J Beck

250 posts

J Beck

@BeckJD_

Macro Economics. Game Theory. Bayesian Probabilities. VX Term Structure. Uncertainty. ie, The Road to Serfdom is a Markov Path.

Katılım Şubat 2020

127 Takip Edilen35 Takipçiler

According to @awealthofcs, government debt is up from $430 billion when this magazine cover came out to nearly $40 trillion today. That is almost a 10x.

English

The "stand-off" on the Straight is somewhere between the Dem/Repub battles on 1) a gov't shut-down and 2) the debt ceiling.

First, there’s a fair amount of game theory in all three of these that encourages holding out. Which side can declare victory? What are the costs incurred along the way? Certainly, Trump’s flagging approval rating and his party’s worries on midterms is a factor.

With the Straight stand-off, there’s not the danger presented by a true drop dead date that comes with the debt ceiling. Time is not truly of the essence in that way. But time does matter, inviting more uncertainty along the way.

While there’s not a date certain, keeping the Straight closed imposes more uncertainty and damage than does a run of the mill gov't shutdown.

When I look at this through my lens of 4 risk dimensions (economic, monetary, financial and geopolitical), I think the immediacy of a financial risk event that market prices like implied correlation and skew were telling us was possible is now lower.

The chart is a scatter plot of the VIX vs 1m 10 delta call vol on Brent. The VIX is lower now than it was a few weeks back with crude vol at the same level.

This immediacy of market risk has been transfered to slower moving but real economic risk. That is, the damage that keeping energy prices this high may inflict on the globaly economy, especially as so much supply is being taken off the market. We may not see this impact until months later

English

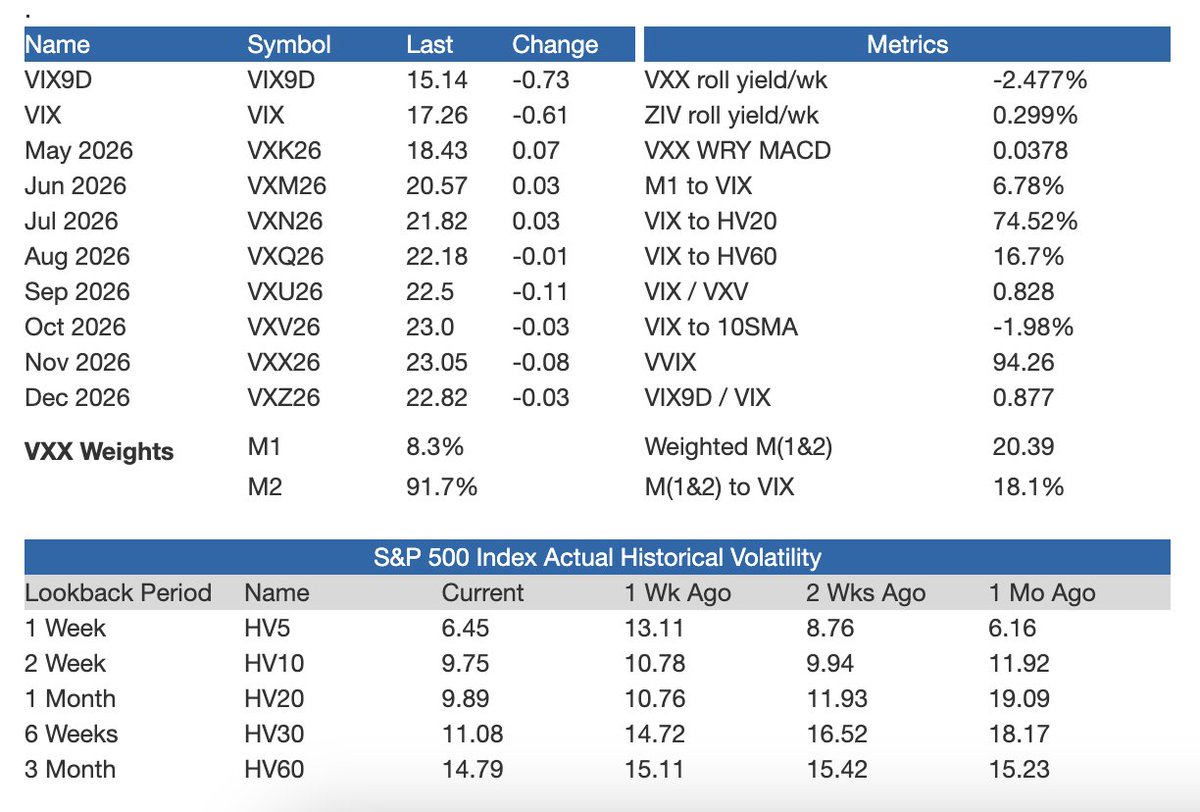

@Jbuehler777 @ZeeContrarian1 As a VX curve MM trader, you are correct. The daily adjustment in STPs always reflect the SPVXSTR index with an equal sensitivity to the underlying.

Z is usually pretty good, not sure what he's saying here.

English

@ZeeContrarian1 I would disagree a bit.. it reduces the sensitivity to spikes of the front month future.

As it's kept a constant 30 day out from $VIX Cash.. the sensitivity to $VIX Cash spikes should stay constant or am I missing something here?

English

@VIXandMore Add to this the actual non-seasonally adjusted change in payrolls for Jan was -2,649,000 jobs...

English

@VIXandMore Yeah that was a good call on Jan 2. Plus ~6830 is the 50 dma. Interesting to see if that holds thru the day.

Important to hold the Dec lows of 6720 in Jan/Q1.

English

Today’s early low (so far) of $SPX 6837 confirms the importance of 6830 as a key support level $VIX

Bill Luby@VIXandMore

Strong chance $SPX 6830 is the first meaningful bottom of 2026

English

@6_Figure_Invest @DaveNadig Storyful (among others) appear to be a good resource to verify / authenticate videos. Used by WSJ and FT.

(For now rapid hand movements with fingers staying aligned is an initial tell...)

English

@DaveNadig I suppose it could be AI-generated, but it certainly looks real...

English

Totally normal. I'm sure the fox was somehow "resisting arrest" or "disrupting an official proceding."

Molly Ploofkins@Mollyploofkins

I mean, c'mon

English

@vixologist @6_Figure_Invest I have around $2.2 B ETP VX_F exp yesterday on the main 30da longs and a recent peak of ~$3.5 billion on 10/7 (China tweet) with VXX at $1.1 B vs ~$.8 B on ~Mar 12.

English

@6_Figure_Invest I see less than half of that $5B out there now and that includes full AUM for $SVOL that doesn't have full exposure to VIX futures. Do you keep a running total?

English

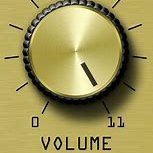

Open interest in VIX futures has never regained their 2017 highs.

English

🧵 on the entire Volatility ETP landscape

All the main products, their 20 year performance, and which part of the VIX Futures Term Structure they track

Follow along, bookmark, and let's find your favourite Vol ETP

English

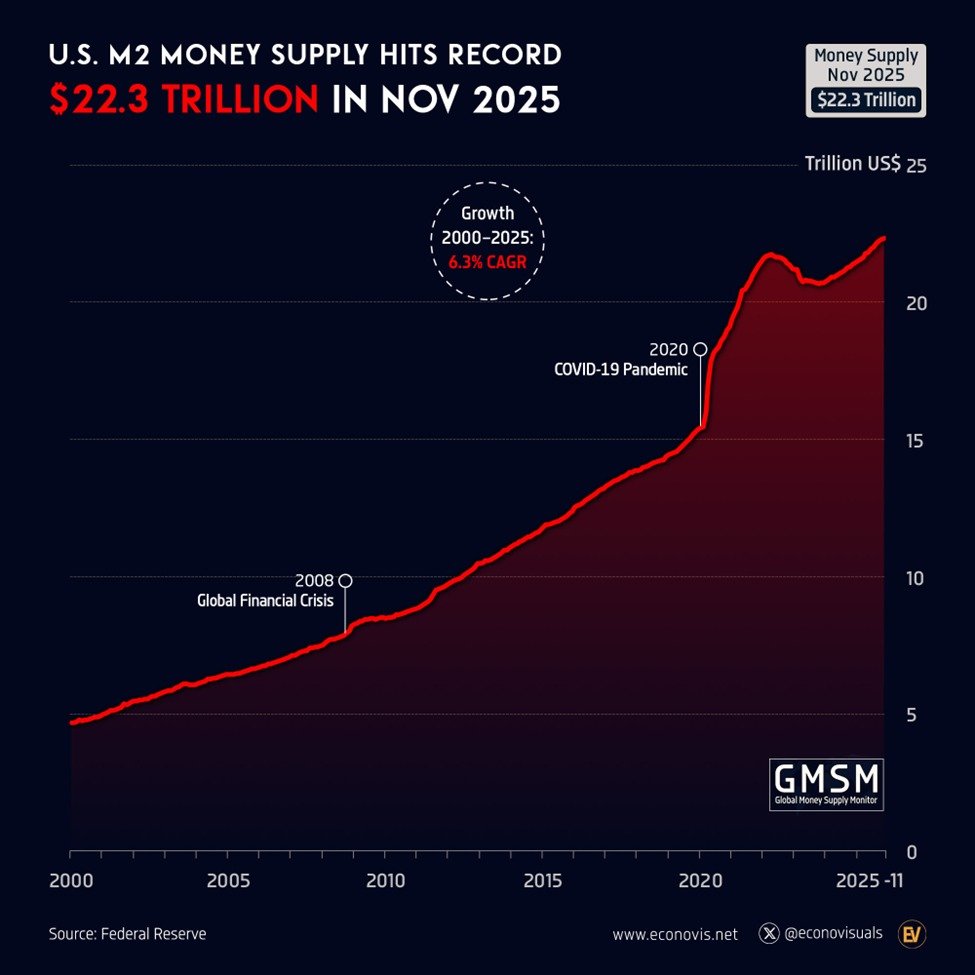

BREAKING: US M2 money supply rises another +4.3% YoY in November 2025, to a record $22.3 trillion.

This marks the 21st consecutive monthly increase.

Money supply is now $400 billion above the March 2022 peak.

Since 2000, money in circulation has grown at an average rate of +6.3% per annum.

Meanwhile, inflation-adjusted M2 rose +1.5% YoY in November, marking its 15th-straight monthly increase.

The US Dollar's purchasing power is deteriorating.

English

@VolSignals About half of Fed days occur on Vix Exp and 2 days before OpEx. Using actionable constant 30da with ETPs and Vix Ops may be more consistent/less noise.

Telegraphed FOMC 12-10 will lead to emphasis on NFP on 12-16 and CPI on 18. (exp 17) Likely this month's vol buildup.

English

8 FOMC Meetings in the last 12 months.

On average, the VIX rose .84 points after the Fed.

(this includes Dec'24... an outlier)

If we remove Dec 19, 2024 (+11.75 change) from the dataset,

then on average the VIX declines .70 points after FOMC.

HOWEVER >>

REGIME MATTERS

High vs low VIX matters.

If we bucket the observations by VIX < 19 and VIX > 19 then we have better information about what to expect.

Why 19?

Simple- 19.02 happens to be the simple average level of the VIX over the last 12 months.

HIGH VOL OUTCOMES

As you (should) expect, when VIX is on the higher end of its average, it tends to decline after FOMC.

Of 8 meetings, there were 3 meetings in which VIX was above 19 going into Fednesday:

March 19, 2025

May 7, 2025

June 18, 2025

ON ALL 3 OCCASIONS the VIX dropped between the close of trading on Tuesday (FOMC eve) and Wednesday (post FOMC).

AVERAGE CHANGE IF VIX > 19:

–1.49 points

LOW VOL OUTCOMES

Logic would have it that volatility cannot CRUSH from low levels. Since the world likes to ignore logic, let's look at empirical evidence.

Of 8 meetings, there were 5 meetings in which VIX was below 19 going into Fednesday:

December 19, 2024

January 29, 2025

July 30, 2025

September 17, 2025

October 29, 2025

ON 3 OF 5 OCCASIONS the VIX rose between the close of trading on Tuesday (FOMC eve) and Wednesday (post FOMC).

AVERAGE CHANGE IF VIX < 19:

+2.25 points

okay, okay- let's remove December '24 again, because it's an outlier.

You can leave it to your conscience as to how you to want to factor it into your decision making.

ON 2 OF 4 OCCASIONS (EX-DEC'24) the VIX rose between the close of trading on Tuesday (FOMC eve) and Wednesday (post FOMC).

AVERAGE CHANGE IF VIX < 19 (EX-DEC'24):

–0.12 points

the asymmetry just doesn't favor the vol-crushooors

English

@HayekAndKeynes Would be interesting to see the cost/price chart of the tomato soup in terms of average minutes of work to purchase since 1895. (ie. 2.7 mins of wages in 2025)

English

“One of the more straightforward ways to show debasement is via the price of Campbell’s tomato soup. Rather than relying on a complex set of estimates and substitutions, it’s just a history record of what the same can of soup cost over time.”

Lyn Alden@LynAldenContact

My December macro newsletter is now available. It discusses the debasement trade, changing macro conditions, and the large dislocation between the economy and markets. lynalden.com/december-2025-…

English

@VIXandMore Plus 1 mo RV is just 13. Market is really tensing up. Some is Nvda on Wed, but not all. IV of ~18 also seems high.

VIX is close to a ~6 mo high. (Oct 16)

English

This is a periodic reminder that a $VIX of 24 translates to an expected average daily move of 1.5% in the $SPX over the next 30 days. Right now SPX is down 1.3% for the day, so if a VIX of 24 is warranted, most days ahead will be more volatile than today. Call me skeptical.

English

@VIXandMore Right. The Kospi fever seemed to break quickly tho and retreat.

Makes you wonder if yesterdays US drop plus Asia night action is enough of a short term (Fed/AI) clearing event.

English

While this will look like a great call on the $SPX chart, it is worth noting that the /ES futures fell as much as 55 points in the first six hours after the close of regular trading. $VIX

Bill Luby@VIXandMore

Nibbling long at the retest of $SPX 6766 as the $VIX and VIX futures remain much more subdued compared to the bottom in stocks just after the open

English

@VIXandMore But the equal wait is down about .75%. This is somewhat an Nvdia and Mag 7 distortion today.

However Wed & Thurs are big event days so expected higher VX_1,2 vs curve.

CNN F+G still in Fear zone..at record highs..

English