InvestingFailure

56 posts

My portfolio is now built up of 5 core sectors that I think will do well in the next 2/3 years

I’ve got AI/Data centers, Photonics, Drones, Teleheath and Space

The only sector I think I could do with adding is a critical metal/mineral stock

Based on the size of my port anymore than 5 stocks is counter intuitive

Full update portfolio breakdown on Monday as always 👍🏼

$IREN $AAOI $ONDS $HIMS $SIDU

English

Now that I’ve sold $TE I’m going to do some serious rebalancing of the portfolio

I’m going to reassess current positions and decide where I want to put my capital

I’m investing for the long term, like I’ve always said I’ll change my stance when the thesis changes and for $TE that moment is now 👍🏼

English

@mcF_dan @BitcoinAIGuy This is why I’m not selling despite down -25%

English

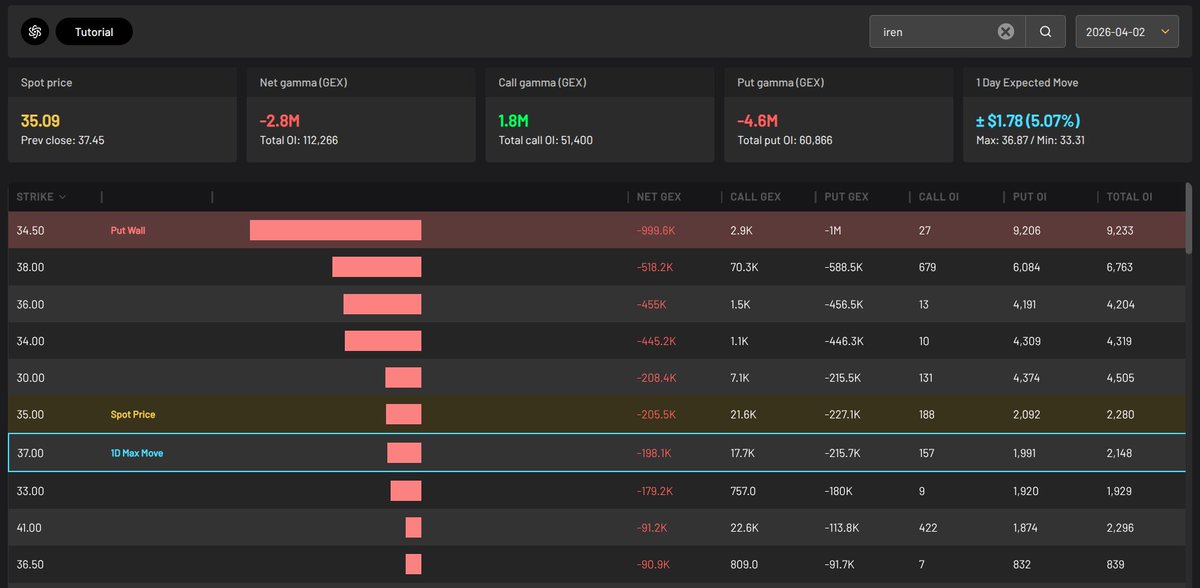

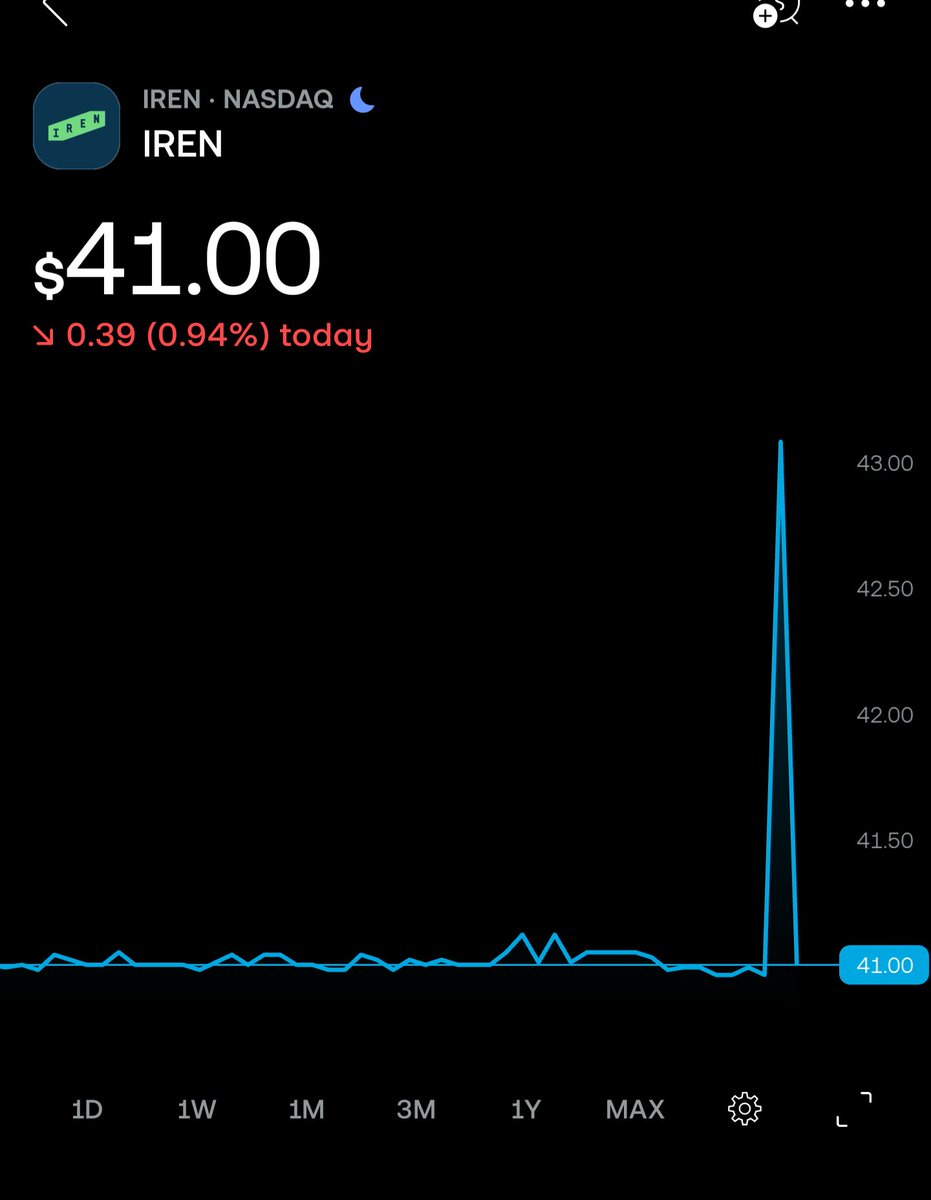

At ~$11B market cap, $IREN is below net asset value.

That implies:

•Zero value for AI cloud growth

•Zero value for contracted revenue

•Zero value for pipeline

I don’t think this buying opportunity will last long.

English

@TradingTh3Trend @aleabitoreddit Where did 40bn come from

English

@aleabitoreddit How would you feel if they sign a $40+ Billion hyperscaler in April for their sweet waters site.

English

$IREN filed to dilute $6,000,000,000 at a $11.7B MC.

That is not noise.

This is Iren's way to monetize their 4.5GW capacity by selling all those new shares onto the open market.

If you want some history on how this turns out:

Look at $BKKT that crashed 99% with Mike and $IREN board of directors history with excessive ATMs. Or his recent company $ASST.

It’s accretive to the company and executives: Because it wipes out all retail shareholders and they can always issue SBC.

So they don’t actually care what stock price it needs to be at to sell.

After they’re finished, they have $6B in new cash to use for scaling without paying interest.

But the reason why convertible notes with interest, and $NVDA funding balance sheets is much better for retail capital:

Is because it doesn’t wipe out retail equity to achieve this. Because at this point $IREN looks like the $AMC of datacenters with a dwindling moat, and looming $6B in shares sold into the open market.

Reason I post about $IREN is because

- people dismiss a $6B ATM as “Noise”

- it’s one of the most popular retail “buy the dip” companies that they’re buying into a $6B dilution machine

- people still don’t understand the risk at all.

- the amount they have now is not enough to finance GPUs/GW capacity monetization.

- they likely will have to use the ATM, it’s not “optionality”

Again: I have zero positions in the company.

I’m just warning retail investors that this ATM structurally wipes out your equity appreciation by how structural mechanics of $6B+ ATMs work.

Because $IREN likely needs to sell new shares at any price to monetize their GW, otherwise there would be zero need to file it.

Executives actually don't need to care because they can make up for stock price dropping by issuing SBC like $SNAP.

If you have to wonder if your equity gets wiped out from an excessive ATM:

There are better longs out there than $IREN.

Bony@BonyBallf2

@aleabitoreddit @Kaizen_Investor I feel like you are way too much focused on the dilution. If they excecute their GW pipeline properly the dilution is just noise. Demand for available GW is so massive and i do think most data centers will have massive delays and also though time to get financed. So imo $iren ☝️

English

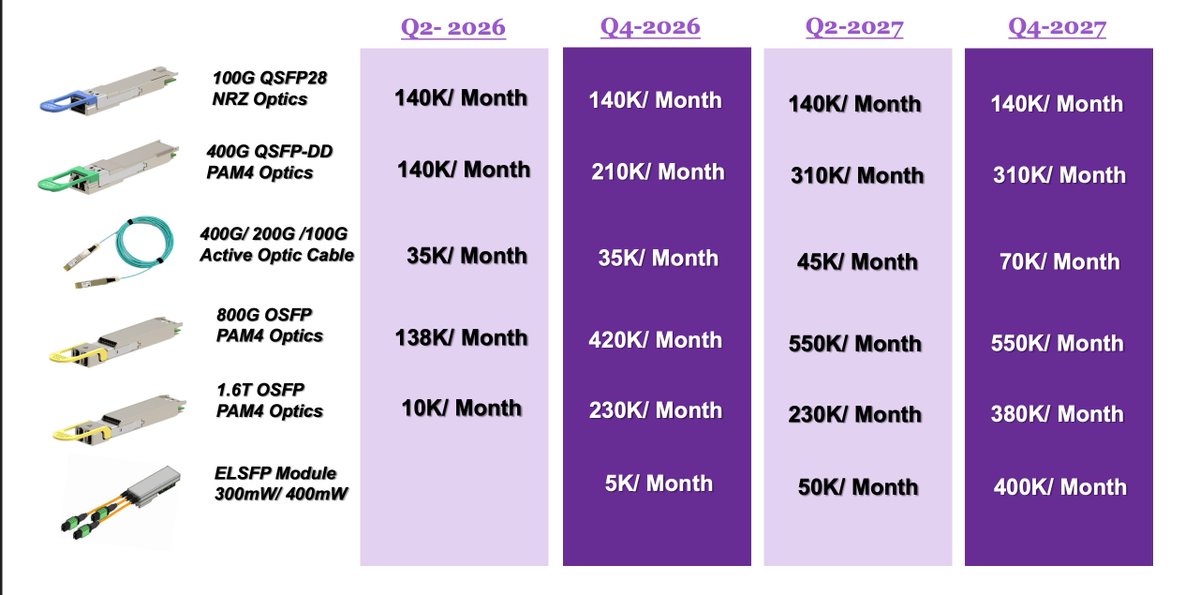

$AAOI Just said 'hold my beer'.

They heard people say there's no way their capacity could hit 500,000 units/m by the end of 2026.

How about 650,000/m by then?

Or how about 930,000/m by the end of 2027?

Check out the image below.

It lays it all out.

For 800G + 1.6T.

They are not backing down from their projections.

They are actually significantly increasing them

When the market realizes the revenue implications here, it will be a field day.

There's also a lot of big X accounts posting about AAOI and it also tagged a key level today. This does not play into my investment thesis at all, but it does influence volatility.

I will write a full debrief on the presentation asap.

They still have to execute and deliver. 100%. The execution risk is still there. But the fact that they are really pushing this capacity ramp is encouraging and it's hard for me to believe it's all smoke. But time will tell.

Shoutout to @Hartik__ for putting this breakdown on my radar

English

InvestingFailure retweetledi

Young people have dreamed for moments such as these.

Brew Markets@brewmarkets

The S&P 500 is on track for its worst month since 2022.

English

InvestingFailure retweetledi

So my 10x moonshot $AXTI ended up landing on the moon.

If you felt like you missed the rocket:

-> $SIVE is my personal favorite next 10x AXT moonshot at today's prices.

-> $AAOI already up 4x since I've mentioned it, but I still think it can 4x again from these levels.

If you want to play a bit safer:

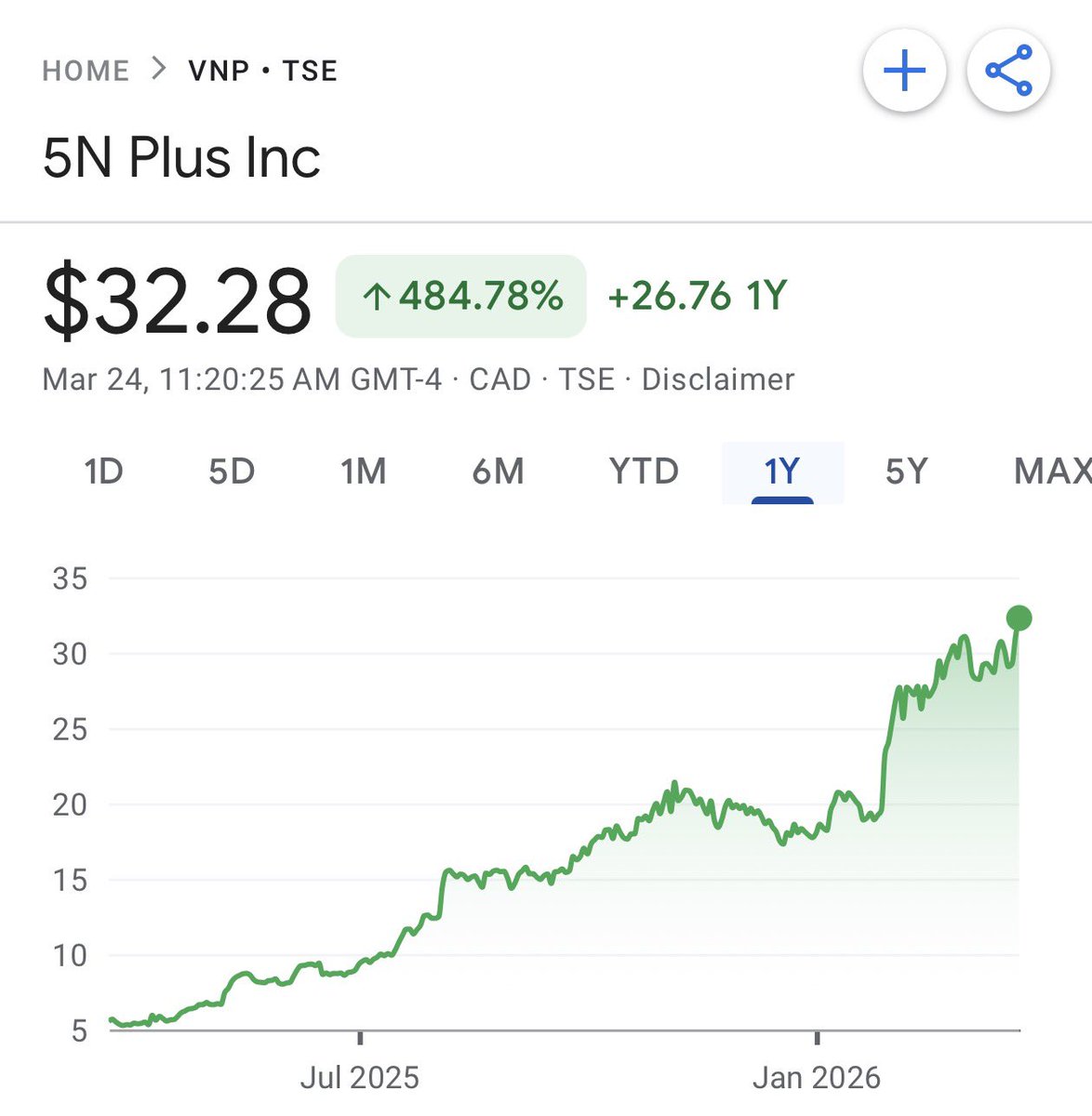

-> $VNP is the Western $AXTI

-> $SOI is the $AXTI for silicon photonics/CPO, but it hasn't really ramped up yet.

-> $IQE is more binary based on restructuring.

-> $TSEM, $LITE, $COHR are the steadier compounders.

I haven’t mentioned $VNP (5N Plus) much yet but it’s genuinely one of the most important companies in Western supply chains as the counterbalance to $AXTI.

Basically it supplies: indium, germanium, gallium, tellurium, bismuth. Solar cells for LEO. Substrate feedstock for photonics.

There's always more opportunities in the market!

Serenity@aleabitoreddit

$AXTI has now reached the legendary status of $69.69. Was expecting close to 10x returns in a year and half, not a few months… Everything from $AAOI to $SIVE are ridiculously outperforming. As for AXT valuations at $4B? Is it overvalued. Yes. Would hyperscalers pay $10B to secure their AI buildout? Yes. Lot of these bottlenecks can’t be valued with traditional metrics.

English

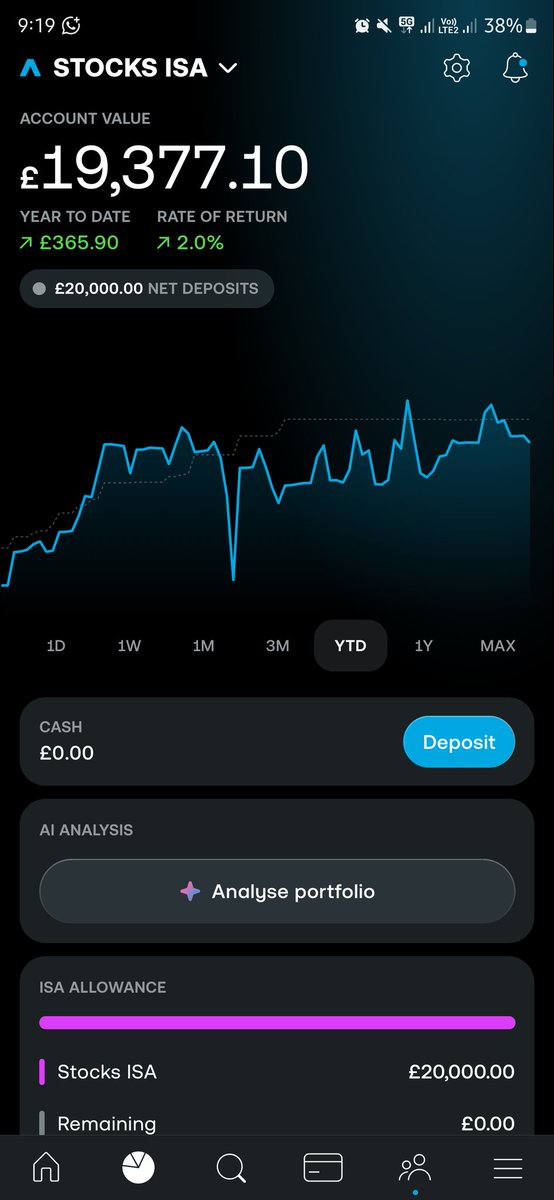

Portfolio update week 8 - Road to 100K💰

Balance: £ 16,978.37 💸

YTD - 10.7% 👀

Current Positions ⬇️

$TE - 2000 Shares - $6.11

$IREN - 150 Shares - $48.60

$ONDS - 131 Shares - $9.73

$HIMS - 40 Shares - $23.96

$ASTI - 50 Shares - $6.57

$IQE - 750 Shares - £0.22

Another turbulent week in the markets but no changes to the port, a drop from last week but it feels as though many green weeks are on the horizon

$ONDS crushed earnings and raised guidance for 2026, $TE announced earnings for next week and $IREN is setting itself up for a huge rally

$HIMS & $ONDS remain my 2 priority positions to build out and scale as they’re both LT investments for myself 👍🏼

Ryan@ryansfinance

Portfolio update week 7 - Road to 100K💰 Balance: £ 18,811.36💸 YTD -0.2% 👀 Current Positions ⬇️ $TE - 2000 Shares - $6.11 $IREN - 150 Shares - $48.60 $ONDS - 131 Shares - $9.73 $HIMS - 40 Shares - $23.96 $ASTI - 50 Shares - $6.57 $IQE - 750 Shares - £0.22 Added another £1K to the port this week, scaled up $ONDS & added $HIMS both of which are 2 positions I’m desperate to build out and scale Holding strong on my $TE shares going into earnings and will reevaluate when we have some more clarity but I’m expecting great things $IREN is being held long term & plan to push this up to 200 shares once I’m happy with the other 2 positions Now up to 18% of the way to the 100K mark 👍🏻

English

@realjoncooper @AST_SpaceMobile ASTS end of year market cap predictions?

English

$ASTS 🛰️🇺🇸 🌐 With a current market cap of $34 billion, I encourage all investors and fund managers to seize the opportunity we have with @AST_SpaceMobile. The upcoming Space X IPO will elevate the entire sector.

The AST SpaceMobile mission to connect the unconnected from anywhere on Earth will be achieved. The subscriber base, through our MNO partnerships, has the potential to reach into the billions.

Our dual use technology for government applications will maximize investor returns and help build a powerful moat around a business with the potential to serve the largest subscriber base in the world!

Polymarket@Polymarket

BREAKING: The SpaceX IPO is now projected to close above $2 trillion after the announcement of TERAFAB. 55% chance.

English

This is why I’m working so hard to get to the £100K mark

Getting to £10K took a lot of learning and discipline but I got there, the last 9-10 months have helped me build the habits I need to stay consistent

The hard work will pay off, getting to that £100K will be a huge milestone, I want to be there by the time I am 25

2 more years of investing until then, I’m 18% of the way there 👍🏻

mon@moninvestor

The first £100,000 is the hardest because you are building everything from nothing. Your income is smaller, your investing capital is limited, and progress can feel slow. But this stage is where the real skill is built. You learn how to save, how to stay patient when results take time to appear, and how to think independently when markets move against you. Compounding is still weak at the beginning, so the numbers may look small, but the habits and mindset you develop during this phase are extremely valuable. Once you cross that first £100k, things begin to change. Your capital starts working alongside you, small percentage gains begin to matter, and you start to feel real momentum building. The early years test your commitment, but the investors who stay consistent through that phase are the ones who eventually experience the real power of compounding.

English

InvestingFailure retweetledi

Markets have got it wrong when they say:

"When Everyone Digs for Gold, Sell Shovels"

You know why?

The real alpha comes from:

Bottlenecking the Shovel Sellers.

Substrates/EML lasers in photonics from $AXTI and $LITE.

to

$SNDK to Sk Hynix for NAND/DRAM are those bottlenecks.

And they end up individually more profitable, than the investors who crowd around shovel sellers like $NVDA.

The saying should go:

"When Everyone Digs for Gold, Profit off the Materials at jacked up prices that the Shovel Sellers need to Sell the Shovels".

English

The sentiment surrounding $IREN rn is at an all time low, dilution and the lack of new deals doesn’t change anything for me

The thesis still remains in tact and until that changes i will continue to invest and hold

If I was worried about volatility I wouldn’t have 86% of my portfolio in only $TE & $IREN

Sentiment will shift and we’ll heed back to ATHs when a new deal is announced 👍🏻

English

InvestingFailure retweetledi

$AAOI is extraordinarily exciting.

There is a chance this re-rates to $35B+ or higher next year from $7B if they can execute.

I'll give a TLDR of the landscape and a simple explanation why:

Assembly:

-> Lasers from $LITE / $COHR -> assembles from blueprints -> then sell the transceiver.

$FN (Asia) -> ~$20B MC.

~$4B projected revenue, 12.4% gross margins.

Design + Assembly:

- Buys lasers from $LITE / $COHR, design the 800G and 1.6T -> then sells the transceiver.

Innolight (China): ~$84B MC

~ 46.2% gross margins, ~$11B projected revenue

Eoptolink (China): ~$50B MC:

~$5.3B projected revenue

Lasers:

- Creates the Lasers to sell to Innolight + Eoptolink or creates the lasers + design to give to $FN to assemble for them/.

$LITE, $55B MC:

FY 2026 est. ~$2.91B (~40% margin)

(they also do more than lasers, eg. $LITE with Cloudlite does design -> $FN to assemble based on blueprints too, but not the entire process end-to-end).

( $COHR and $AVGO do this too)

_ _ _ _ _ _

Entire supply chain (laser chips, design, and assembly)

$AAOI $7.5B MC:

Midpoint 2027 est. ~4.5B ARR (40% margin)

- $AAOI makes the laser (like $LITE), designs it from ground up (like Innolight), then assembles it like ( $FN ):

And it's primarily made in the USA.

-> $AAOI does the $LITE / $COHR lasers in-house

-> $AAOI does Innolight/Eoptolink transceiver design.

-> $AAOI does $FN's assembly.

This is possible margin expansion/optimization across the board.

Best of all they're projected to leapfrogging $LITE's FY2026 projected ~$2.91B revenue...

By doing: ~4.5B ARR mid-year 2027

When you look at $AAOI's $7.5B Marketcap.

And you look at each part of the photonics supply chain from $LITE at $55B to Eoptolink at $55B.

Anyone can see the raw, unadulterated upside if they execute.

Serenity@aleabitoreddit

High conviction long: $AAOI. I genuinely think this could easily be a 3x by next year. Nvidia funded $COHR, who does Malaysia manufacturing for 800G/1.6T. $LITE uses FN in Thailand for volume production, and has it's own manufacturing in Thailand. I will keep hammering this home but Applied Optoelectronics is only pure Made in America, optical transceiver play. Again, the two "American" optical companies outsourced it to Asia, while $AAOI spent the years building up capacity and fabs in Texas. Nvidia funded both $COHR and $LITE just now to build out a US-version to insulate its most critical supply chain from geopolitical risks. But guess who already has the supply chain setup and is years ahead in that regard? $AAOI. $LITE ($55B) FY 2026 est. ~$2.91B $AAOI ($7.1B MC) H2 2027: $4.35B ARR. $AAOI will actually leapfrong Lite FY 2026 projections if management executes (and with ~40% gross margins). Once again. $AAOI ($7B) will leapfrog $LITE ($55B MC) entire 2026 revenue projections if they deliver their projections. $FN over in Asia, 2026 projections are actually around the exact same as AAOI. ~4.39B revenue off 12.4% gross margins. And it's a $20B MC (with much lower margins) Even if $AAOI hits 70% of their target, it's likely to be heavily re-rated way past it's current marketcap. TLDR: Hard to see downside with $AAOI at these levels, especially with 3-4 hyperscalers (likely $GOOGL, $MSFT, $AMZN) wanting to buy up any capacity it can make for years out. And with $GOOGL not going the CPO route. $AAOI leapfrogs $CRDO, $ALAB, $LITE, and others in growth + benefits from photonics theme vs. copper (from the first two). $AAOI remains an asymmetrical 1Y high conviction as long as management delivers.

English

$IREN getting all the Marketing aligned.

Very excited for $IREN Holders.

Remember Dan does not get pay until $IREN well beyond 120s

One of the best Team in the space. You are lucky if you are holding this company and know about this space.

This is a hell of an opportunity!!

Daniel Roberts@danroberts0101

Proud to team up with the Swans. We might be building AI cloud infrastructure around the world today - but Sydney’s where $IREN started.

English

@endless_frank Holding 84 shares at 89.51. Wish I had more cash to buy the at the 70's tho

English

$ASTS I said 88, high 87.81 AH and no report yet. Can’t do much better than that. Give us 6 or more completed satellites and we’re ahead of our launch schedule with satellites to spare for the New Glenn ramp in the back half. 🅰️🚀🙏🏼

Endless Capit🅰️l@endless_frank

$ASTS I could see $88 today then gap up tomorrow and back over $100. Island gap reversal time. They def sandbagged info for MWC. They pretty much locked down most of the European market. Space X and AST and nobody else. This is a real duopoly in a huge addressable market.

English