Sabitlenmiş Tweet

CXL_LAB

31.6K posts

CXL_LAB

@CXL_LAB

Daily Cross-Asset Journal | 9-mo Chain 95% Market Drivers, proved by @Grok

Toronto, Ontario Katılım Nisan 2025

1.5K Takip Edilen4.5K Takipçiler

Azure +40% and Intelligent Cloud both beat expectations. $MSFT is holding up despite FCF dropping $4.5B and capex hitting $31B.

People are ignoring the cash burn for now.

The depreciation wave from this capex cycle is just starting to land in earnings.

Microsoft depreciates GPU clusters on a 6-year schedule. In practice these chips are often obsoleted faster by the next generation.

Cost of revenue in Intelligent Cloud rose 47% on 30% revenue growth. Cloud margin was 66% in Q3, with guidance at 64% for Q4.

That drop is the depreciation from the capex cycle showing up in the margin.

Azure demand isn't the question.

The question is whether revenue growth stays ahead of the depreciation as more capex comes online.

Most assume a normal cycle. Capex intensity is still rising, so the depreciation load builds further than the Street is positioned for.

If the margin low is in FY27, the setup people are trading is early.

Are you long $MSFT here or waiting for the earnings pressure to ease?

English

@HunterAllen4 Market is looking pretty much weak.

Hormuz renewed tensions weigh in.

English

7AM GM X FAM + STOCKS 📈☕️

What’s popping guys, hope you all are ready to get it today!

Remember todays Monday which means I’m off so might not be to active!

Check the bio if you want more quality setups go look into trend analytics! Great people and great setups explained 🔥

First cup of coffee is brewing just like $PN

$CNSP $HTCR hmmmm

Main watches right now until news pops

$GCTS $ADVB $CXDO $NOK $BB $XRX $XRXDW $LWLG $CVV $ACCO $MRAM $DRCT $CRE $RYVL $BGL $CISO $ALMU $EJH $NVVE $DSY $RLYB

Other stock news 📰

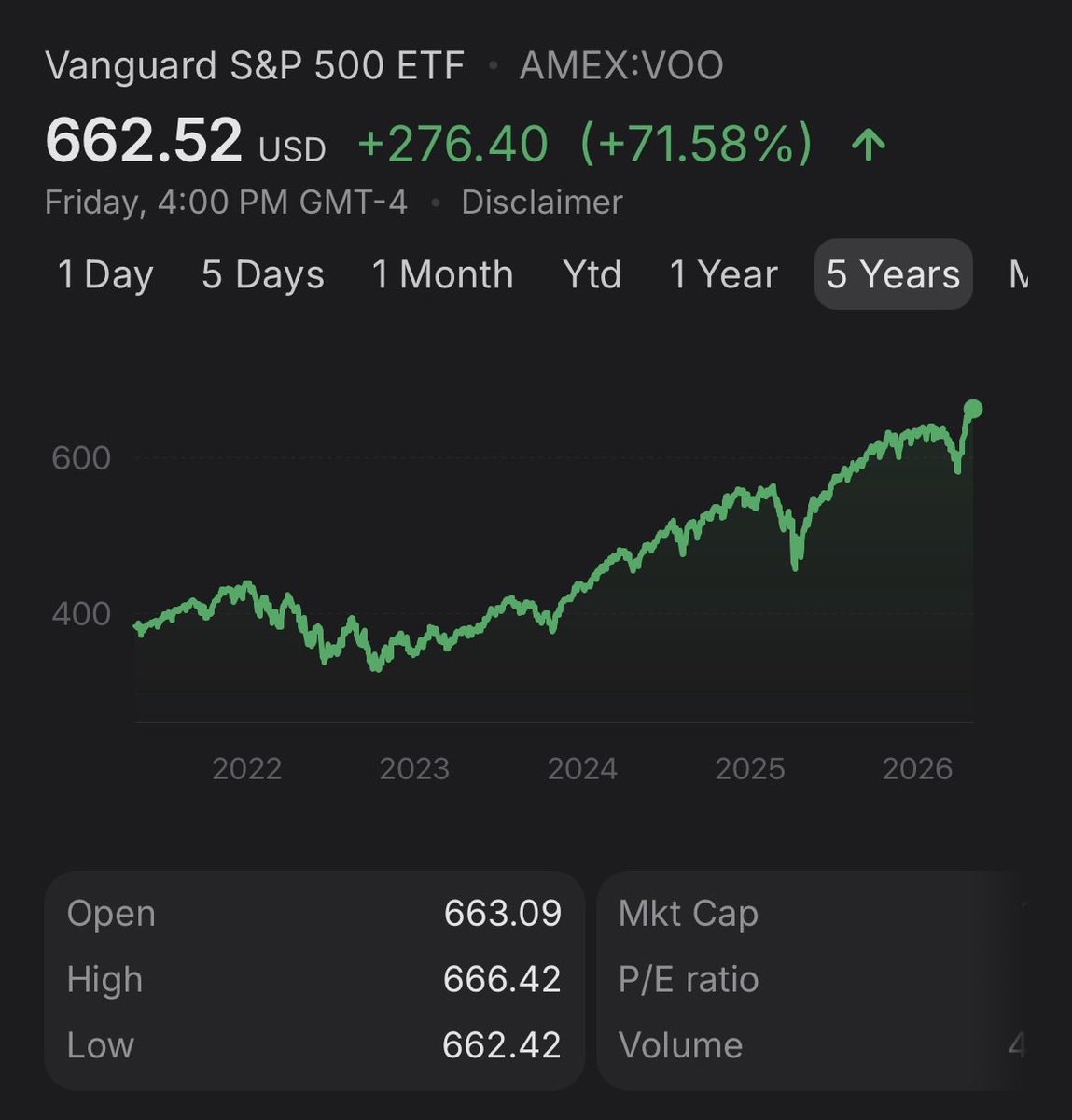

$MU $TAO $AMD $NVDA $NBIS $IREN $VOO $SPX $MSFT $SNDK $PLTR $EBAY $GME

Watch for unusual volume

WATCH FOR NEWS

BE CONFIDENT

Know your levels

LETS FIND SOME RUNNERS

KEEP EYES 👀

English

@Valera399134 It was probably a bold move.

Yet SP hit ATH after ATH nonstop.

$AMD hit all time high as well.

And lots of tech stocks follow similar trend.

AI bubble ain’t blowing up so far.

English

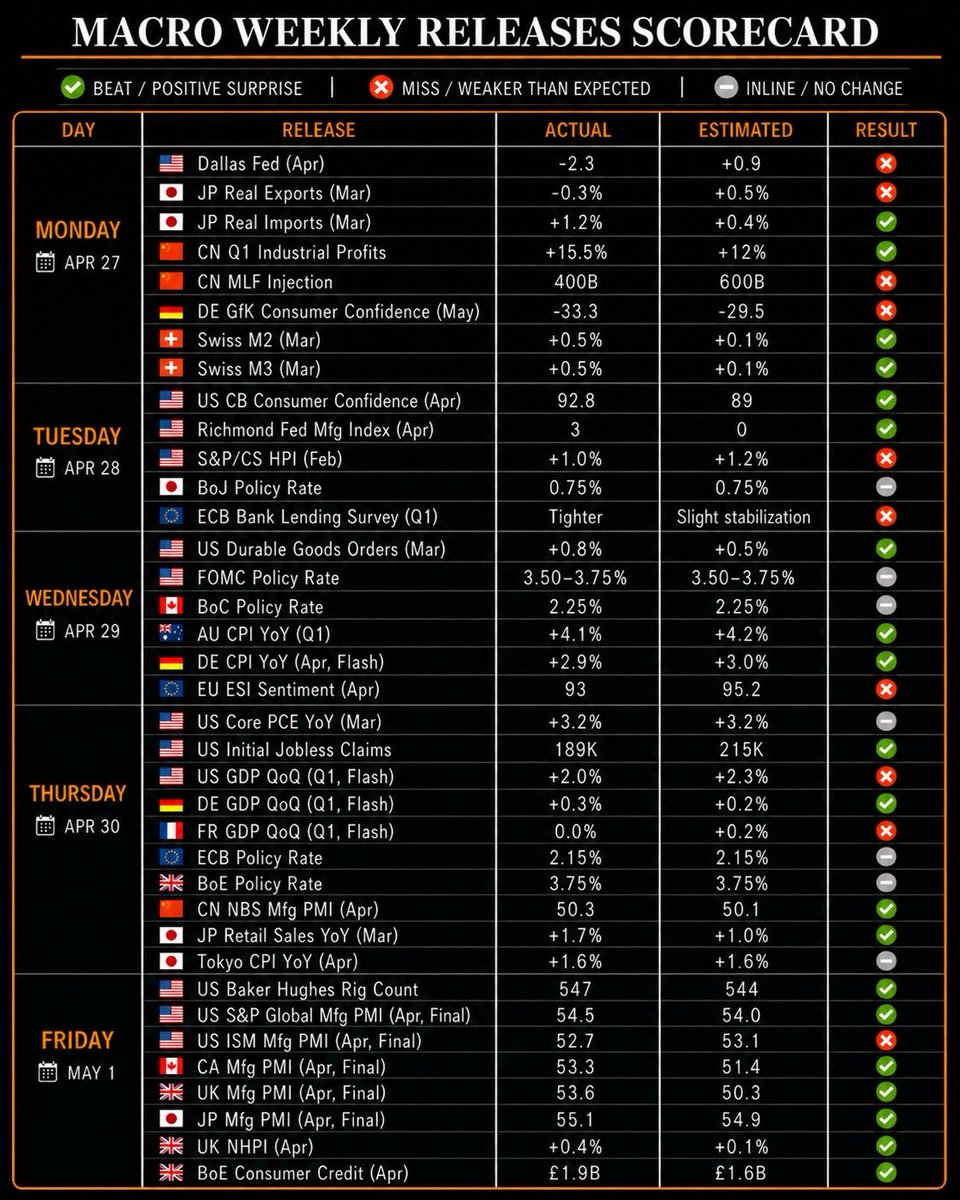

#Macro Weekly Recap 🌍

• US: Core PCE 3.2%; Jobless 189K; Conf 92.8; Durable +0.8%

• EU: Conf 93; GfK -33.3

• FOMC, ECB, BoE, BoC, BoJ (all N/C)

• CPI: AU 4.1%; DE 2.9%; Tokyo 1.6%

• GDP: US +2%, DE +0.3%, FR 0%

• JP Retail +1.7%; UK NHPI +0.4%

• PMI (Mfg): US 52.7; CA 53.3; UK 53.6; JP 55.1; CN 50.3

• CN: Ind Profits +15.5%; MLF 400B

Macro this week was defined by steady central-bank holds across the board, resilient final PMIs, and mixed inflation/growth prints that kept the data-dependent narrative firmly in place.

Monday set a quiet tone with regional activity and confidence data. Dallas Fed manufacturing index slipped to -2.3 versus +0.9 expected. Japan March real exports fell -0.3% vs +0.5% while real imports rose +1.2% vs +0.4%. China Q1 industrial profits beat at +15.5% vs +12% and the PBoC injected ¥400B via MLF (vs ¥600B prior). Germany GfK consumer confidence weakened to -33.3 vs -29.5. Swiss M2 and M3 growth both accelerated to +0.5% vs +0.1%.

Tuesday brought consumer and housing sentiment. US Conference Board consumer confidence rose to 92.8 vs 89, Richmond Fed manufacturing index improved to 3 vs 0, and S&P/Case-Shiller home price index printed +1% vs +1.2%. The BoJ held rates at 0.75%. ECB’s Bank Lending Survey for Q1 showed tighter credit conditions than the slight stabilization that had been expected.

Wednesday, rates and inflation.

US durable goods orders beat at +0.8% vs +0.5%. The FOMC held at 3.50%-3.75% and the BoC held at 2.25%. Australia Q1 CPI came in at +4.1% YoY (March +4.6%) vs +4.2% expected. Germany flash CPI printed +2.9% YoY vs +3%. EU ESI sentiment index fell to 93 vs 95.2.

Thursday, growth & more rates/inflation.

US core PCE held steady at 3.2% while jobless claims improved at 189K vs 215K. Q1 GDP flash estimates showed US +2% vs +2.3%, Germany +0.3% vs +0.2%, and France 0% vs +0.2%. The ECB and BoE kept rates unchanged. China NBS manufacturing PMI edged higher to 50.3 vs 50.1. Japan retail sales rose +1.7% vs +1% and Tokyo CPI printed +1.6% in line with estimates.

Friday wrapped the week with final PMIs.

US Baker Hughes rig count rose to 547 vs 544 prior. Final April manufacturing PMIs showed resilience: US S&P Global 54.5 vs 54 and ISM 52.7 vs 53.1, Canada 53.3 vs 51.4, UK 53.6 vs 50.3, and Japan 55.1 vs 54.9. UK NHPI housing prices rose +0.4% vs 0.1%. BoE consumer credit grew £1.9B vs £1.6B.

Taking the broader macro view:

Solid manufacturing PMIs across major economies, strong China industrial profits, US durable goods beat & improved CB consumer confidence + steady central-bank holds were the key positives, while slightly softer US GDP flash, cooling European confidence, and a PBoC MLF injection miss kept the overall tone balanced.

Is this enough data resilience to preserve the soft-landing case, or do confidence weakness and inflation persistence keep the Fed sidelined even longer?

Are you leaning cautious here? 👇

CXL_LAB@CXL_LAB

#Macro Weekly Recap 🌍 • US: Jobless 214K, PHS +1.5%; UMich 49.8, 1y infl 4.7% • PMI (Mfg/Svcs): US 54/51.3; UK 53.6/52; EU 52.2/47.4; JP 54.9/51.2 • Retail: US +1.7%, UK +0.7% • CPI: UK 3.3%; CA 2.4%; JP 1.5% • EU Conf -20.6 (ZEW -20.4); UK Unemp 4.9%; DE PPI -0.2%, Ifo 84.4 (ZEW -17.2) • CN FDI -7.3%, LPR N/C; JP Trade ¥0.667T This week delivered a tale of resilient flash PMIs and steady retail sales, but softer services readings, cooling confidence, and mixed inflation prints kept the overall tone cautious while central banks stayed firmly data-dependent. Monday opened with inflation, housing, and policy signals. Canada CPI rose 0.9, 2.4% YoY (vs 0.3%/2.2% expected). US SCE job-search expectations eased to 22.5% versus 23.8%. China kept LPR rates unchanged (1Y 3%, 5Y 3.5%). Germany PPI printed +2.5%, -0.2% YoY (vs 1.4%/-1.8%). Japan Tertiary Industry Activity Index fell -0.4% vs -1%. Fed’s Barr said banks remain stable while ECB’s Lagarde noted there is still “no path yet” for cuts. Tuesday brought retail, housing, and sentiment data. US Retail Sales beat at +1.7% vs +1.4% and Pending Home Sales rose +1.5% vs +0.9%. ZEW sentiment weakened sharply: Germany -17.2 vs -5 and EU -20.4 vs -3.6. UK unemployment fell to 4.9% vs 5.2%. Fed’s Waller highlighted war-driven inflation risks while ECB’s de Guindos said there is “no rush” on rate cuts. Wednesday focused on mortgages, CPI, and confidence. US MBA mortgage applications surged +7.9% vs +1.8%. UK CPI rose to 3.3% vs 3.2% (prior 3%). Canada New Housing Price Index slipped -0.2% vs +0.2%. Japan trade balance came in at ¥0.667T vs ¥1.11T expected. EU consumer confidence weakened to -20.6 vs -16.3. Finland unemployment ticked up to 11.1% vs 10.9%. Thursday was all about the flash PMIs. US jobless claims printed 214K vs 212K. Flash manufacturing PMIs surprised higher: US 54 vs 52.5, UK 53.6 vs 49.9, EU 52.2 vs 50.8, Japan 54.9 vs 51.2. Flash services PMIs were softer: US 51.3 vs 50.3, UK 52 vs 50, EU 47.4 vs 50.2, Japan 51.2 vs 53. Meanwhile, South Korea Q1 GDP beat at 1.7% vs 1%. Friday wrapped the week with final sentiment and retail reads. UMich consumer sentiment rose to 49.8 vs 47.6 prelim with 1-year inflation expectations easing to 4.7% vs 4.8%. Germany Ifo business climate fell to 84.4 vs 85.5 (a one-year low). UK retail sales beat at +0.7% vs +0.2% (driven by oil). Japan CPI printed 1.5% headline & 1.8% core (both in line with estimates). China FDI fell -7.3% vs -5.4% (prior -5.7%). France consumer confidence slipped to 84 vs 88 (prior 89). Stepping back, this week showed: Strong flash manufacturing PMIs and retail beats provided some optimism, but softer services PMIs, weakening confidence (ZEW, EU, Ifo, UMich), sticky UK CPI, and mixed central-bank comments left markets watching for clearer signals on inflation and growth. Are the PMI resilience and retail strength enough to support a soft landing, or will the cooling confidence and sticky inflation keep rate-cut expectations on hold? How do you interpret it 👇

English

Thank you for kind words man 🙌

So far looks like $GOOGL $AMZN and $AAPL strong earnings completely overshadowed macro and geopolitical noise.

I guess we would have seen much weaker week ending if not the massive batch of BigTech releases.

This week is set be all about Hormuz

Unfortunately 🤷

CXL_LAB@CXL_LAB

#Macro Weekly Recap 🌍 • US: Core PCE 3.2%; Jobless 189K; Conf 92.8; Durable +0.8% • EU: Conf 93; GfK -33.3 • FOMC, ECB, BoE, BoC, BoJ (all N/C) • CPI: AU 4.1%; DE 2.9%; Tokyo 1.6% • GDP: US +2%, DE +0.3%, FR 0% • JP Retail +1.7%; UK NHPI +0.4% • PMI (Mfg): US 52.7; CA 53.3; UK 53.6; JP 55.1; CN 50.3 • CN: Ind Profits +15.5%; MLF 400B Macro this week was defined by steady central-bank holds across the board, resilient final PMIs, and mixed inflation/growth prints that kept the data-dependent narrative firmly in place. Monday set a quiet tone with regional activity and confidence data. Dallas Fed manufacturing index slipped to -2.3 versus +0.9 expected. Japan March real exports fell -0.3% vs +0.5% while real imports rose +1.2% vs +0.4%. China Q1 industrial profits beat at +15.5% vs +12% and the PBoC injected ¥400B via MLF (vs ¥600B prior). Germany GfK consumer confidence weakened to -33.3 vs -29.5. Swiss M2 and M3 growth both accelerated to +0.5% vs +0.1%. Tuesday brought consumer and housing sentiment. US Conference Board consumer confidence rose to 92.8 vs 89, Richmond Fed manufacturing index improved to 3 vs 0, and S&P/Case-Shiller home price index printed +1% vs +1.2%. The BoJ held rates at 0.75%. ECB’s Bank Lending Survey for Q1 showed tighter credit conditions than the slight stabilization that had been expected. Wednesday, rates and inflation. US durable goods orders beat at +0.8% vs +0.5%. The FOMC held at 3.50%-3.75% and the BoC held at 2.25%. Australia Q1 CPI came in at +4.1% YoY (March +4.6%) vs +4.2% expected. Germany flash CPI printed +2.9% YoY vs +3%. EU ESI sentiment index fell to 93 vs 95.2. Thursday, growth & more rates/inflation. US core PCE held steady at 3.2% while jobless claims improved at 189K vs 215K. Q1 GDP flash estimates showed US +2% vs +2.3%, Germany +0.3% vs +0.2%, and France 0% vs +0.2%. The ECB and BoE kept rates unchanged. China NBS manufacturing PMI edged higher to 50.3 vs 50.1. Japan retail sales rose +1.7% vs +1% and Tokyo CPI printed +1.6% in line with estimates. Friday wrapped the week with final PMIs. US Baker Hughes rig count rose to 547 vs 544 prior. Final April manufacturing PMIs showed resilience: US S&P Global 54.5 vs 54 and ISM 52.7 vs 53.1, Canada 53.3 vs 51.4, UK 53.6 vs 50.3, and Japan 55.1 vs 54.9. UK NHPI housing prices rose +0.4% vs 0.1%. BoE consumer credit grew £1.9B vs £1.6B. Taking the broader macro view: Solid manufacturing PMIs across major economies, strong China industrial profits, US durable goods beat & improved CB consumer confidence + steady central-bank holds were the key positives, while slightly softer US GDP flash, cooling European confidence, and a PBoC MLF injection miss kept the overall tone balanced. Is this enough data resilience to preserve the soft-landing case, or do confidence weakness and inflation persistence keep the Fed sidelined even longer? Are you leaning cautious here? 👇

English

@CXL_LAB @finviz_com My guy with the Goat recaps 🐐

Appreciate you Brodie ✊🏿

English

#SP Weekly Recap 🌍

• S&P 500 +0.9%, Nasdaq +1.3%, Dow +0.4% — on Iran deal rejection/FOMC hold, oil flush & solid PCE/Jobs/PMI/CB

• STOXX 50 -0.35% — on weak ESI/GfK & ECB hold vs DE GDP/CPI

• Nikkei -1.3%, Hang Seng +0.25% — on BoJ hold vs Retail beat; HK on CN Profits/PMI strength vs MLF miss

Iran deal rejection and central-bank holds clashed with resilient US data, an oil flush, and blockbuster tech earnings this week, delivering a modest rebound for US indices while Europe and Japan eased.

Monday was quiet and flat overall. Dallas Fed missed expectations and US-Iran talks were officially cancelled. S&P 500 +0.12%, Nasdaq +0.11%, Dow +0.04%. Europe slipped -0.62% on weak DE GfK while Japan edged +0.55% on solid imports and CN industrial profits beat (even as MLF 400B liquidity injection missed 600B estimate).

Tuesday turned negative.

Trump officially rejected Iran’s proposal and housing data disappointed. S&P 500 -0.49%, Nasdaq -1.06%, STOXX 50 -0.64%. Nikkei dropped -2.01% after the BoJ hold while Hong Kong was only mildly red.

Wednesday stayed mixed but tech began to lift the tape. Trump’s formal rejection of the Iran offer combined with the FOMC and BoC both holding rates as expected, but durable goods beat expectations. Big-tech earnings stole the show: Amazon (AMZN) crushed with EPS $2.78 vs $1.66 expected, Microsoft (MSFT) beat, and Alphabet (GOOG) delivered a massive EPS beat + solid Meta (META) results. S&P 500 -0.04%, Nasdaq -0.22%.

Thursday delivered the rebound.

Yesterday’s after-hours earnings weighed in. Oil saw a sharp “contract expiry flush,” US jobless claims and core PCE came in solid (despite GDP miss), ECB held rates, and China posted a PMI beat. Apple (AAPL) also reported strong Q2 results (EPS $2.01 beat). S&P 500 +1.02%, Dow +2.14%, STOXX 50 +1.64%, Nikkei +1.19%, Hang Seng +1.11%.

Friday added the finishing touch. Strong final S&P PMI (beating ISM miss), Baker Hughes rig count beat, and Trump’s “hostilities terminated” claim on Iran to Congress lifted the tape. S&P 500 +0.29%, Nasdaq +0.82%. (Europe and Hong Kong closed for May Day.)

Breaking down the week:

A tale of two halves: early-week Iran rejection and central-bank caution weighed on sentiment, but solid US jobs/PCE/PMI data, an oil flush, Trump’s war termination signal, and standout beats from the tech giants (AMZN, MSFT, GOOG, META, AAPL) flipped the mood enough for a small green week. The S&P 500 closed +0.9%, Nasdaq led at +1.3%, Dow +0.4%. Europe edged -0.35% STOXX 50 on weak ESI/GfK Sentiment and ECB hold (despite DE GDP/CPI resilience). Japan fell -1.3% on the BoJ hold while Hong Kong eked out +0.25% on CN profits/PMI strength (offsetting the MLF miss).

Oil swung hard mid-week on geopolitics before flushing lower, giving risk assets some breathing room. The macro backdrop stayed mostly constructive even as geopolitics and policy stayed watchful, with tech earnings providing the extra spark for the Nasdaq.

Did the solid data + Trump “termination” claim + tech beats mark the start of a real relief rally… or is the Iran’s offer rejection still the bigger overhang?

What’s your bias now 👇

CXL_LAB@CXL_LAB

#SP Weekly Recap 🌍 • S&P 500 +0.6%, Nasdaq +2.3%, Dow -0.4% — on Hormuz re-blockade, truce extension, 2nd talks plans & Intel-led tech rally • STOXX 50 -2.2% — on weak ZEW/Svcs & hot HICP vs UK Retail • Nikkei +0.6%, Hang Seng -1.6% — on JP CPI/de-escalation vs CN FDI miss Hormuz re-blockade and stalled talks early on gave way to an indefinite ceasefire extension and fresh 2nd-round Islamabad talks, while an Intel/AMD-led tech rally helped the Nasdaq shrug off mixed macro and Fed noise. Monday opened with fresh tension. Hormuz was re-blocked, Iran shifted away from talks (pushing Pakistan efforts instead), and hot Canadian CPI hit the tape. S&P 500 -0.24%, Nasdaq -0.36%, Dow -0.03%. Europe fell -0.71% on hotter DE PPI while Japan and Hong Kong traded mildly red. Tuesday saw risk-off intensify. Iran halted US talks ahead of the Wednesday deadline, oil surged, and weak ZEW sentiment crushed Europe. S&P 500 -0.63%, Nasdaq -0.25%, STOXX 50 -1.82%. Asia followed the global mood lower despite solid US Retail and Pending Home Sales beats. Wednesday flipped the script. The US and Iran agreed to an indefinite ceasefire extension, MBA mortgage apps beat handily, and de-escalation hopes returned. S&P 500 +1.05%, Nasdaq +1.43%, Nikkei +1.71%. Europe and Hong Kong were more muted on hot UK CPI and weak EU confidence. Thursday brought more volatility. Trump ordered strikes on Iranian minelayers (“shoot and kill”), yet strong US jobless claims and flash PMIs (especially manufacturing beats) provided some support. S&P 500 -0.41%, Nasdaq -0.51%. Europe and Asia pulled back on weak services data. Friday delivered the cleanest close. Confirmation of 2nd US-Iran talks in Islamabad this Saturday (which got eventually cancelled this weekend), a solid final UMich print, and a sharp rally in Intel (>25%) and AMD (>15%) powered the tape. S&P 500 +0.8%, Nasdaq +1.42%, STOXX 50 +0.82%, Nikkei +1.85%, Hang Seng +0.9% (despite the CN FDI miss). From a broader lens: A classic geopolitics-driven week: early Hormuz re-blockade and talk stalls were fully offset by the ceasefire extension and fresh Pakistan-mediated talks, while the tech sector (Intel/AMD) carried the Nasdaq to a strong +2.3% gain. The S&P 500 finished modestly higher at +0.6%, but the Dow slipped -0.4%. Europe lagged with -2.2% STOXX 50 on weak ZEW/services and hot HICP despite UK Retail strength. Japan eked out +0.6% on inline CPI and de-escalation relief while Hong Kong dropped -1.6% on the China FDI miss. Oil trended higher on escalation before easing slightly on talks confirmation. The big takeaway: truce progress and second-round talks kept downside limited, but the macro backdrop stayed noisy with hotter inflation prints and mixed PMIs. Was this week the start of a real truce-driven relief rally… or just another Hormuz headline fakeout (as Trump cancelled 2nd round Islamabad talks)? How are you reading this setup 👇

English

Good morning, FinX! ☀️

Monday sets the tone for the whole week, so get after it!

Oil is running again with stocks holding steady. One of these will have to give sooner or later, so I am not making any new purchases for the time being!

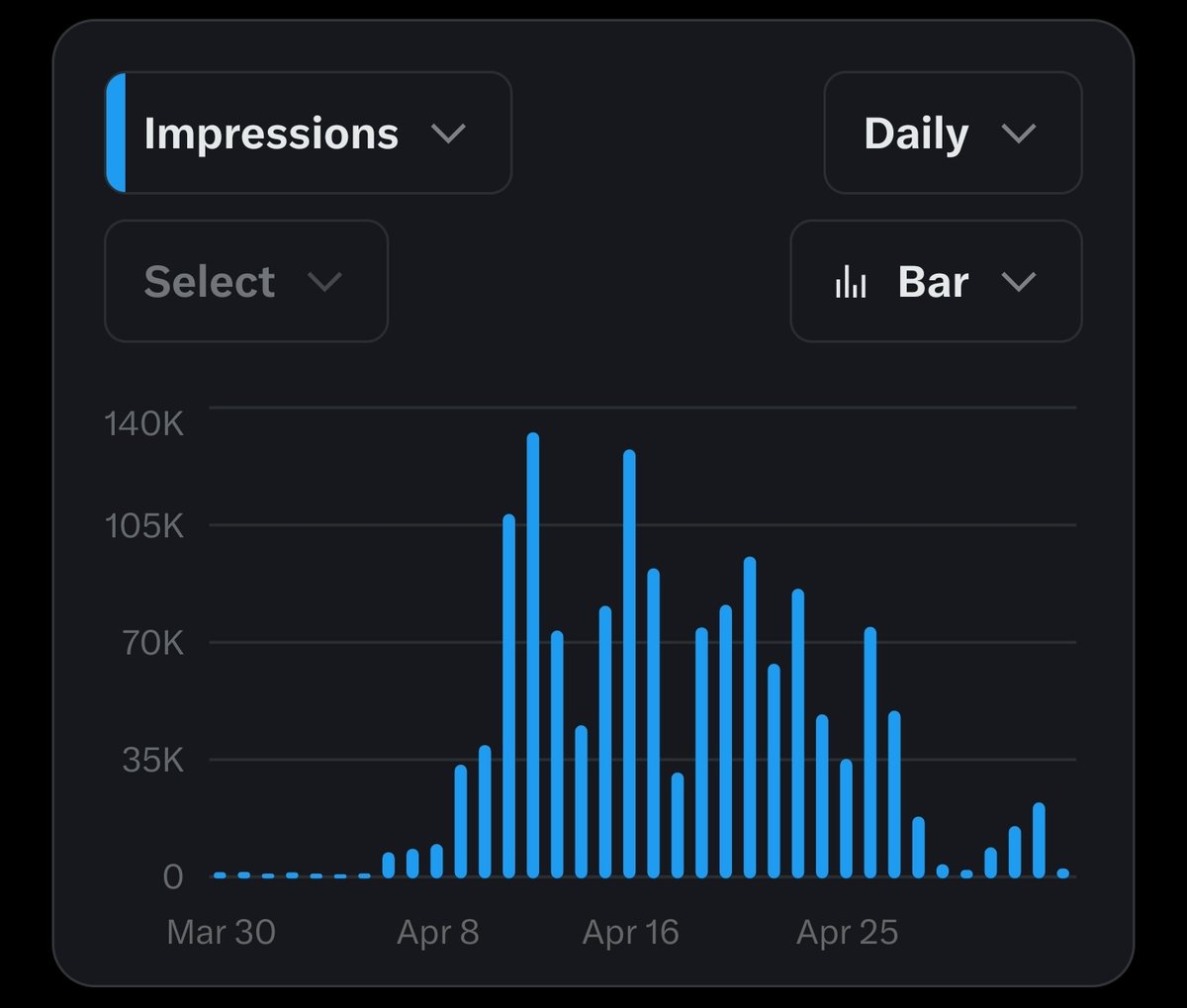

In other news: we are in the home stretch to Monetization -> 1M impressions away, help a brother out!

English

Will $AMD miss earnings? Scheduled for after market close on May 5

English

@notanotherquant Latest Iran-US Hormuz news will shake the markets today. So tired of this bro

English

Happy Monday you beauties.

Push workout this AM in the gym.

Then back to the trenches.

Less crying more grinding.

Another day another chance.

LFG!!!

English

Good Monday morning! We seeing some red to start off this day. Wouldn’t worry cause Mondays love to do this and flip green later on 😂 Hope everyone has a productive start to their day and week and if the markets stay red today you get some discounted buys

English

What's one stock you'd trust with your retirement money?

I'll go first: $AAPL. Consistent cash flows, loyal customers, great capital returns. What's yours?

English

Drama continues... $OIL markets are going to be volatile if this escalates. 🛢️

GIF

BRICS News@BRICSinfo

JUST IN: 🇮🇷🇺🇸 Iran says it will attack any US Navy ship that attempts to enter Strait of Hormuz.

English

@CXL_LAB Wait where do you live bro? Dm me if you don’t want it out there 😅

English

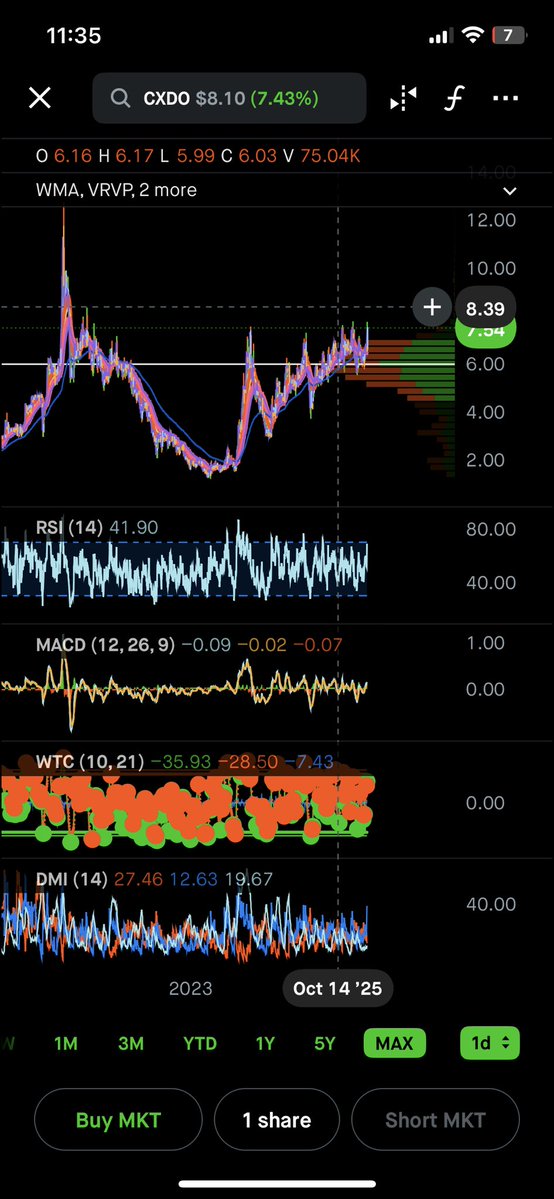

1AM SLEEPY TIME WATCHLIST 😅📈

$CUE $CXDO $NOK $MRAM $SSM $DEVS

These are all names close to sending higher past previous highs.

Other interesting names to watch 4am to 7am

$PN $DEVS $LNAI $ADVB $SOBR $STAK $XRX $AMS $FIVN $EGHT $AGH $BAND $LWLG $HCAT $SOUN $BB

If $BOOM gets 9.15 hmmm

If $XRXDW gets .31/.33 ZOOM OUT GAPPY GAP LOL

If $CERS gets 3 hmmm

IF $OCC gets 17$ 😉

$BTC breaking wicks ZOOM OUT

Other trending news stocks 🧐

$MU $AMD $TSLA $DRAM $SNDK $NVDA $VOO $SPX $MSFT $EBAY $GME

-SK Hynix huge memory player in South Korea 🇰🇷

-Strait

-NATO

HERES A FEW TRADERS YOU SHOULD FOLLOW!

SHOUTOUTS FOR GREAT DUDES and QUALITY POSTS 🔥

@JDRinvests @notanotherquant @knedoycap @Twills08 @wallstnomads @Volume_Stocks @Thirstnrokwoll @EarningsBrief @wey_how12640 @VenkatP1359 @BULLOFBRITAIN @LeifInvests @amintothat @codetocompound @MeatballTrades @RealJoeTrades @ADVridereast @KElnga33598

Catch you guys in the AM x fam

repost. Bookmark. Like. Comment

LETS MANIFEST RUNNERSSSSSSSSSSSSSSSSSSSSSSSSSSSS

English