Gil Arbell

93 posts

@RozOded @dvdrnsl204 לדעתי תוצאות ההצבעה היו מראות שאותם 3 דירקטורים שהציעו המוסדיים היו מקבלים הרבה יותר מ8% מהקולות.

אולי הדירקטוריון (עדיין) לא נמצא כאשם בבית משפט, אבל איך אומרים

“if it looks like a duck, walks like a duck, and quacks like a duck, it’s probably a duck”

עברית

@dvdrnsl204 3 מ8 זה יותר מידי ל8% אחזקה, רוצים לקנות שליטה שיתנו הצעת רכישה בעצמם.

תסביר למה הדריקטוריון הנוכחי פושע? הם לא הסכימו להצעת הרכישה הנמוכה, וכבר הוציאו הודעה שלקחו יעוץ לגבי רכישה עתידית. וכבר יש מספיק עיניים על האירוע

עברית

@Chuckyb22074706 @InvestyMan Any thief that was caught in the act will say they “would have handled things differently”.

Insanity is doing the same thing over and over and expecting a different result. Voting for the current board is exactly that.

English

@InvestyMan Meaning they came across as sincere; that if given the opp to do over would've handled the Ofer/BOD thing differently. I mentioned Maersk's approach to buybacks etc but not going to try and armchair manage. If I don't like what I see I'll sell my $ZIM. I still like what I see.

English

FYI, just had 30 minute conv w/2 of $ZIM BODs incl ChairYairS. Changed my vote for them. I gave them the riot act about Ofer and his two guys on the board during mbo process=BAD af. Their response satisfied me that they were 1) above board and 2)totally against $20/share.

English

Gil Arbell retweetledi

$ZIM Severe Capital Allocation Failure

We have witnessed criminally poor capital allocation a total failure that reached its peak in 2024 and 2025.

The Board of Directors and Management have not acted in the shareholders' best interests.

Take, for example, the case for a

Buyback Program:

# The stock had huge daily volume.

# It traded deeply below its cash position.

# It traded deeply below book equity (let alone economic equity).

# The company’s revenue recognition model provided P&L visibility two months in advance.

The share price could have reached levels that are hard to imagine. The potential value for investors was theoretical yet immense.

Our focus is on Cash per Share and Economic Equity per Share, rather than a megalomaniacal focus on the company's aggregate size.

A Theoretical Illustration:

Equity: 300

Cash: 100

Market Cap: 50

Trading at 0.166x Equity

Trading at 0.5x Cash

Scenario: A Buyback of 20 (Theoretical adjustment):

New Equity: 280

New Cash: 80

New Market Cap: 30

Trading at 0.107x Equity (Down from 0.166)

Trading at 0.375x Cash (Down from 0.5)

It is difficult to visualize this when the market refuses to assign fair value. However, a pro-shareholder Board could have driven the share price to over $100.

Effective capital allocation during a period where the market does not close the valuation gap (between market cap, cash, and economic equity) is critical.

Ultimately, one of two scenarios would have materialized:

1. The gap between Net Cash/Economic Equity and the share price would have closed, reflecting proper valuation.

2. The company could have utilized the arbitrage opportunity to continue the buyback until the stock reached $100 or higher

English

@ZeeContrarian1 The value is there, the question is how will it get to the share holders?

English

$ZIM Buyout Math

(I have never seen something like this)

•Shares outstanding: 120M

•Current share price: $13.6

•Buyout offer: $22/share

•Total cost of buyout:

22 × 120M = $2.6B

Cash & Assets

•Cash per share: $24

•Total cash: 24 × 120M = $2.88B

•Additional assets: –$5B (net), with ~$1B liquidatable without materially harming operations.

Structure (PE-Style Arbitrage Play)

1.Loan: Ask a bank / PE lender for $2.64B bridge financing (1 month maturity).

2.Buyout: Acquire all shares at $22/share = $2.64B.

3.Post-close balance sheet:

•Cash on hand = $2.88B.

•Debt from buyout = $2.64B.

•Immediate net cash = $240M surplus + control of $ZIM ’s operations and liquidatable $1B in assets.

4.Repayment: Use ZIM’s cash ($2.64B) to immediately repay the loan.

5.Leftover: ~$240M free cash remains in the newco, plus $1B in liquid assets and the full operating business.

A buyout or management-led partial buyout appears imminent. Unfortunately, all funds I spoke with don’t have visibility on the exact timeline. Management probably wants to make shareholders puke their stock before they come in with the buyout offer.

And this valuation is so obvious you don’t even need an Asian quant on your team to do the math.

English

לגאסי מופיעה במדגם כלכליסט הבוקר כאחת מקרנות הגידור שניצחו את הבנצ׳מרק שלהן במהלך המחצית הראשונה של 2025.

תשואת ה - S&P 500 מוצגת בכלכליסט במונחי $ ארה"ב יש לציין.

נכון למחצית, זו השנה השלישית ברציפות שלנו כקרן גידור מוטת חו"ל הטובה בישראל

calcalist.co.il/market/article…

עברית

#BREAKING ☢️🇺🇸⚡🇮🇷 Director of National Intelligence Tulsi Gabbard issues a strange and shocking nuclear warning, warning an incoming nuclear Holocaust and call others to ‘Reject this path’.

Is she signaling something from inside US government to outside that we don't know?

English

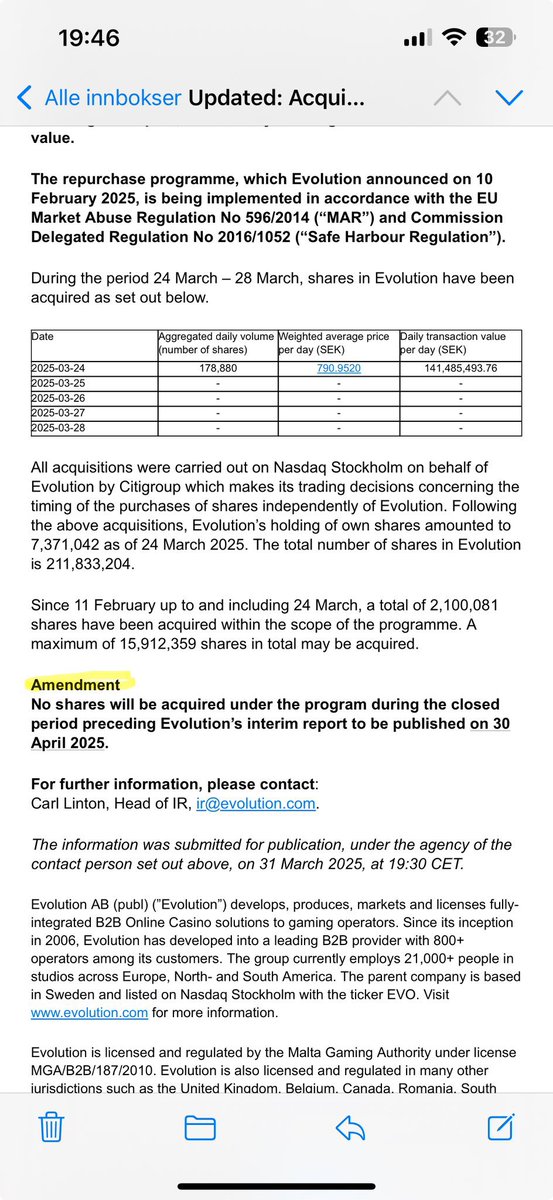

@KvammeSteffen As far as I know It’s a requirement by EU regulation that they not buy back shares in the 30 days prior to an earnings release.

English

Any $EVO-analysts out there who plans on asking questions tomorrow during the conference call? If so, could you add this:

-“Any particular reason you stopped the buybacks a month before the report?”

English

@BrownMarubozu @MananaInvesting @Kevin_AGraham @VikingVan100 At what point does size start to be a limiting factor for them? 47 billion CAD$ market cap ain’t that small.

English

@MananaInvesting @Kevin_AGraham @VikingVan100 P/B has to be used in conjunction with ROE. If the assets are worth more than book then ROE will be higher for the whole company as they produce more income. $FFH.TO has an operating ROE of ~15%. I think $BRK is closer to ~8%. BRK has a lot of Social Value. At FFH, SV is -ve.

English

Has Fairfax become the perfect safe-haven trade? Yes, that sounds bizarre. But if it looks like a duck, swims like a duck, and quacks like a duck, then it probably is a duck... $FFH.TO

English

@bramschiphouwe1 @TacticzH From my understanding it is a requirement of EY market abuse regulations, ie they are halting buybacks to comply with the law and not because of any specific information due to be public or need of capital for other activities.

English

$EVO $EVVTY

No shares will be acquired under the program during the closed period preceding Evolution’s interim report to be published on 30 April 2025.

Guess we do not have to worry about that anymore. 😀

English

@Nukular11 From a logical perspective that’s totally right. But seeing red in your portfolio is never fun.

English

בים של אדום אני רואה נקודה ירוקה אחת היום וזו צים.

שילוב של דוחות מעולים, מכפיל זול, סטאפ טכני סופר שורי בגלי אליוט, ודיבידנד מאוד נדיב של 3.17$ למניה שישולם ב 3/4/25.

$ZIM

Avery@ATMSnipes

$ZIM back at it again with a weekly $ZIM post because this stock looks special and I've been ringing the bell on it for months now. Textbook impulse. Weekly Cup. Weekly Handle. IH&S in the Handle. 200D EMA supportive?✅ rebid the 50D EMA & its game on again Only downside I see here.. Freight is cyclical and they have moderate expectations for 2025. Revenue: ZIM reported Q4 2024 revenue of $2.17 billion, an 80% increase year-over-year from $1.21 billion in Q4 2023, surpassing analyst expectations of $1.91 billion to $2.02 billion. Full-year revenue reached $8.43 billion, up from $5.16 billion in 2023, driven by higher freight rates and record volume growth. Net Income: Net income for Q4 was $563 million, a stark turnaround from a $147 million loss in Q4 2023, yielding an EPS of $4.66 (diluted), beating forecasts of $2.83 to $3.49. Full-year net income was $2.15 billion, reversing a $2.7 billion loss in 2023. Current Dividend: ZIM declared a Q4 dividend of $382 million, or $3.17 per share, payable April 3, 2025. Full-year dividends totaled $7.98 per share ($961 million), representing 45% of 2024 net income, up from a $0.23 per share policy in prior quarters.

עברית

This might be the smallest, most illiquid, and mispriced stock I’ve ever stumbled across. Bodyflight Sweden AB is a nano-cap with a market cap of just 8 million SEK—about $750,000 USD. What makes it fascinating? It has generated an average of 5 million SEK in free cash flow past years and holds 88 million SEK worth of property, plant, and equipment on its balance sheet. That’s a stock trading at a 0.1x price-to-book ratio and less than 2x its free cash flow.

So why is it so cheap? There are real risks: razor-thin liquidity, a rough 2024 ahead, and some debt that needs careful handling. It’s priced like a company already on its knees, teetering toward bankruptcy. But here’s the kicker— even if it fails, the liquidation value of its assets could exceed today’s market price. And if management can steer through the challenges this could turn into a multi-bagger opportunity for those willing to stomach the volatility.

It’s a simple, overlooked story that’s too mispriced to ignore. Want the full breakdown? Link to my deep dive is in my bio!

English

@Omri_Legacy "The marginal prices are set by the dumbest insurer in the business"

English

במהלך השנתיים-שלוש האחרונות יצא לי לדבר הרבה על איך כדאי להסתכל על חברות ביטוח בגלל עניין, וגם חשש, של משקיעים שבחנו כניסה ללגאסי בהחזקה המאסיבית של הקרן בפיירפקס.

הדבר הראשון שאני מבהיר הוא שחברת ביטוח, ובכלל כל חברה שעושה חיתום למחייתה (אשראי חוץ בנקאי, בנקים) - ***לא יכולה לדבר במונחי יעדי צמיחת מכירות***

🚩🚩🚩

הכלל הזה חסך לי המון כסף

אופטיקאי מדופלם@meduplam

לפני כחודשיים, למונייד קיימה יום משקיעים, שבמרכזו עמדה תחזית לצמיחה בקצב 30% CAGR במשך עשור. כן מה ששמעתם. הגדיל לעשות סמנכ״ל הכספים, שעל סמך התחזית הזו טען שבכל תסריט אפשרי שהוא ניתח, המניה של למונייד צריכה להיות שווה $90. לנקוב במחיר יעד למניה של עצמה, זה כבר משהו שמעולם לא ראיתי הנהלה עושה ביום משקיעים. ובכן, חודשיים לתוך העשור הזה - למונייד לא צמחה ב-30% ברבעון האחרון. ואפילו לא מציגה תחזית לצמיחה של 30% ב-2025. מה שכנראה אומר שה CAGR של 9 השנים הבאות יהיה אפילו יותר גבוה מ-30%! או שזה אומר שהתחזית מיום המשקיעים הייתה מופרזת. אחת מהאופציות. לפחות אינסיידרים הצליחו לנצל את חלון הזמן שבו המניה זינקה אחרי יום המשקיעים כדי למכור (בהרבה פחות מה-90 שההנהלה טענה שהמניה שווה). כתבתי עוד על יום המשקיעים ההוא במהדורה 100 של הרהורי יום שישי.

עברית

$EVO CEO Martin Carlesund at the next earnings call 😅😅 (sorry) :

youtube.com/shorts/L4QA4q3…

YouTube

English