Sabitlenmiş Tweet

Alex

1.8K posts

Alex

@AlexanderKim120

South Korea FICC manager with structured products(IR, Credit, FX, and Commodities) & Prop trading(cross-asset view)

대한민국 영등포구 Katılım Şubat 2023

318 Takip Edilen3.1K Takipçiler

생각할게 많았던 금통위.

생각보다 UK쪽 신고전학파 느낌이 강했음.

특히 외환경로에 대한 부분, 기대인플레이션과 retail price(RPI)에 대한 접점, 그리고 외부효과에 대한 설명, GDI에서 Terms of trade를 녹인 해석 등이 꽤 인상에 남았음. 이게 UK쪽 색깔이 강하다고 생각한 부분임.

앞으로 기존 BOK와 꽤 다른 색깔이 나올 것 같다는 기대감이 들었음.

Alex@AlexanderKim120

오늘 처음 신현송 총재의 기자회견이 있습니다. 아무런 편견없이 지켜보고자 합니다. 행동을 크게 바꿀 수 있을만한 이야기를 하기에 부적절한 시기이기 때문에, 그가 갖고 있는 사고와 철학 그리고 논리에 대해 무장해제 상태로 들어볼 예정입니다. 희망하는 바는 (향후 금리 운용 방향과 무관하게) 본인이 표현하시고 싶은 바를 가감없이 표현해주시는 것입니다.

한국어

Alex retweetledi

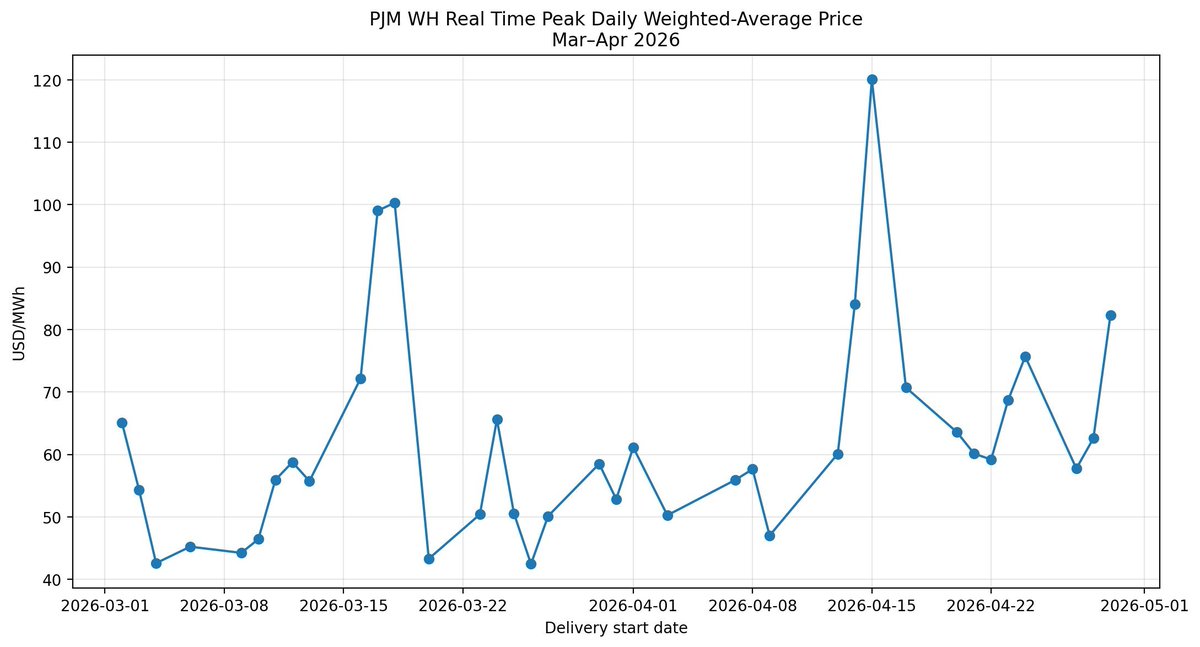

Treasury sanctioned Persian Gulf Strait Authority.

Unsanctioned inbound tanker flow is now dead on arrival.

Even if an MOU is signed, they don’t have a legal mechanism to pay the “toll” fee.

English

We are gradually opening up our delta exposure. We are assuming a maximum growth rate of 2.7% and a CPI of 2.8% for 2026, factoring in two rate hikes within this year and 1.2 hikes in 2027.

Since we already have plenty of cash on hand, we have sufficient capacity.

We see the worst-case levels for the 3-year KTB at around 3.95% and the 10-year KTB at around 4.45%.

This outlook is based on a combination of two assumptions: first, the probability of a U.S. rate hike passing through this summer, and second, that December WTI futures will sustain the $85 level driven by an endogenous market rebound, looking past headline noise.

Alex@AlexanderKim120

<중간점검> 내 동료 트레이더들은 잘 알겠지만 나는 국고3년 캡을 3.80, 10년 캡을 4.20으로 픽했었음. 그것도 6-7월내에 도달 가능한 캡라인이라고 봤음. 꽤 많은 딜러들이 '현재 레벨이 기준금리 몇번을 프라이싱'하고 있다는 식으로 말할 때마다 왠만하면 호들갑 떨지 말고 좀 더 기다리자고 꾸준하게 말했음. 그리고 X에서도 꾸준히 밝혔지만 나와 우리 데스크는 그 방향을 고집했음. 중간에 상황이 맛탱이 가서 이 레벨에 도달할 순 있다는 생각을 했지만 이렇게 빠르게 올줄은 솔직히 생각을 못함. 지금은 좀 고민이 많아지는 자리임. 레벨 접근을 내가 극혐하지만 지금 이 상황이 비정상적인 포지셔닝이 몇겹이 쌓여서 왔기 때문에 더더욱 고민이 많아짐. 평소 내 스타일이었으면 너무 과도하면 매수를 했겠지만 지금은 좀 조심스러움. UK politics, BOJ개입, 다카이치의 추경없음 발언이 뒤집힐 것 등은 모두 예상에 있었음. 이건 꽤 보수적인 가정이 아니라 내 경력상 그리고 꽤 오랜 기간 집요하게 리서치해온 바에 따라 충분히 내릴 수 있는 결론이었음. 그리고 하나 확실하게 보이는건 2Q KR GDP도 좋게 나올 것이라는 점임. 특히 지금 시장이 예상하지 못한 분야의 기여도가 꽤 될 것이라 생각함. 여기까지는 내가 그래도 컨빅션을 갖고 다른 데스크들과 다르게 'wait and see'를 고수할 수 있는 타임라인이었음. 그 다음이 문제임. Iran사태와 앞으로 Oil의 역학은 훌륭한 친구들의 오랜 도움을 바탕으로 선별 가능한 시나리오들이 존재함. 하지만 딱 하나 컨빅션을 갖지 못하는게 있음... 그 고민을 좀 더 해봐야겠음..

English

The BOJ has already exhausted almost all of its intervention capacity. Since the current supplementary budget and the upcoming 'Honebuto' policy (Basic Policy on Economic and Fiscal Management and Reform) in June are already anticipated, the BOJ will not halt its rate hikes within the year, even if immediate data proves unreliable. Ultimately, everything hinges on the BOJ's terminal rate, but I believe they will approach 2% over a long-term cycle rather than in the short term.

English

@AlexanderKim120 I'm curious why? Psychological barrier due to fear of BOJ intervention? Wouldn't fiscal actions like this one weaken their credibility?

English

@JJNews002 not much room for now. The worst level would be 162 i guess

English

@yieldsearcher you can find video Bank of Korea youtube and 11:10am SK time

English

@nevergonnaeasy @brandonjcarl we can seen the dramatic movements within a month lol

English

GPU spot prices continuing down from their spike.

Brandon Carl@brandonjcarl

More GPU price normalization via @OrnnExchange. Easing is across H100, H200, B200 and A100.

English

It's raining in SK right now. It's super early in the morning, and every day when I wake up at this hour to go to work, I usually just read the news feeling completely numb. There's really not much to laugh about at this time of day. But seeing this made me crack up laughing. hahahahaha

Barak Ravid@BarakRavid

הנשיא טראמפ אמר כי הוא לא בטוח שכדאי לו לחתום על הסכם לסיום המלחמה עם איראן, אם סעודיה ושאר מדינות המפרץ לא יצטרפו להסכמי אברהם. ״הם חייבים לנו את זה״, הוא אמר

English

From a conservative perspective, my view is that between 2026 and 2030, the supply-demand balance is unlikely to break down immediately unless there is a massive supply shock.

However, considering well-known factors such as supply inelasticity, utilities' uncontracted long-term volumes, and the timing of hyperscalers' secondary supply depletion, I have concluded that purchasing options in the 1Y-2Y segment is the most rational strategy at present.

If I proceed with the actual trade, it is highly likely that I will execute a diversified investment spread across the 1Y, 2Y, and 3Y tenors. I am currently waiting on standby, as the 3Y option requires desk approval.

English

@AlexanderKim120 Do you see uranium upside so soon? I am bullish too but thought it would take longer as many countries have yet to build or restart their reactors

English

I'm planning to trade CMX U3O8 Futures Options OTC. We will be targeting the 1-to-2-year maturity range, as I believe there is an upside potential for the price to reach around $150. This is a move I've carefully considered for quite some time. I am confident that no other FICC desk in South Korea is attempting anything like this. We are constantly striving to upgrade our business, pushing it in a more advanced and progressive direction.

Recently, we've also been developing our own electricity hedging products for the Korean market. I work on a sell-side FICC desk, and our true expertise lies in 'product development.' For nearly 20 years, most FICC desks have been stuck doing little more than interest rate or credit structuring.

To widen the gap between us and the rest of the market, we have taken on numerous new initiatives throughout 2025 and 2026. We are actively seeking out blue oceans in this space and allocating lot of resources to them. I have drawn a great deal of inspiration from the many highly respected traders on X.

I always have the utmost respect for them.

English

@acemoney21 Oh nope.. cash settlement.. I got quoted 2yr 5 delta vol near by 30%.. quite expensive..

English

@AlexanderKim120 Are they physical contracts like do they settle and you would potentially take delivery if you’re a dealer?

English

Alex retweetledi

US and OPEC+ exports are slowing down.

Japan and SK normalizing, now the global oil balancing act is solely resting on China's inland inventories which allows them to reduce their imports and refinery runs.

Utterly unsustainable and inventories will eventually draw. Chinese imports are currently less than during peak Covid lockdowns.

English

npr.org/2026/05/26/nx-…

It is still too early to definitively say that DJT has politically collapsed within the Republican Party. Of course, the situation could change at any time.

Alex@AlexanderKim120

Are you saying that DJT has lost his grip on the Republican leadership? Isn't that a bit of a premature prediction?

English

@acemoney21 So I give up the vols... pursuing long-term investments.. lol

English

Alex retweetledi

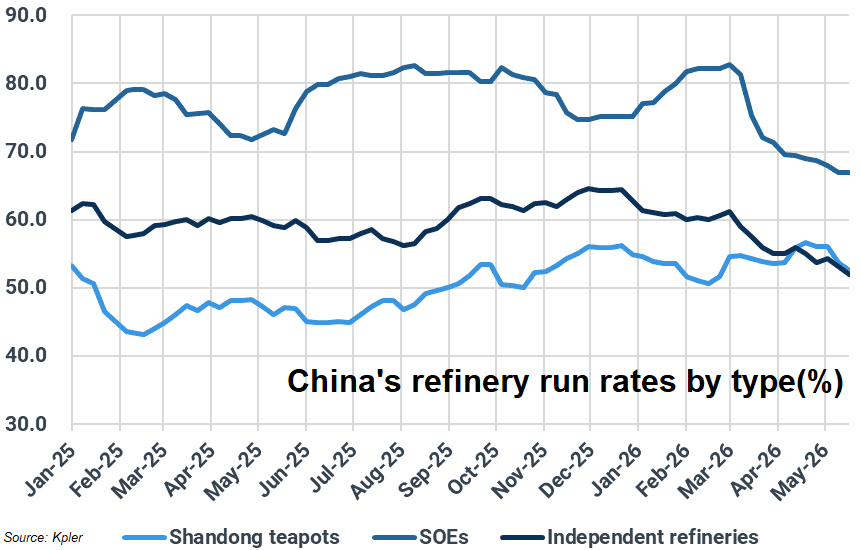

I’ve been grinding away trying to map out China’s recent crude plays, but after going through today's report, I have to hand it to OIES—they scripted the plumbing way better than me.

Here is my quick breakdown after running through their print, alongside the Chinese refinery throughput chart to help connect the dots.

-

Three months into the Hormuz crunch, and Beijing is completely blindsiding the market with its crude playbook. A heavyweight that easily sucked in 11mb/d over the last five years just saw its import prints plunge to 9.3mb/d in April. Now, the forward data says May and June seaborne arrivals are about to crater straight into the gutter at 6.5mb/d.

Instead of running its usual playbook of panic-dumping the SPR to backstop the market during a supply crisis, Beijing just completely cock-blocked refiners from touching the strategic vaults, only greenlighting commercial stock draws.

To make it worse, refiners aren't even willing to bleed their own commercial inventories, while state traders are acting like total penny-pinchers—happily flipping premium WAF cargoes back into the market and hoarding dirt-cheap Russian barrels instead.

This is a complete 180 from the 2021 power crunch, when Beijing panicked and ordered everyone to grab supply 'at any cost.' The heavyweights and policymakers in Beijing clearly think they can outmaneuver this supply shock and keep the economic damage locked down by playing a few smart, tactical micro-levers.

China’s true red line for freezing out imports is hardwired to the scale of their run cuts. If they try to copy-paste their five-year average throughput of 14.1mb/d, the exact moment seaborne arrivals drop below 9.2mb/d, they’re trapped—they either have to open the strategic taps wide or start chasing expensive market barrels. Instead, chopping runs by 5% down to a 13.4mb/d baseline is hands-down their most realistic, long-term survival play.

In this setup, if domestic crude extraction and pipeline taps keep humming, they can easily coast for a few months without taking a single economic hit, even with seaborne prints scraping a measly 7.9–8.5mb/d, because transportation fuels like gas and diesel will still be taken care of.

However cranking run cuts to a nuclear 10% scenario means they could survive without chasing a single market barrel even if seaborne flows dry up to 7.2mb/d—but they'd have to throw petrochemical feedstocks like naphtha and LPG under the bus just to keep gas and diesel flowing, a desperate move that runs on borrowed time and stalls out after a few months unless the whole economy is in a total tailspin.

To micromanage this whole run-rate circus, China's refining complex is pulling a highly responsive lever: the yield shift.

Beijing explicitly told state majors like Sinopec and PetroChina to ditch chemical feedstocks and prioritize flooding the market with gas and diesel, and these plants immediately saluted by shifting their product yields by several percentage points on a dime.

As a result, the real bloodbath isn't happening at the refining gate—it's completely decimating the downstream petrochemical chain. With Hormuz blocked, their seaborne naphtha inflows were already sliced in half, but a 5% run cut is about to bleed domestic naphtha and LPG supplies by tens of millions of tons a quarter, sending a compounding, fatal shock straight through the petchem feedstock backbone.

They are keeping wheels turning by guaranteeing gas and diesel, but the squeeze on industrial chemical feedstocks is completely running on borrowed time.

To paper over the massive raw material hole in the petchem chain, Beijing is shoving its massive 'Coal-to-Chemicals' complex into the spotlight, branding it as a strategic shield against volatile crude under the 15th Five-Year Plan.

Thanks to dirt-cheap, stable domestic coal, inland plants churning out olefins and methanol are running hot to boost volumes, but this quick fix hits a hard ceiling when it comes to replacing lost barrels at scale due to structural bottlenecks.

The core infrastructure is trapped deep in the northwestern sticks like Inner Mongolia, meaning slamming those products down to the massive manufacturing teeth on the southeastern coast comes with a punishing logistics and freight premium.

Most importantly, coal gasification routes physically cannot clone key aromatics or specialized LPG chemical chains—the feedstock deficit is mathematically locked in.

On top of that, the fact that Beijing is sitting on a massive 1.1-1.3 billion barrel pile without tapping it proves that institutional red tape is locking up the plumbing.

The 100 million barrels buried deep in dark underground rock caverns—completely invisible to satellites—are almost entirely SPR, requiring endless red tape like complex auctions and market disclosures, so Beijing is hoarding it as a nuclear option.

Even for the commercial barrels that are accessible, refiners are terrified to draw down because plotting out the repayment timeframe to replace that crude is a total mathematical nightmare in this chaotic macro environment.

Beijing is pulling off a highly calculated micromanagement script here: they are completely freezing out the inventory draw requests from state-owned heavyweights like Sinopec, who are nakedly exposed to global benchmarks and were the first to aggressively slash throughput.

Instead, they are using the Shandong teapots as a human shield—handing these independent refiners tax breaks and strict run-rate mandates because they have the flexibility to stomach toxic, illicit Iranian and Russian barrels to cushion the margin bleed.

Bottom line, this entire web of macro levers—starving imports, shifting yields, hunting for distressed barrels, and burning through coal-to-chem assets—will keep the lights on and protect the economic skeleton through the peak of summer, but only under that tight 5% run cut baseline that keeps seaborne arrivals pinned at roughly 8mb/d.

But with May and June seaborne prints already locked in at a subterranean 6.5mb/d, the expiration date on this makeshift band-aid play cannot stretch into autumn.

Short of letting their entire national refining infrastructure suffer a catastrophic meltdown, Beijing is running straight into a hard physical wall.

Before late summer wraps up, they will be forced to either open the strategic floodgates and dump their massive stockpiles or make a frantic U-turn right back into the international physical market, chasing heavy volumes aggressively at any price.

#oott #iran

English

Alex retweetledi

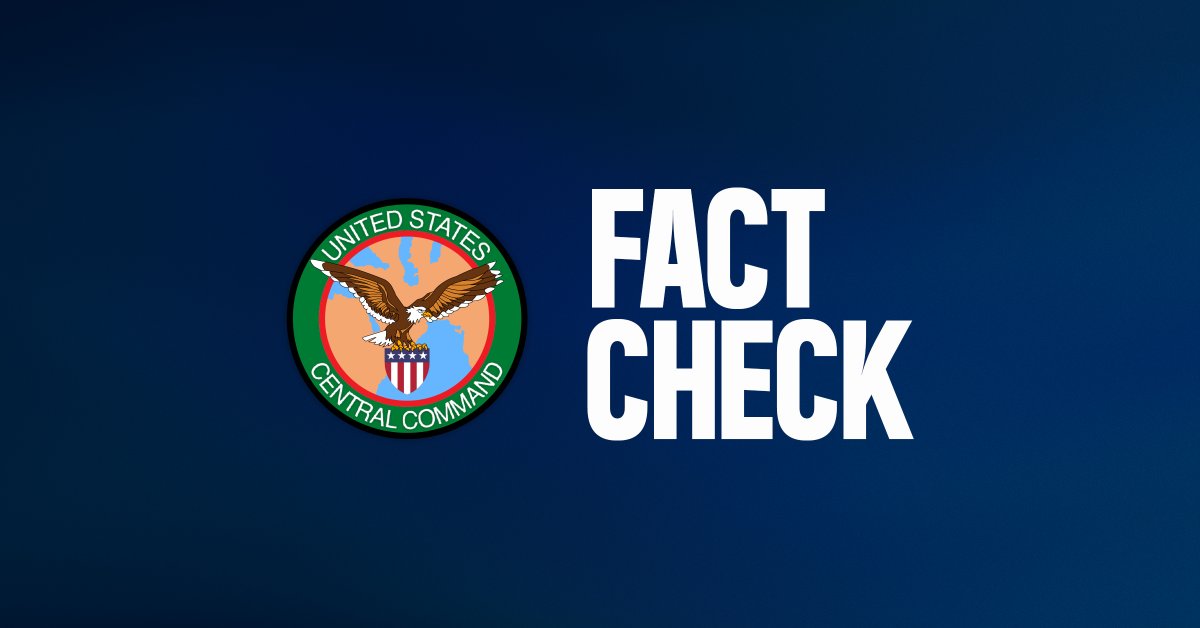

🚫CLAIM: Recent media reporting claims that the U.S. Navy has restarted escorting or assisting commercial vessels during transits through the Strait of Hormuz. FALSE.

✅TRUTH: Project Freedom has not resumed, and U.S. forces are not currently escorting commercial vessels through the Strait of Hormuz.

English