Asymmetry

1.1K posts

Asymmetry

@Asymmetry_X

Long term investor seeking out asymmetric opportunities. NFA.

United States Katılım Şubat 2024

505 Takip Edilen899 Takipçiler

NAKA is now at $0.15 per share.

The market is paying roughly 48 cents for $1 of senior claims-adjusted Bitcoin exposure.

That means either:

The balance sheet deserves a massive trust discount

The market has not figured out the CEBE math yet

The stock is obscenely mispriced

Maybe some combination of all three.

What do you think? 🤔

English

@amitisinvesting You hit the nail on the head with your last sentence. Many so called investors are not. They are gamblers.

English

is everyone okay with realizing that you don’t have to be in every single stock that goes up and you definitely don’t need to sell your losers and chase a winner every other day?

like if you are in a name that had a great 2025 and is having a bad 2026…you realize you don’t have to dump it and buy the name that went up 40x in a year right?

are we all also okay with realizing that complaining about your name being stuck and some other name going up means you are a just someone who has no conviction because you 1) cant cut the loser 2) don’t have the balls to buy the name that is moving which means all you are basically doing is yelling at a brick wall?

like if you didn’t want to buy any names that dipped last few days…why are you complaining about them being up today?

if you can’t handle your 10x from 2024 beginning to consolidate in 2026 (which is maybe healthy) without thinking it’s an opportunity cost then why are you upset if the name you chased is going down 10% in a day? didn’t you want volatility?

it’s almost like everyone decided they can become a hedgefund manager and make a change to their portfolio every single day and not actually have a thesis to a company and let it play out (through the good and bad) and as a result have decided to complain about every single market move

it’s just not healthy, either DCA into the names you believe in or sell them and go chase the winners but the complaining daily is becoming laughable when investing is, and has always been, a long term game

English

I respect the reply. Disagree fundamentally on the BTC vs ETH debate, but respect the detailed reply. I addressed only the inflation rate as that was the basis of the initial post, but my qualms with ETH go beyond the fluctuating supply (centralization, premining, existing precedence for protocol change, PoS, Vitalik specific concerns). I also don’t agree that the Bitcoin network with settlements on top of it like Lightning can’t also achieve similar purposes to ETH’s purported purposes. We’ll probably just agree to disagree

English

See but there’s an implicit assumption there that the usage of ETH itself will remain approximately the same in two years… considering Larry Fink’s push for tokenization, the various ETFs/DATs, and the CLARITY Act about to pass (paving the way for widespread use of stablecoins and their programmatic usage) - I seriously doubt that assumption to hold.

If true, that means the network will likely have enough activity for the inflation rate to go formally negative due to fee burning. Not inflating at a decreasing rate like Bitcoin, but inflation formally below zero.

This is speculative at the moment, yes. I’ll concede that point. But it’s not hard to see this materializing against the current landscape of how development and adoption by commercial industry is happening (albeit largely out of the mainstream headlines). Like it or not, the things Ethereum enables cannot be achieved on the Bitcoin network.

English

Annual inflation rate (or any other metric you want to discuss) only matters if you have an annual time frame. Presumably when discussing the merits of a new technology in solving the issue of a broken money system that references the many thousand year history of various faulty currencies, one is looking beyond a year time frame instead of cherry picking a single point in time. But if the annual rate does matter a lot to you, would you then agree to switch away from being an ETH maxi to a BTC maxi in April 2028 after the next BTC halving when the annual inflation rate of BTC < ETH?

English

@Asymmetry_X @FunOfInvesting Serious question: what’s the current annual inflation rate of Bitcoin? (as a percentage)

And what’s the same for Eth?

I’ll save you some time

Bitcoin: 0.83%

Ether: 0.79%

Even when ETH is supposedly running hot, it still has lower inflation than bitcoin.

English

Let's talk about $IREN and why I think a Sweetwater deal is imminent.

The capital Dan has raised in the last 8 months:

→ $5.8B Dell GPU purchase agreement (Nvidia GB300s)

→ $1B convertible notes (Oct 2025)

→ $2.6B convertible notes (closed last night, upsized from $2B, converts at $73.07)

→ $2.1B NVIDIA equity investment right (30M shares at $70)

→ $400M GPU financing

→ $625M Mirantis acquisition (software + orchestration + 1,500 enterprise customers)

→ Nostrum acquisition (490MW in Spain + GW pipeline)

→ $9.3B in total funding secured

All of this in 8 months. You don't raise that kind of money without knowing exactly where it's going.

Sweetwater 1 is energized. 1.4GW connected to the ERCOT grid. The power is on. The software layer is acquired. The GPU supply is secured. The capital is raised. The only thing missing is the tenant.

Both the Microsoft and NVIDIA deals are bare metal — IREN owns the GPUs and provides the compute. A Sweetwater deal will be the same model. And with demand for AI compute at all-time highs, pricing per MW is only going up.

So what could a Sweetwater deal look like at $11-12M per MW?

200MW (first phase):

→ 200MW × $11-12M = $2.2-2.4B annual revenue

→ 5-year contract: $11-12B

500MW:

→ 500MW × $11-12M = $5.5-6.0B annual revenue

→ 5-year contract: $27.5-30B

1,000MW:

→ 1,000MW × $11-12M = $11-12B annual revenue

→ 5-year contract: $55-60B

For context the Microsoft deal was $9.7B. A Sweetwater first phase alone could exceed that. Anything beyond 500MW would be the biggest single compute deal in the industry.

NVIDIA locked in the right to buy shares at $70. The convertible converts at $73.07. Two separate groups of institutional money are telling you $70-73 is a fair entry.

The stock is trading below both.

nfa, long $IREN ⚡

English

I’m of the opinion that these companies are about to enter the S growth phase and need up front capital to fund the build outs which will bring exponential returns. So I’m ok with “dilution” realizing most of this is not up front and will occur in 5 years time by expiry. But the NBIS vs IREN debate takes are very low IQ.

English

Remember last week how I said I won’t touch $IREN because they have the weakest numbers and the highest dilution risk and I got hate in the live chat for it?

Well… this is exactly what I meant. As more time passes $NBIS will continue to decouple from the pack. Quality shows.

Parkash Heerani@HeeraniPK

$IREN 7% down after announcing $2B of convertible senior notes due 2033 with an option for another $300M This is in addition to $6b ATM announced before and 30m shares of calls 5 years out at $70/share to $NVDA

English

@EricTNFL @FunOfInvesting Sure, don’t deny that and I’m not an NBIS bear, I’m actually a shareholder. I just find this post comically short sighted. “Highest dilution risk” but forgets about 3 dilution deals in 9 months including just over a month ago.

English

Everyone is wondering what the next $SNDK is going to be.

My answer is $ASST.

Market cap of $1.1 billion. One of the fastest growing public Bitcoin holders in the world, currently ranked 9th with 15,000 Bitcoin on the balance sheet.

Their ambition is to become the second largest issuer of Bitcoin credit in America.

That is a trillion dollar opportunity at a billion dollar valuation.

English

Asymmetry retweetledi

@amitisinvesting I don’t want my future grandchildren asking me, “Why didn’t Papa Jawwwn buy SpaceX at IPO?”

English

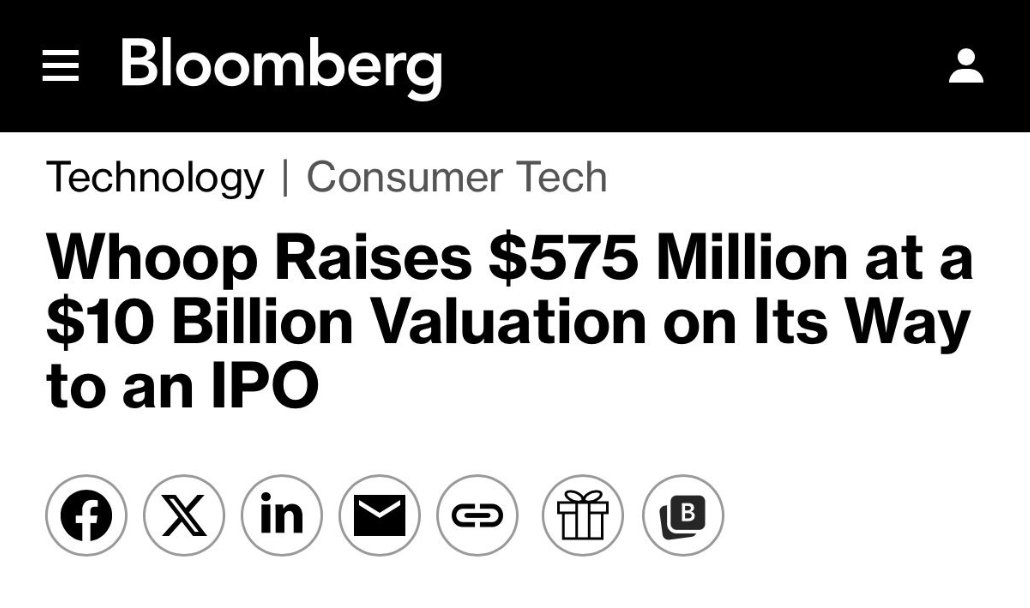

🚨 BREAKING: WHOOP RAISES $575 MILLION, VALUED AT $10 BILLION

- Now has 2.5M subscribers, was cash flow positive in 2025, grew subscriptions +103%

- Wants to IPO in next 1-2 yrs

- Oura valued at $11B as of Oct 2025

- $HIMS market cap currently $4.5B 😳

English

Loved the vid! Would be neat to see poker creeping into the vids somehow. Maybe betting against an opponent but something more creative than “$5000 if I break 80” or “closest to pin.” Maybe both players start with same chip stack and you make bets on hole winner each stroke (like streets) prior to green.

English

I’m making my YouTube golf debut today…and naturally there’s action:

$5,000 says I break 80 from the red tees at SouthShore Country Club ⛳️

I’m an 11 handicap…

Confidence or delusion? 😂

What should I film next?

English

Asymmetry retweetledi

“11% is a big number.”

“Am I offending you if I call it a money market fund?” - @SullyCNBC

Digital Credit is redefining yield.

Today we discussed Stretch $STRC on @PowerLunch.

English

$NBIS signs massive $27B deal with $META a week ago

Today $CIFR signs 15 year deal with a hyperscaler

Will $IREN sign a major deal soon?

English

Agree with TTC as key metric but respectfully disagree that this is a barrier for IREN, much rather the opposite and what strengthens IRENs moat. They are structurally capable of getting companies to compute quickly with their infrastructure set up almost a decade ago. Pre-payments or financing are not the issue, like Dan has said, they don’t just have idle GPUs sitting around. I own both to be clear as the future needs AI infrastructure/compute, but disagree with a lot of this NBIS superiority talk. It’s a classic case of banging loudly related to recent stock price action/deals announced, than anything actually material imo.

English

@Asymmetry_X yes access to power is important, but the KEY like Dan Roberts says is actually not power but rather time-to-compute. In order for $IREN to accelerate time-to-compute they need another deal which will provide the pre-payments to continue the buildout.

English

Wells Fargo sees $NBIS at 7.5GW of ACTIVE capacity by 2030 🔥

What would that mean for Nebius market cap and stock price?

Wells Fargo now projects Nebius will have 7.5GW of fully deployed activated GPUs.

At ~10M per MW revenue that would equate to ~75B ARR by 2030.

Using a conservative valuation multiple of 5X ARR we would be looking at ~375B market cap company by 2030.

(That’s ~12.9X the current market cap of ~29B)

Let’s estimate share count to be ~350M by 2030 accounting for additional dilution.

This would yield a stock price of ~$1,071 a share

$NBIS long game

NFA (Always do your own research)

Marc@NeuralCadence

I would not add the 5 GW+ Nvidia commitment on top of existing plans. I see it more as the total number going into 2030. But maybe Wells Fargo knows more. $NBIS

English