co.uk) and podcast producer Simon will collate.

English

@NJM71 It's interesting that individuals receiving the new State Pension may have a £5,000 threshold for non-ISA cash savings but that there is a more restrictive £500 limit for non-ISA dividends.

English

There's a distinct difference between 'Basic State Pension' and the 'New State Pension'. I expect better from the Chancellor when talking about a cohort receiving £125+ billion in state pensions. Fully expect pensioners with small private pensions to be kicking off about this 👇

David Robbins@David_J_Robbins

A person who just gets the basic state pension would not be paying tax regardless of the November 2025 Budget announcement, because the full BSP will remain below the personal allowance for some time. The Chancellor means that she will exempt pensioners from tax if if they just get the full BSP or the full New State Pension (which is on course to exceed the personal allowance from April 2027), with no private income or State Pension increments. She's not the only politician to use the term "basic state pension" as though the NSP had never been introduced. A bit of loose terminology may not matter, but the point of calling the BSP the basic state pension was that there were other state pensions that some people received on top. That remains the case with early cohorts of NSP claimants, some of whom receive protected payments. And the value of the NSP as a % of average earnings is similar to what BSP was at its early 1980s peak. But if NSP becomes fully mature without Parliament changing the system again, NSP will be the only State Pension that anyone receives. Its name in statute - simply "State Pension" will then be more appropriate.

English

@LauraTrottMP Creative arts students are paying £9250+ a year. So those students are actually subsidising science/medic courses !

English

The IFS have been clear that 3/4 of the value of loans funding creative arts courses have to be written off. There is nothing progressive about sending young people on courses that won’t get them jobs and leave them with no prospects.

English

English

As someone said to me recently, universities impoverish themselves and the towns and cities they're meant to be part of by attacking arts and humanities subjects @UCU @UniversitiesUK @timeshighered

English

@Moshe_89 @FlottaConsultin @DrLukeCraddock Not quite.

Science/medical degrees are expensive to run. Arty degrees are not. The arty students were subsidising the science/medical students.

English

@FlottaConsultin @DrLukeCraddock You miss the point.

They arent repaying their own loan, they are repaying other peoples' loans. The ones who did dud degrees that earn peanuts.

English

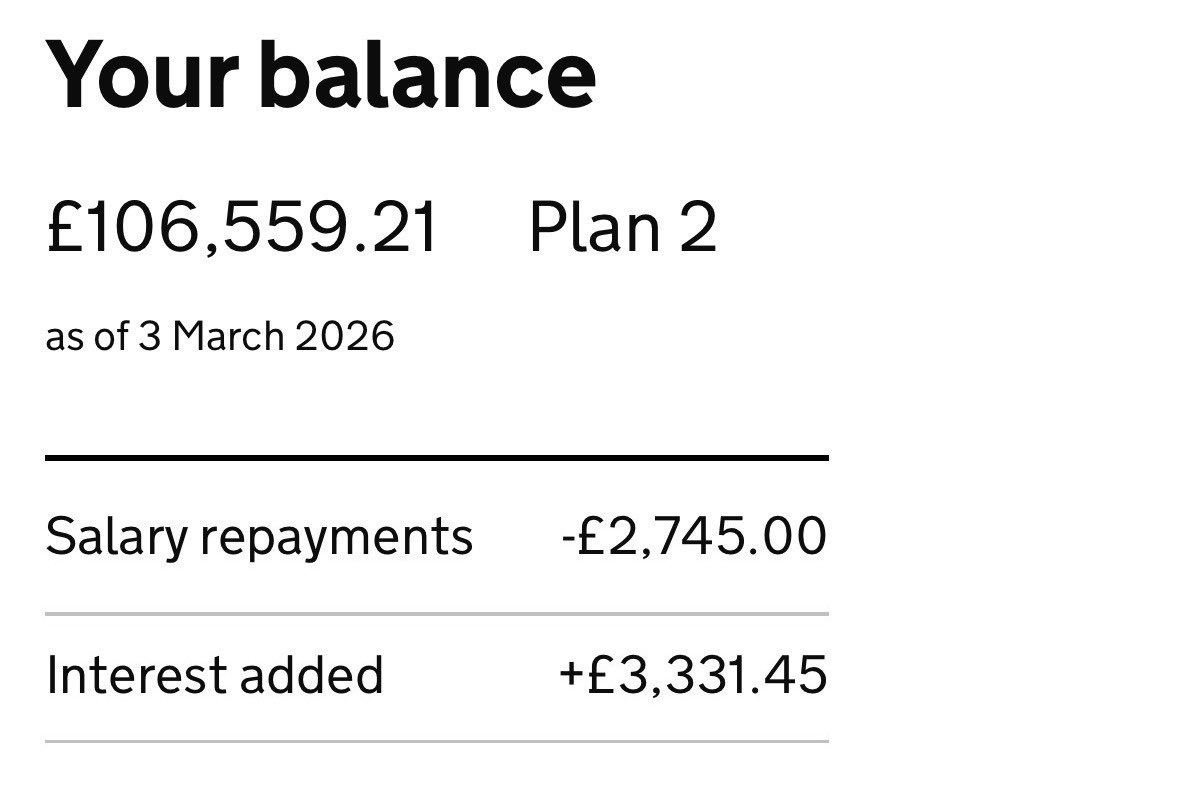

My plan 2 student loan as we come to the end of this tax year. Another year of an increasing balance despite repayments.

English

@BKMacC @paullewismoney Exactly !

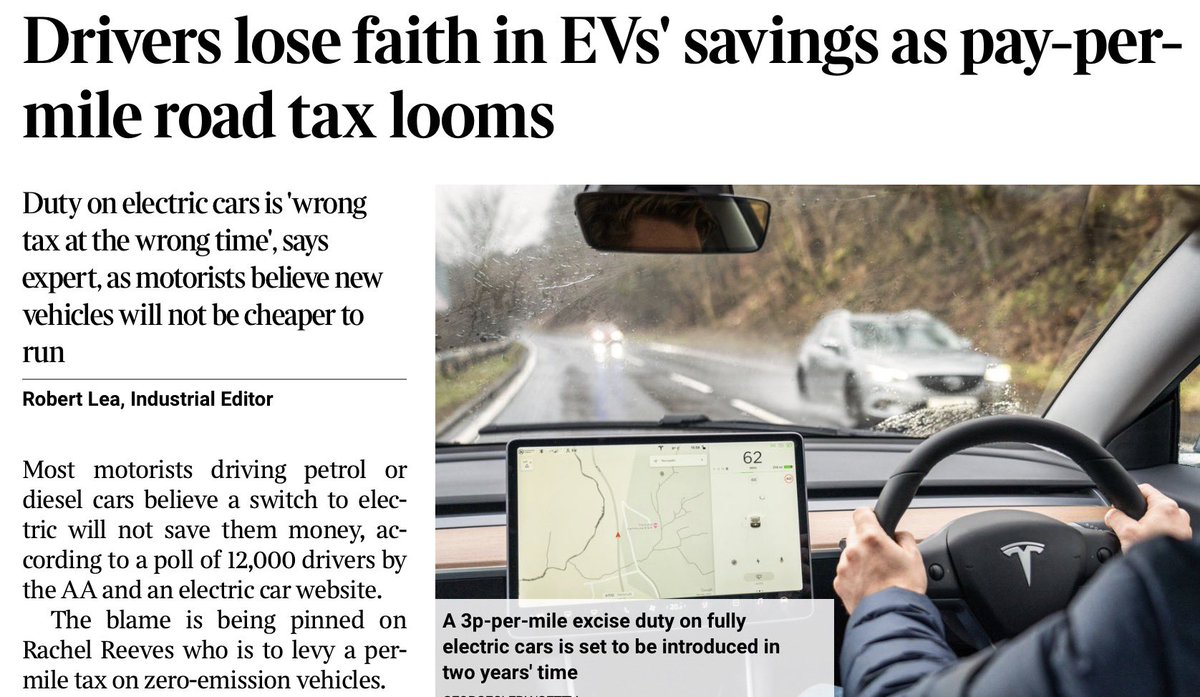

Remember the duty is increasing from September and December and March !

gov.uk/government/pub…

English

Electric shock - new tax threatens to make EVs more expensive to run than fossil fuel cars bit.ly/4tVfveK

English

@RyanShorthouse I thought the art courses actually subsidies the science/medical courses.

English

Universities currently bear no risk for the fees that they charge. This is because the government subsidises the non-repayment of student loans.

This is the main driver of why the subsidy is so high and taxpayers’s are paying too much for HE, and why too many students are on the wrong courses.

The Chancellor @RachelReevesMP needs to make universities take on more risk for the fees that they charge. Say, charge a levy on those that produce a disproportionate number of graduates with low earnings who will have loans which are ultimately subsidised.

This will make universities focus on recruiting and nurturing potential, rather than just treating students as income.

English

@nickhillman @billwells_1 @LibbyHackettJMI @UniAlliance @KateOgdenEcon @MartinSLewis However at that time lenders offered loans (from memory) about 6 or 7%.

I’m skeptical about the point about ‘actually lost value in real terms’. I am not aware any lender base on such terms.

English

@123ndcd @billwells_1 @LibbyHackettJMI @UniAlliance @KateOgdenEcon @MartinSLewis When inflation was over 10%, interest on loans was capped at something like 8% so they actually lost value in real terms.

English

One of the major problems for policymakers wanting to reform student loans is the lack of polling among Plan 2 borrowers. We don’t know what most of them want. The campaigners are mainly much better paid than average (eg MPs) so are probably not typical. 1/n

English

@billwells_1 @nickhillman @LibbyHackettJMI @UniAlliance @KateOgdenEcon @MartinSLewis I’m surprised that nobody seems to carefully read s.22(4) Teaching and Higher Education Act 1998 (as amended)

English

@nickhillman @LibbyHackettJMI @UniAlliance I think a bias to early repayment gives even more weight to what to me looks like a technical mistake - (prescribed) contributions only start on graduation but interest starts from loan receipt.

[Also shows importance of no. not size of repayments.] @KateOgdenEcon @MartinSLewis

English

@nickhillman @LibbyHackettJMI @UniAlliance The difficulty is the large loan is such that most students suspect the repay period will cover their working lives. As a result the incentive is to take the largest possible loan, and to repay the minimum.

English

@LibbyHackettJMI @UniAlliance Make of this what you will. I’m not sure what to make of it myself but it is the only polling I’m aware of on such issues. Original source is: unialliance.ac.uk/wp-content/upl…

English

@merjerper @BenZaranko @KateOgdenEcon I wonder whether it needs wider objectives. For example, tax deductible student loans for those who have children.

English

@BenZaranko @KateOgdenEcon What about allowing it to be tax deductible? Allowing the loan to be paid gross seems like a sensible thing to me although would have weird fiscal effects

English

There are lots of student loan proposals flying around. This stuff is complicated and contentious. Fortunately @KateOgdenEcon has stepped in as the fifth emergency service to explain what these proposals mean, who would win/lose, and how much they'd cost.

Institute for Fiscal Studies@TheIFS

NEW: How would proposed changes to Plan 2 student loans affect graduates? 📗 We’ve modelled proposed reforms from the Conservatives, Lib Dems and Rethink Repayments and more in our new report: [THREAD]

English

@nickhillman @KateOgdenEcon @TheIFS I would be interested to ‘scrunch’ the numbers if changed the compound interest to simple interest.

English

Brilliant new paper from @KateOgdenEcon / @TheIFS. The Rethink Repayment proposals on student loans wd cost £12bn for 1 cohort (& there are 11 Plan 2 cohorts in England). This is a harder issue than the campaigners want you to think ifs.org.uk/publications/o…

English

@AppleSZS @MrRBourne Unfortunately your estimate for £4-7k for accommodation is not correct.

English

@MrRBourne 10k uni fees

£4-7K in accom (average)

£5k living (if that’s even possible)

Who’s gonna pay you £19-22k after tax as a part time job as a student? For 3-5 years

Just so chaotic , and non sustainable.

Even if you could save before hand, can you actually?

English

Unpopular opinion: people who go to university should pay for their own education, including paying a market interest rate if they borrow to do so.

Politics UK@PolitlcsUK

🚨 WATCH: Kemi Badenoch clashes with Martin Lewis on her plans for student loans

English

@Newmanoid68 @MartinSLewis This is the perverse system.

If you have enough to pay off your kids’ loan, it would be probably sensible to use it for a deposit for their first home.

English

@MartinSLewis So if I can help my kids to pay it off , should I ? Your advise was always not too. Which I’m sticking too at the moment

English

Student Loans: the furore is over Plan 2, but new starters (Eng) are on even worse Plan 5!

My last two posts have been about Plan 2 student loans (Eng & Welsh students who started Uni 2012 to 2023). Those who started since Aug 2023 (Eng) are on Plan 5, which is even more expensive for most...

As while the interest rate is lower (set at the RPI rate of inflation as opposed to up to RPI+3%) you start repaying at income of just £25,000 and you repay for up to 40 years.

The combination of this means it's predicted many middle earners will repay in total 40% or 50% more than those on Plan 2 for the same degrees.

And that's before we get to the fact that the English household income assessment for maintenance loans has been frozen since 2008. So students start to lose entitlement from family income of just £25,000/yr (if it'd risen with inflation it'd be around £35,000 to 40,000).

That means, for example, a child of a single parent who is earning little above min wage won't get the full living loan, never mind dual earning parents.

And don't get me started on the issue of 'parents partner moves in'.

The problem is the system is so complex very few understand it, including quite a few politicians I've met, And of the politicians who do understand it, they tend to use confusion marketing, to make the lifetime cost more expensive while focusing on superficial headline changes (eg Plan 5 change focused on lower interest).

English

@ryan_wain @MartinSLewis As an alternative, consider change compound interest to simple interest.

There is some precedent, for example in judgments incur simple interest.

English

Hard to argue with @MartinSLewis. Literally.

Student loans are essentially a 9% tax rate on graduates. Any policy offering immediate relief should treat them as such - either by lowering the % rate or increasing the threshold at which they’re paid.

Politics UK@PolitlcsUK

🚨 WATCH: Kemi Badenoch clashes with Martin Lewis on her plans for student loans

English

@seledka_vodka @KemiBadenoch Perhaps the system should consider change the interest: changing from compounded interest to simple interest.

There is a precedent, for example interest on judgments are based on simple interest.

English

Martin - you say that @KemiBadenoch's proposal to cut Plan 2 student loan interest is "too late for most" - that because most graduates never clear their loans, reducing the interest rate won't change what they actually repay. I think you're right on the maths. But I think your alternative - raising the repayment threshold to £40,000 - solves the wrong problem.

The graduates who never clear their loans are not the victims of this system. They're its beneficiaries. A low earner who borrows £53,000 and repays £25,000 over 30 years before the rest is written off has, effectively, received a £28,000 education grant from the taxpayer. That's not an injustice. That's literally a subsidy.

You seem to want to give these graduates even more relief by raising the threshold, which amounts to a targeted tax cut for people who are already net recipients of public money. While it is a progressive cost-of-living relief measure, it has nothing to do with actually fixing student loans.

The actual injustice sits with middle earners. A graduate on £45,000 who ends up repaying £132,000 on a £53,000 loan - that's where compound interest does real damage. These are teachers, engineers, mid-career NHS staff. Not rich. Just earning enough for the interest to snowball, but not enough to escape quickly. They repay two and a half times what they borrowed. That is the scam.

Kemi's proposal targets exactly this group. Capping interest at RPI means these graduates clear their loans years earlier and save £40,000-£50,000 in lifetime repayments. On the other hand, your threshold increase proposal would redirect the same budget toward people who were never going to repay in full anyway.

Basically, the choice is between fixing a genuine structural penalty on aspirational, middle-earning graduates, or handing a broader but shallower subsidy to people the system already treats generously.

I think @KemiBadenoch has the better instinct here. The loans that "feel like a scam" are the ones where you pay back far more than you borrowed - not the ones where the taxpayer quietly absorbs the loss for you.

Martin Lewis@MartinSLewis

The problem with @KemiBadenoch proposal to cut Plan 2 loans interest rates is it is too late for most. While I've long campaigned against above inflation interest rates on student loans, so much interest has already been added to people's accounts that cutting it now, while psychologically appealing, won't reduce by a penny the amount lower and middle earning graduates repay. While it would be nice to do, assuming they're not planning to spend unlimited funds, or say reduce the actual debt owed, in my view a far better use of the same funds would be to massively increase the repayment threshold (the opposite of what @RachelReevesMP is doing with the disgraceful and damaging freezing of the threshold). Plan 2 loans were always set up so that most would not repay in full over the 30 years before it wipes. For them it works like a hefty 9% additional tax above the repayment threshold (though psychologically it's a nightmare for many to see the interest grow and grow even if they won't pay it). The only people who would financially benefit from lowering interest rates to inflation at this point, would be those who earn enough to clear what they owe in the 30 years before the debt wipes. Currently that's predicted to be only the highest earning (or lowest borrowing) 20% to 30% of graduates, but with lower interest maybe it'd be 30% or 40%. For the rest, the bulk of lower and middle earning graduates, lowering interest rates won't help. They'll still repay the same for the next 30 years. Yet if you used the same money to increase the threshold so repayments were say 9% of everything above £40,000 (and index link that) rather than the current £28,400. Graduates would have up to £1,000/yr more disposable income each year. Plus this way many of those who didn't get a graduate premium (ie financially benefitted from their degrees) wouldnt be paying.

English

@daisyeastlake You could ask the Secretary of State for Education whether she could finally fill in the blanks in her 2 June 2023 article in The Times thetimes.com/uk/politics/ar…

English

EXCL: Ministers are in discussions about easing the burden of student loan repayments on graduates facing crippling interest charges on their debt

While the Treasury insisted it would not U-turn on the terms of the loans, senior government sources confirmed that preliminary discussions were taking place behind the scenes about possible measures to make the loans fairer

Senior government sources said that ministers “knew they had a problem on their hands” and that an increasing number of MPs had raised the issue after a campaign run by The Sunday Times

Another said ministers “wanted to see what they could do” to reduce annual payments and interest rates. “This was not a problem that we created but one we inherited from the Tories,” the source said. “But we realise it is something that we need to try and address.”

One Labour MP said they knew of “dozens” of backbench MPs who wanted the government to reform the system. The MP added: “We were outfoxed [by the Conservatives] on the social media ban. Kemi is going to try and outfox us again on this. Have we learnt our lessons?”

In @thetimes 👇

thetimes.com/uk/politics/ar…

English