Burry just called NVIDIA "the North Star, Orion, the whole Milky Way" — and warned about the bullwhip.

He's pointing at customer concentration that's "off the charts."

The thesis: hyperscaler demand is training-phase, temporary. When training ends, NVDA's $75.25B data-center quarter shrinks fast.

He's not wrong about the concentration.

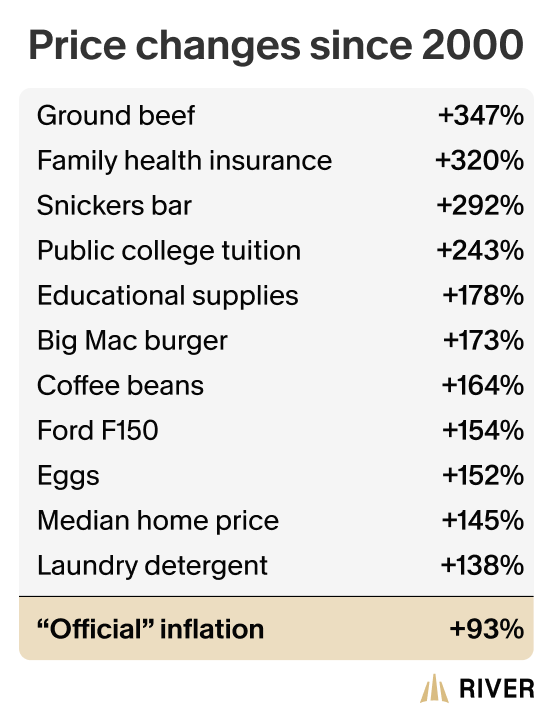

Apollo's Slok (cited in Burry's post): 87% of VC funding is now AI. In 1999, internet was 38%.

But the bullwhip story has a problem.

Today, while Burry was publishing, two things happened.

Micron CEO Sanjay Mehrotra confirmed HBM4 is sold out through 2026 at fixed prices. The company can only fulfill 50 to 67 percent of key-customer demand. Tightness extends "well beyond 2026."

And Micron signed its first-ever 5-year supply contract with a major customer.

Five years. Locked. Mid-supercycle.

That is the opposite of bullwhip behavior. Companies caught in a bullwhip cancel orders the moment demand wobbles. They do not sign 5-year contracts at the top.

The second data point: Korea Customs Service, first 20 days of May.

Total exports $52.7B, +64.8% YoY — biggest May on record.

Semiconductors $22B, +202.1% YoY.

Computer peripherals +305.5%.

Exports to China +96.5%, Taiwan +110.4%.

That is what real demand looks like in the rear-view mirror, not a forecast.

So the bezzle exists. Burry is right that it does.

But the canary is not NVDA.

NVDA already gets punished — 4 straight post-print drops, closed $215.33 today. The skepticism is in the price.

The actual canary is two-fold:

1. The day Micron stops signing multi-year SCAs. That is the signal hyperscaler conviction broke.

2. The 10Y yield through 5%. We are at 4.56% today, spiked to 4.67% on May 19. BofA's Hartnett (same Flow Show note that warned tech weighting goes past 48% after SpaceX/OpenAI IPOs) named the unwind mechanism: "bond vigilantes on manoeuvres."

When duration buyers go on strike, AI capex gets re-marked alongside everything else. The NVDA print date stops mattering.

The trade.

Long $MU $754.61. Stop last week's low $700. BofA price target $950. Risk-reward ~1:2.6, in a stock whose buyer just signed a 5-year supply contract.

Pair with $TLT puts ($83.91, near the bottom of the post-2023 range) — the bond-vigilante side bet.

The Burry hedge, for purists: own MU + Jan'27 $SOXX puts (his actual position). SOXX printed a new 52w high today ($534.79); vol is finally cheap enough to BE the hedge instead of the trade.

Two things to watch — not earnings.

Micron's next 5-year SCA announcement.

The 10Y print on the next CPI.

Until those flip, the bullwhip is the wrong frame.

English