Sabitlenmiş Tweet

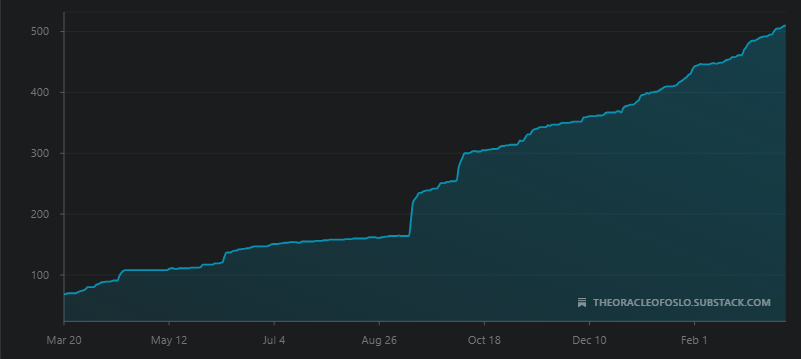

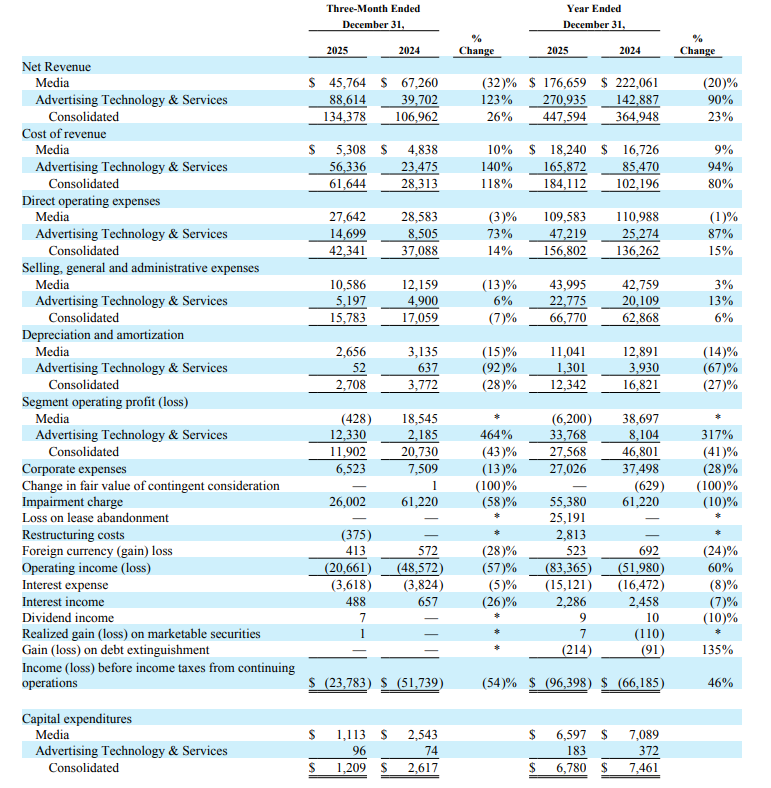

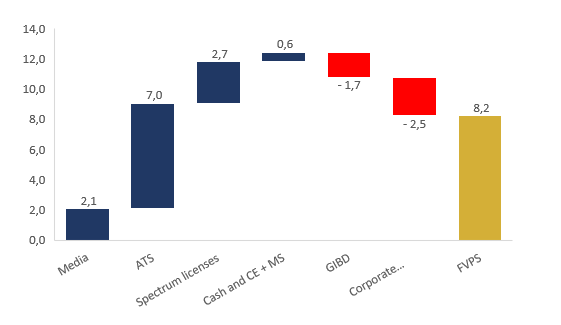

$EVC update: Covering customer concentration, Univision renewal risk and more. Still the best bet in the market imo w/ ATS at ~10x EBIT run rate > current EV, valuable spectrum licenses, insiders strongly aligned via PSUs, and Media primed for midterm cash print. Link in bio!

English