@BinanceTR Binance TR giriş yapılamıyor 2 haziran 2026 saat 00:30

Türkçe

That Valve Guy

1.4K posts

@AmCoin82832

Poor guy in the middle east who tries to learn tech stocks and hoping to get even knowledge with Korean/Japanese/Taiwanese and USA investors

Okay chat, it’s been awhile since the previous one. And a ton of names from $VPG to $ASPI cooked. So crowdsourcing a new list: What’s your highest conviction ticker that you think can 10x in a short timeframe, and why?

A lot of interest in CPO.

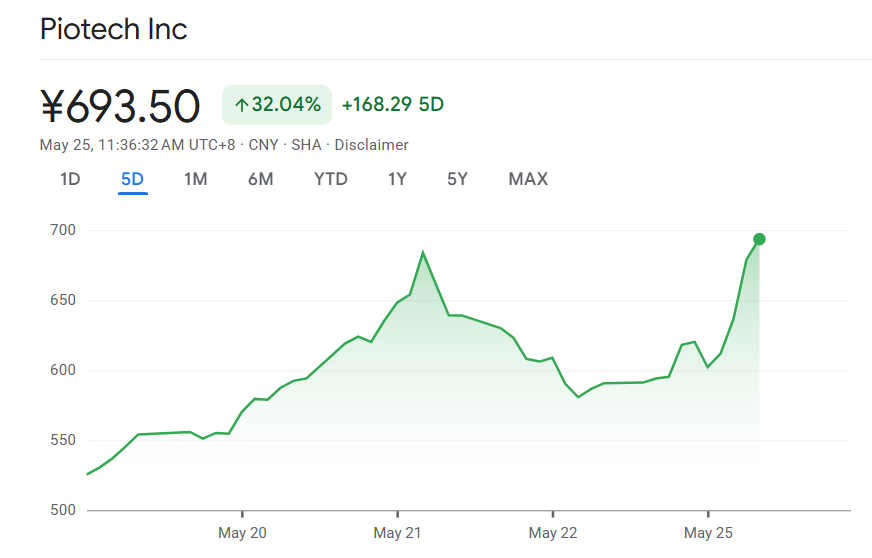

We are short $SIVE. A retail-driven pump built on speculative hyperscaler links, a fabricated bottleneck narrative, and a rumored volume ramp-up has driven a 1,800%+ rally in $SIVE.ST. Insiders sold ~29M shares into it. Here's what they're not telling you.👇 Full report: ningiresearch.com

We are short $SIVE. A retail-driven pump built on speculative hyperscaler links, a fabricated bottleneck narrative, and a rumored volume ramp-up has driven a 1,800%+ rally in $SIVE.ST. Insiders sold ~29M shares into it. Here's what they're not telling you.👇 Full report: ningiresearch.com

damn i took the screenshot too early lol

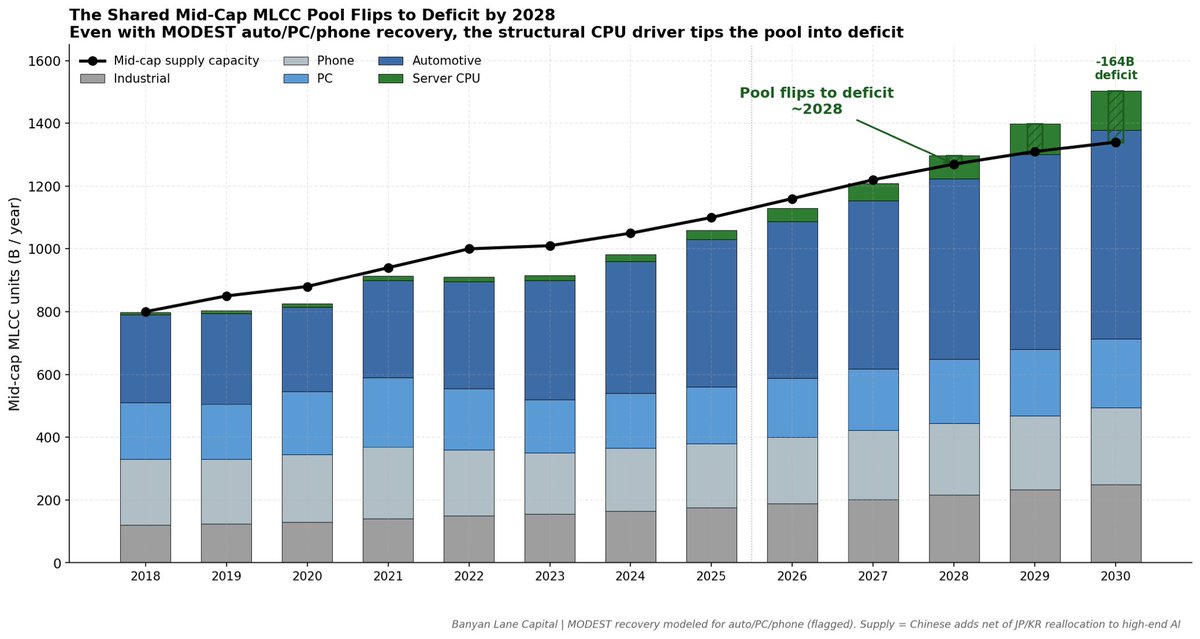

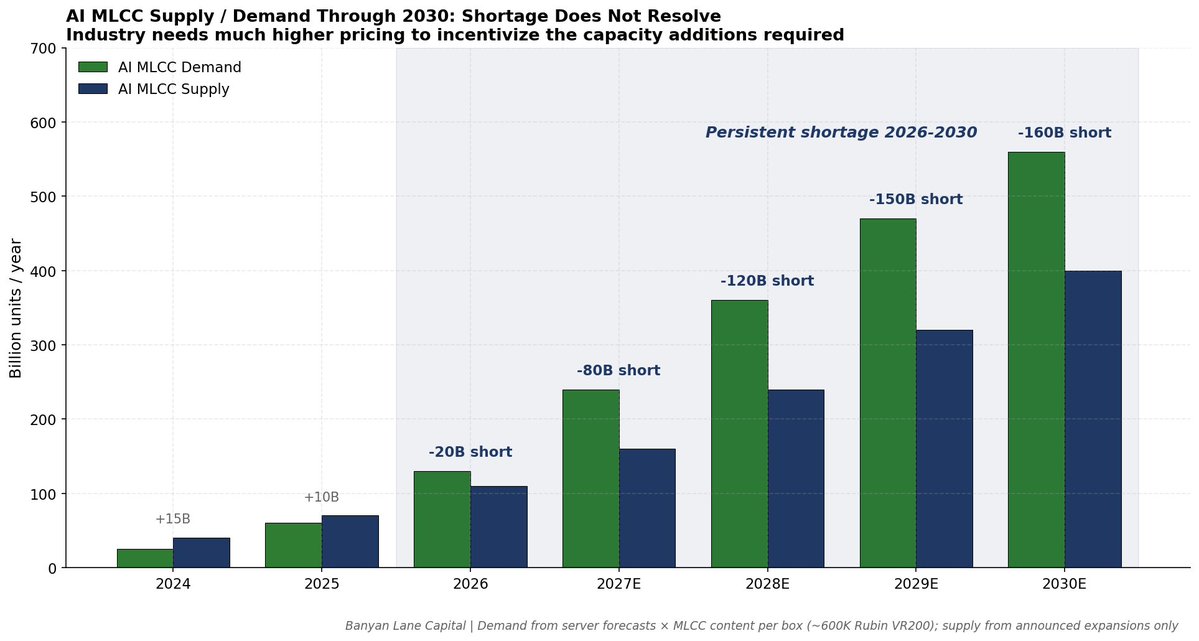

Please tell me if my $SIVE InP capacity modeling is incorrect. (Assuming WIN Semi's Maximum Expansion) Based on discussions with Taiwanese semiconductor industry experts, I still struggle to justify the assumption that $SIVE can become the next $LITE within the next few years. Since $SIVE outsources its InP manufacturing to WIN Semi, even under an extremely optimistic scenario assuming WIN Semi's maximum foundry expansion is converted to 6-inch InP capacity and largely allocated to $SIVE, my model still suggests that $SIVE's accessible InP capacity would only reach roughly 10% of $LITE's by 2028. So what am I missing here? Reference: x.com/Leoskie_L/stat…

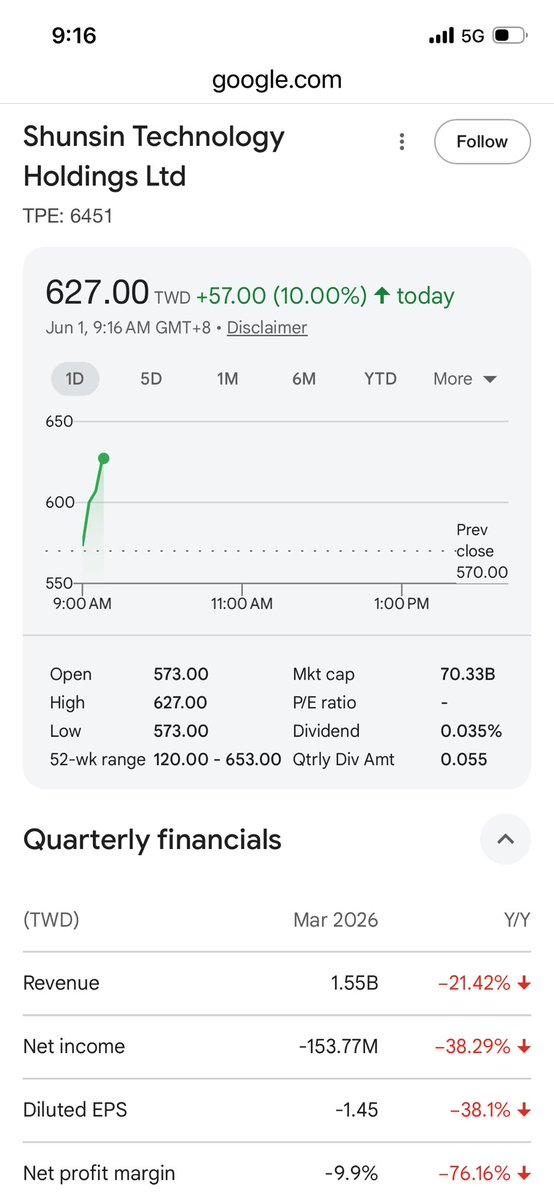

今年一萬台明年是五萬台CPO全光交換器,總共是差不多6B USD的CPO訂單給富士康,Shunsin富士康生態系獨家高階光學封裝佔全光CPO交換器總成本的10%,Foxconn->Shunsin大約是共600M USD的訂單,若給予10x P/S ratio,訊芯的MC只考慮這則新聞應該要來到6B也就是換算股價大約1500NTD左右的位置,若有接到博通的單則另外計算。

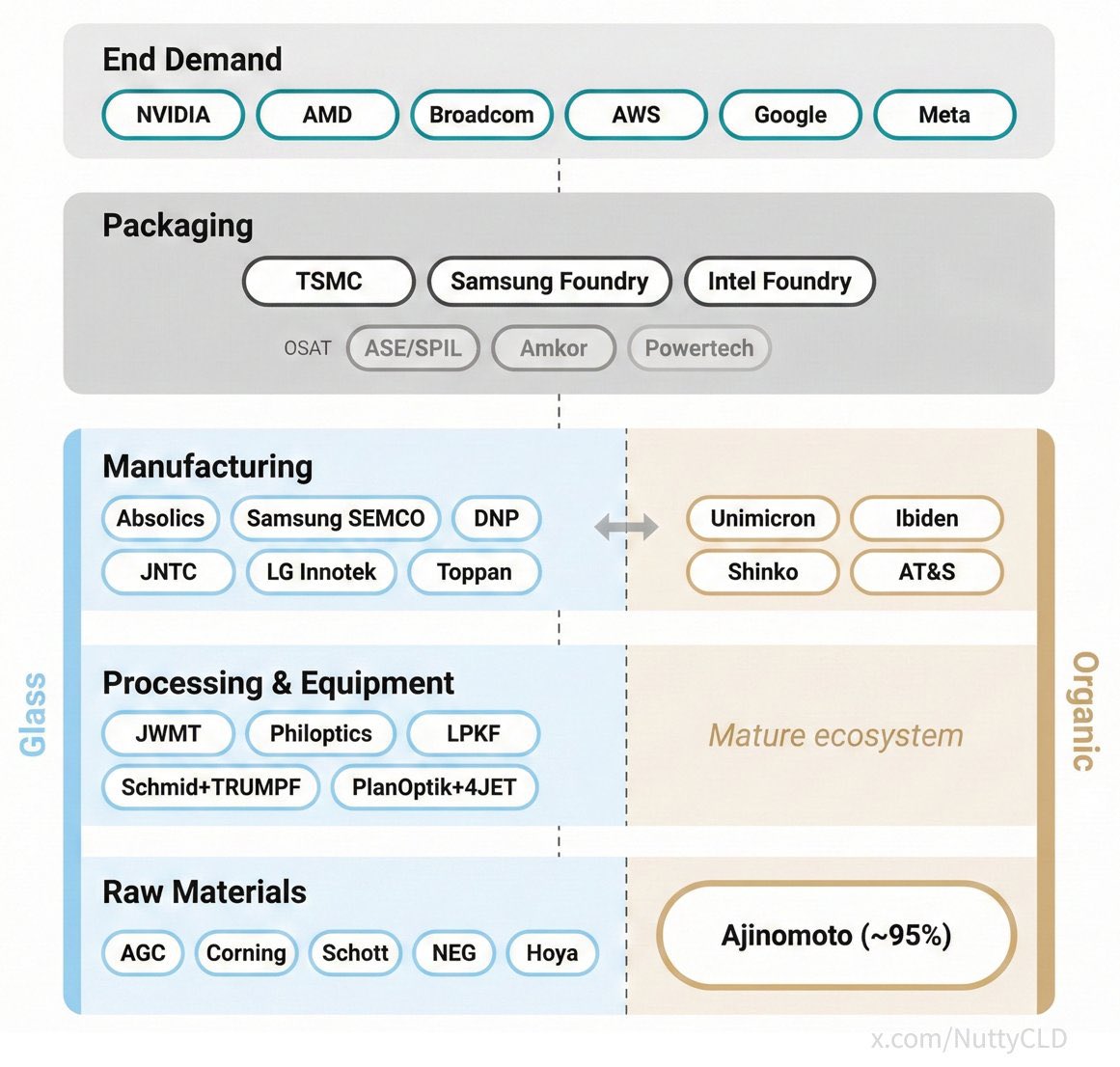

Taiwan $NVDA CPO supply chain ide #1: Shunsin (6451 TWSE) - Photonics Packaging at ~$1.4B MC. It's a subsidiary of Foxconn. And Foxconn is ODM for $NVDA. It's almost like Celestial got listed by $MRVL and got a free piggy back ride? Some personal est. 2027 fwd ~20 P/E, that compresses harder into 2028, 2029. Shunsin's optical division openly lists their markets as "CPO 51.2T/102.4T" and "Pluggable XCVR 800G/1.6T. Markets themselves as "Supported by Foxconn's vertically integrated supply chain for fast project ramp" If you look at $TSM COUPE for $NVDA, they don't assemble final fiber arrays/racks, Foxconn does. So $NVDA's CPO networking gear probably goes through Shunsin's alignment and bonding machines? And $GOOGL, $META optical switches probably end up thorough them too since they scaled Vietnam CPO facilities (speculative). Basically you get a free Foxconn piggy-back ride with this company at low forward multiples. Disclosures: I am personally long.

I think $SIVE should just become a full American company, and use NASDAQ listing as the first step. > US cap table / large ownership + US CHIPS act support already > larger valuation premiums + M&A opportunities. > local Swedish media blatant disinformation from underwater short sellers, isn’t helpful for AI photonics growth > lot of more funding opportunities + support from US institutions / funds / indexes By preserving EU efforts under a subsidiary and having a US parent company. This helps Sivers become a major US optical player, not just a Swedish semi trying to explain itself to local markets that doesn’t understand. I do think management sees a path forward for $SIVE to become the next dominant US photonics giant like $LITE.

Very impressive roadmap 2026 will be a big density jump for them and good enough for most advanced AI chips

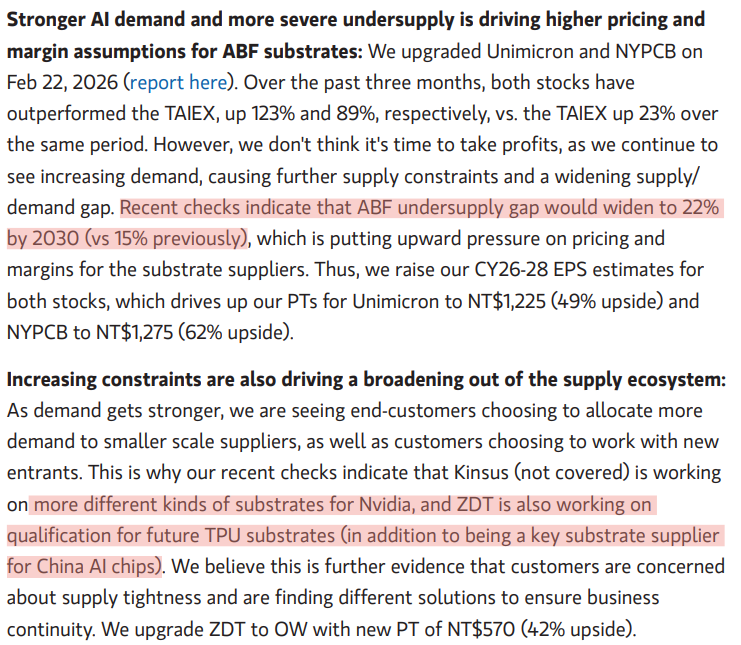

$ATS is up 200% in the last 6 months, but is still trading ~8.5x NTM EBITDA (they're just coming out a debt-funded expansion cycle). AT&S manufactures PCBs and the substrates that go between the chip and the PCB. As AI chips get more complex, you need more innovation in substrates. They're the main non-Asian player in this space, so seeing demand from AMD, Intel, and even defence firms. Operating leverage picking up too. Quite a few concerns, but mostly on competition (Unimicron) and the PCB segment (60% of revenue) being a drag. Great call by @illyquid and @Iqbal_yusuf1994 back in Nov.

BYTEDANCE IS DEVELOPING NEW AI INFERENCE CHIPS The Information reports ByteDance is working on a new AI chip with a structure similar to Groq’s language processing units. The chip is designed for inference, the workload behind running trained AI models and AI agents. ByteDance is also working with InnoStar Semiconductor to integrate Chinese memory technology into the design. The new chip may avoid HBM, the high-bandwidth memory used with many AI accelerators and heavily restricted by U.S. export controls. InnoStar specializes in RRAM, or resistive random-access memory, and ByteDance invested in the company in 2024. ByteDance is also developing a separate AI processor code-named Ada-S and another chip for video algorithms. Reuters separately reported ByteDance is developing custom CPUs for AI infrastructure as rising chip prices and supply shortages pressure its data-center buildout.