Sabitlenmiş Tweet

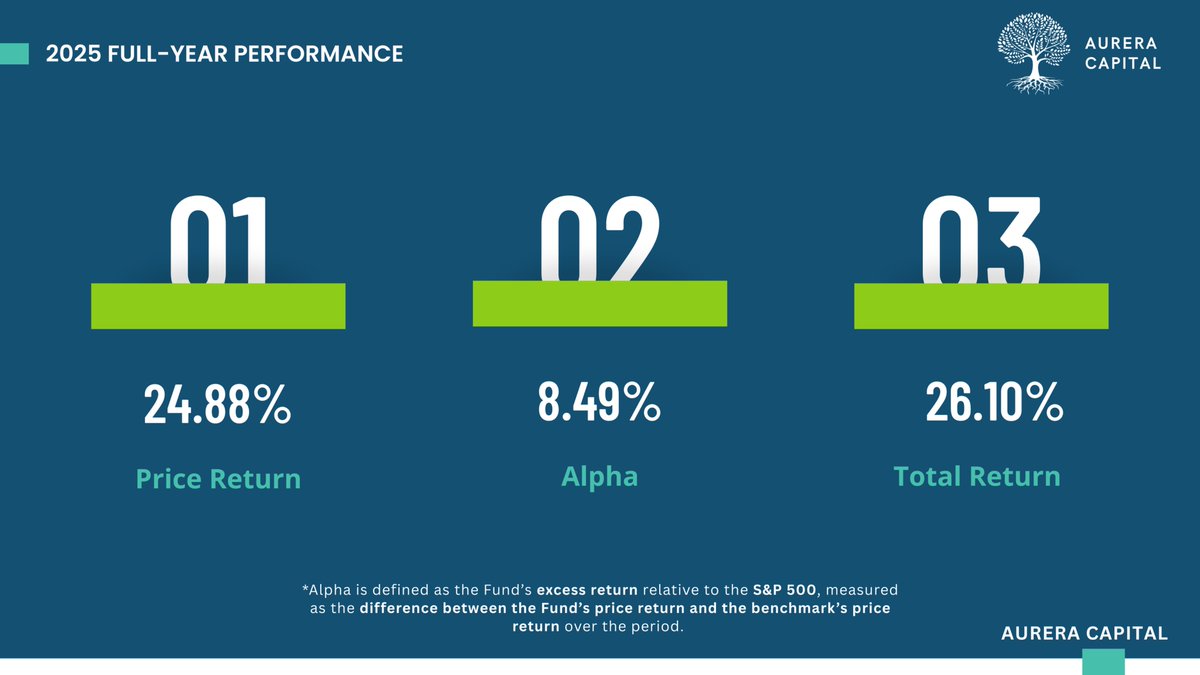

1/4 - Aurera Global Equities Fund — 2025 full-year: +24.88% price return vs the S&P 500 (benchmark) + 16.39%. That's 8.49% of outperformance, delivered with a concentrated 15-position book. The Fund's +26.10% total return represents price appreciation plus dividends.

English