Sabitlenmiş Tweet

Very happy to join Princeton's @PUPolitics @BobstCenter as a Visiting Research Scholar, for a year. Excited to meet people and explore new ideas – let me know if you are around!

English

Andreu Arenas

1.2K posts

@AndreuArenas

Economist | PhD @EUI_EU | Editor @nadaesgratis | Trying to answer interesting questions using data.

This from @alexolegimas and @soumitrashukla9 is by far the best thing I’ve read on how to think about how AI may affect the labor market. Absolutely required reading. aleximas.substack.com/p/how-will-ai-…

IA y productividad: promesas y obstáculos nadaesgratis.es/andreu-arenas/… Vía @nadaesgratis #Economía

One of the clearest examples of public ignorance and irrationality having bad political effects.

Again I ask: Is the “Wall Street wants to turn single family homes into an asset class” stuff an exaggerated myth, or is it an essential plank of the abundos’ housing agenda?

Cese de actividad del blog NeG nadaesgratis.es/editores/cese-… Vía @nadaesgratis #Economía

This is the kind of statement I worry about. Basically, the Pentagon apparently agrees and is doing this. But I can’t imagine this is what @DAcemogluMIT , @davidautor and Johnson mean. So what is the nuanced application of power?

Aquest dimecres, Gerard Maideu (European University Institute) explica que el creixement econòmic pot reflectir-se tant en salaris com en feines més segures i de més qualitat. Ignorar aquestes millores pot conduir a una subestimació del creixement. 5centims.cat/creixem-mes-de…

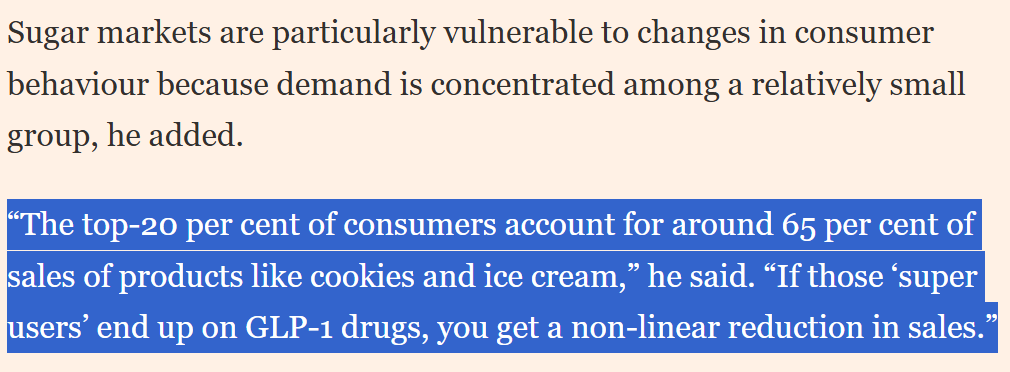

Sugar prices have tumbled to their lowest level in more than five years as weight-loss drugs accelerate a drop in demand by pushing consumers to ditch sweet treats in favour of protein. ft.trib.al/KSGrkUo

Economics is mostly a bullshit field of study. It is specifically for people who can do a little bit of stats and calc and want to feel smart but too dumb to study physics or math. Most economic theories are built like this: they start with an assumption about human behavior. Then without checking if the assumption is true, they will pile on layers of sloppy math on it and come to all sorts of conclusions that obviously don’t hold up in the real world. Recently a couple of economists won the Nobel Prize for being the first to realize that assumptions about human behavior must be tested and they went out and did some field work, and proved that a lot of assumptions in economic theories about how humans behave with money are well just not true. I was working at a bank for 2 years and saw firsthand that economics PhDs tend to be the dumbest. These people are completely alien to the idea of first principles thinking and treat axioms as if they were written in the Bible. Also they don’t really understand what an axiom is. Economics only exists because your average normie is easily impressed buy math and midwits in power are not scientific enough to realize that it is all voodoo and keep taking economists seriously. I don’t blame them though, at some point they hit an intelligence wall and the average economist brain is simply not equipped to have meta level thoughts about their own field of study. I guess this is one of those bullshit jobs like HR, therapy, astrology, project management that will just stay around for a while cause most humans are either mid or retarded.