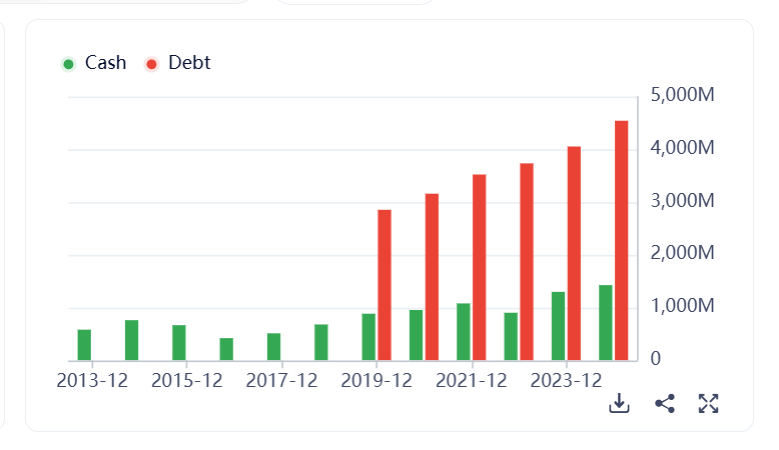

I am long $TOYO. I argue it is easily worth $2B just on it's Houston facility and section 45X credits. It makes $80M in annual tax credits today on a $558M mkt cap, and the market isn't pricing any growth.

Check out my in depth analysis below:

open.substack.com/pub/gabrielcor…

English