Sabitlenmiş Tweet

Après Capital

5.3K posts

@ApresCapital

/ Markets, Macro, Magniloquent /

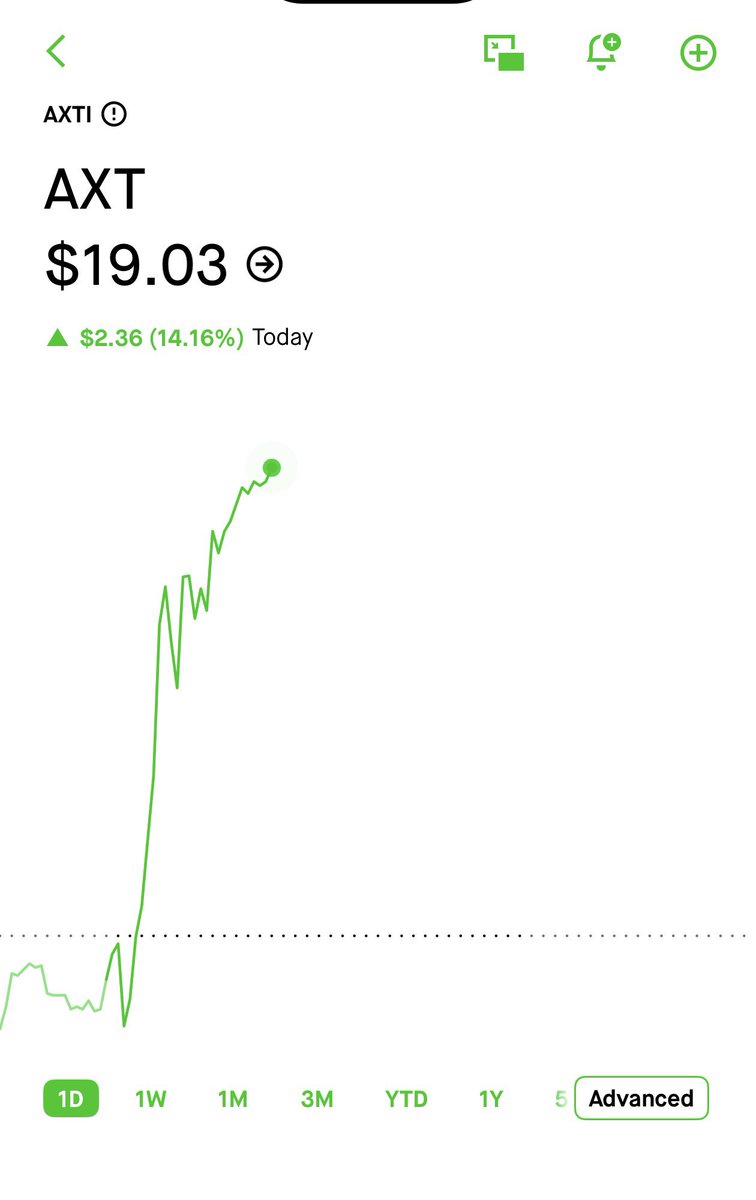

Warning: The entire AI industry will likely be bottlenecked by two companies: 1. $AXTI ($700M) 2. $SMTOY ($31.7B) Which both control 60–70%+ of the world's InP substrates. Future $NVDA, $GOOGL TPU v7 pods, $META, $MSFT, $AMZN hyperscaler clusters require InP-based lasers and receivers. $AVGO, $LITE, $COHR use for EMLs for 800G/1.6T transceivers, DFB lasers, and other optical infra. Without InP substrates, the supply chain falters. After looking at TPU BOM to Maia BOM, it looks like future ASICs + GPUs + hyperscaler deployments are heavily reliant on photonics. And two vendors could freeze the global InP substrate market covering nearly all of: - Hyperscaler optics (TPU pods, etc) - Optical transceivers (5g, data) - LiDAR (robotaxis, drones, military) -Optical Modules (interconnect clusters) - Silicon photonics laser dies (Nvidia’s future co-packaged optics and Intel/Broadcom SiPh engines use InP CW laser arrays.) Since these companies make up majority of the market supply: -AXTI (est. ~30–35%) -Sumitomo (est.~30%) - JX Nippon (est. 10-15%) That’s it. (eg. 2021 industry note from Yole states that "Sumitomo Electric + AXT together had “more than 75%” of the InP substrate market") Hyperscalers/AI are moving toward photonics but the entire AI industry is fragile. If either $AXTI or $SMTOY stop supplying materials, the entire future AI buidlout gets crippled. It's even crazier that a $700m company could become the the center of it all. InP substrate will likely one of the biggest bottlenecks alongside HMB as the AI industry shifts to photonics.

@TheValueist Good explanation and thesis. But remember Sumitomo Electric is Japanese, China exports 70% of raw Indium supply and has just banned all exports to Japan. Sumitomo Electric inventory levels will not be high given the permitting situation. It’s ATX or bust for most clients..

My guest today is Paul Tudor Jones (@ptj_official), one of the greatest macro traders of all time. He correctly predicted the 1987 stock market crash and shorted the Japanese bubble in 1990. For over 40 years, his flagship fund has had a negative correlation to the S&P 500. 100% of his returns are alpha. He says today's market has so many similarities to 2000, "the easiest bear market I've ever seen in my whole life." He makes the case for going long dollar-yen, why Bitcoin beats gold as an inflation hedge, and why he was wrong about Warren Buffett. But what I'll remember most from this conversation is Paul's zest for life. He's 71 and still wakes at 2:30 every morning to trade the London open. He works out for two hours a day. He walks with his wife every evening. He travels the country chasing peak spring and peak fall. He's so excited about the songs picked for his funeral that he wishes he could be there to hear them. Paul has lived five lifetimes in one. He's one of the most entertaining and interesting people I've met, and the conversation will leave you searching to be as passionate about what you do as he is about what he does. Enjoy! Timestamps: 0:00 Intro 1:00 The Kindest Thing 13:19 Trading vs. Investing 17:33 Lessons from Warren Buffet 22:24 The Existential Risks of AI 29:54 The Nature of Trading 31:46 Bitcoin 35:55 Bubbles 42:08 A Day in the Life of PTJ 46:00 Information Overload 47:07 Passion for Markets 50:49 The Robin Hood Foundation 54:18 The Workless World 56:03 Journalism 1:00:00 Principal Components of a Great Life 1:05:06 Kill Them With Kindness

DeMARK is now available on @TradingView and we're giving away 4 free annual Superchart plans 🏆 Prizes: 🔸Essential 🔸Plus 🔸Premium 🔸Ultimate To enter: 1⃣ Follow @DeMarkAnalytics 2⃣ Like this post 3⃣ Repost Winners will be announced on April 27.

Was at the WH Correspondents dinner last night, a rare DC trip for me without a subpoena. On the positive side—was exciting, no one was killed, and ended early. I noted a new litmus for status among the gov’t elite—whether you were whisked away by secret service, or left to fend.

Good Morning ! A bad night and an unforgettable image …

My bias: The deal was agreed already pre and details ironed out in the first round of talks when 100s of American delegation + 80 Iranian delegation attended. The phase we in since has been the agreed theatrics episode to get it sold back home.

🚨🚨BREAKING Massive blaze at one of India’s biggest petrochemical refineries (HPCL Rajasthan, Pachpadra) 4th major oil/gas incident in 5 days 🔥 - 15 Apr: Viva Energy Geelong Refinery fire (Australia) - 16 Apr: Deadly gas pipeline explosion in Haripur, Pakistan (8 killed) - 18 Apr: Fires at Russian oil refineries (Novokuybyshevsk & Syzran hit by drone strikes) .. and now this! What’s happening?! 😱