@pandaquantai Thanks for sharing but to fair why dont you Also add all those that are holding or buying of insititions . It anormal for some selling to happen . And insider sellin is very minor

English

Ana Paula Cintra

996 posts

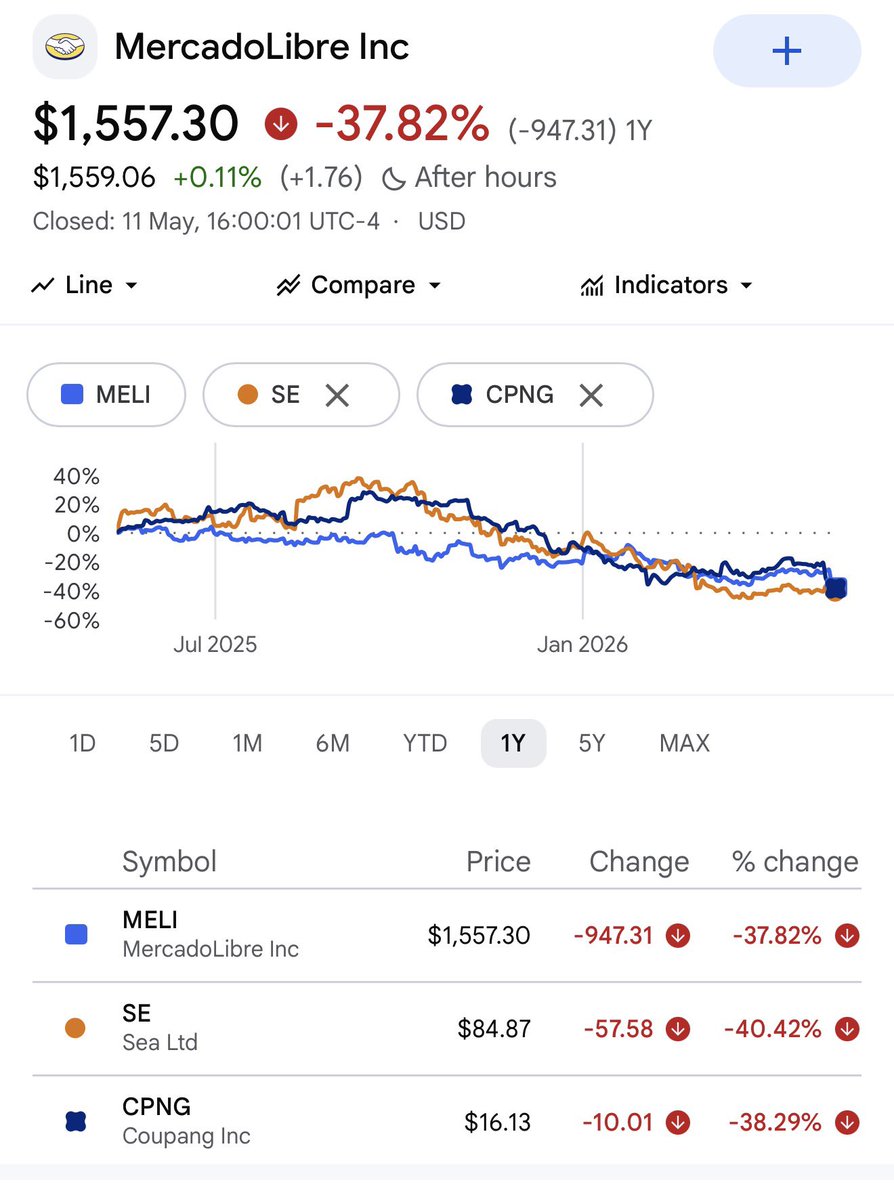

$MELI is not “the Amazon of Latin America.” It never was, and it never will be. Just repeating that label creates false expectations and lazy analysis. Mercado Libre has its own business model, its own market structure, its own risks, and its own limitations. It has nothing to do with Amazon beyond surface-level comparisons people use because it sounds catchy. This is exactly how investors get trapped in narratives. I warned about $MELI before, and it’s interesting to see how many hate messages and comments I received telling me how dumb I was when the stock was around $1,900. A lot of influencers on X even reposted my comments just to mock the idea. Now it’s funny to see how many of those same people quietly deleted their tweets. This is exactly why you should never become emotionally attached to narratives. Because valuation and price often have very little to do with each other in the short-to-medium term. Markets move on momentum, perception, positioning, and future expectations. 𝘼 𝙡𝙤𝙩 𝙤𝙛 𝙥𝙚𝙤𝙥𝙡𝙚 𝙬𝙝𝙤 𝙖𝙧𝙚 𝙨𝙢𝙖𝙧𝙩𝙚𝙧 𝙩𝙝𝙖𝙣 𝙮𝙤𝙪 𝙘𝙪𝙧𝙧𝙚𝙣𝙩𝙡𝙮 𝙗𝙚𝙡𝙞𝙚𝙫𝙚 𝙩𝙝𝙞𝙨 𝙞𝙨 𝙩𝙝𝙚 𝙘𝙤𝙧𝙧𝙚𝙘𝙩 𝙥𝙧𝙞𝙘𝙚. 𝙁𝙤𝙧 𝙩𝙝𝙚𝙢 𝙩𝙤 𝙗𝙚 𝙥𝙧𝙤𝙫𝙚𝙣 𝙬𝙧𝙤𝙣𝙜, 𝙩𝙝𝙚𝙧𝙚 𝙪𝙨𝙪𝙖𝙡𝙡𝙮 𝙝𝙖𝙨 𝙩𝙤 𝙗𝙚 𝙖 𝙘𝙖𝙩𝙖𝙡𝙮𝙨𝙩: 𝘼 𝙩𝙪𝙧𝙣𝙖𝙧𝙤𝙪𝙣𝙙. 𝘼 𝙘𝙝𝙖𝙣𝙜𝙚 𝙞𝙣 𝙚𝙭𝙥𝙚𝙘𝙩𝙖𝙩𝙞𝙤𝙣𝙨. 𝙎𝙤𝙢𝙚 𝙣𝙚𝙬 𝙞𝙣𝙛𝙤𝙧𝙢𝙖𝙩𝙞𝙤𝙣. 𝘼 𝙘𝙝𝙖𝙣𝙜𝙚 𝙞𝙣 𝙚𝙖𝙧𝙣𝙞𝙣𝙜𝙨. The fact that so many people on X still think $MELI is an obvious bargain while the stock keeps trading this poorly is, in my opinion, more of a warning sign than an encouraging sign. Because it suggests many holders still haven’t capitulated. They still believe. They still haven’t emotionally given up on the stock. Real bottoms usually come with exhaustion, apathy, forced selling, and disbelief - not confidence. You saw it before in $PYPL. You saw it before in $NOW. You see it now in $MELI. And many others. “Cheap” alone is rarely enough. Go through the history of most people currently calling $MELI a great opportunity, and you’ll notice that most of them were saying the exact same thing when it was trading at $1,900 too. Without a catalyst, without strong price action, and without a real change in trend, it’s difficult for a broken stock to suddenly recover just because people think the valuation looks attractive. Bad charts can always get worse.

🚨 Compute is the bottleneck $AMZN AWS Growth 28% $MSFT Azure Growth 40% $GOOGL Cloud Growth 63% $GOOGL CEO Sundar Pichai: Our cloud revenue would have been higher if we had more compute.