cattlecapital

2.6K posts

cattlecapital

@CattleCapital

capital deployment and curiosity. compiling for myself, scroll at your own risk

Atlanta, GA Katılım Ağustos 2018

1.2K Takip Edilen222 Takipçiler

JUST IN: Trump is reportedly considering seizing control of Iran’s oil sector to gain trade leverage against China.

English

cattlecapital retweetledi

Scarcity dictates what’s meaningful.

ㅤ

When you are alone, a relationship feels meaningful. When you’re in a relationship, time to yourself feels meaningful.

ㅤ

When you are overworked, time off feels meaningful. When you have plenty of downtime, work feels meaningful.

ㅤ

The scarcity never gets solved, it simply changes form.

English

@KobeissiLetter We should 100% take the oil as compensation

English

BREAKING: President Trump says he believes he can "get a deal with Iran" by Monday and that Iran is "negotiating now."

Trump also says he is considering "blowing everything up" and "taking Iranian oil" if Iran does not make a deal "fast."

English

@LinkofSunshine It’s an ugly socialist gulag. We should test it down and sell to developers

English

Stuy Town is weird because it’s basically everything wrong with 50s urbanism (the kind of suburban idea that people want to live in these carefully planed communities instead of just natural city growth)

But honestly it was so well made that it still works great

Civixplorer@Civixplorer

Soviet-style blocks in New York City? The red-brick towers of Stuyvesant Town–Peter Cooper Village are post-WWII modernist designs, created to tackle the housing crisis.

English

@clashreport Actually when you kill bad people the world gets better. Don’t be stupid

English

French President Macron:

Iran is a very bad regime — no discussion about that. I disagree with them on a lot of topics.

But I don’t believe that we will fix the situation just by bombings or by military operations.

Look at what happened with this type of operation in Iraq, in Afghanistan, in Libya — we never delivered. Never. Even after 20 years.

So you have to respect the sovereignty of people. If people want to change a regime, they want to react, step up, they can do so.

English

New York is about to do a huge payoff to the teachers union, letting them retire at age 55 (instead of 62) and lowering their contribution rate from 4.5% to 3.5%.

This sweetheart deal will cost New York $1.5 billion.

Meanwhile, taxpayers are fleeing New York for other states with lower taxes.

English

cattlecapital retweetledi

Bad bonuses are absolutely a way of weeding people out

The only problem is that you will probably get rid of all the strong employees who you actually want at the firm, and leave behind the ones you don’t want

Also just an absolute disaster for culture when there is a mass exodus like this. Ends up hurting who you can recruit for the next time around

Short Squeez@shortsqueeznews

BREAKING: UBS canceled a round of junior layoffs because too many analysts and associates quit after bonuses were paid out. The firm reached its headcount target thanks to voluntary resignations. Reportedly most of the strong analyst/associates left while weaker ones stayed.

English

English

@CBSNews Only the ignorant and idiots believe more government funding makes things better

English

Sen. Elizabeth Warren's bill would raise taxes on households worth more than $50 million and on billionaires. cbsn.ws/4uO5CQJ

English

cattlecapital retweetledi

This is one of the best investing lessons from Warren Buffett

English

@LynAldenContact Always best to run the number on tax paying households. Because it’s a bigger number and the others don’t foot the bill

English

cattlecapital retweetledi

Japanese actor Hiroyuki Sanada spoke about the contradictions of human nature:

“Some people dream of having a swimming pool at home, while those who have one hardly ever use it. Those who have lost a loved one feel a profound sense of loss, while others often complain about their living relatives. Those without a partner long for one, while those who have one often don't appreciate it. The hungry would give anything for a meal, while the satiated complain about the taste of their food. Those without a car dream of owning one, while those who have a car are always looking for a better one.”

The key to happiness is gratitude: truly seeing and appreciating what we already have, and understanding that somewhere, someone would give anything for what we take for granted.

English

@Cthomsix @SpecialSitsNews Most people that I talk to that invest in alts do not know IRR is different than GAGR …

English

@SpecialSitsNews IRRs account for uneven cash flows, your assumption is fully invested geometric return like owing the S&P 500. Geometric return and IRRs are apples and oranges. Not arguing with your point, it may still stand, impossible to say because IRR and geometric avg aren’t comparable.

English

Most of these PE long term IRRs are fake...

If $KKR’s first $31 million fund from 1976 had compounded at 26% a year it would be worth $2.6 trillion today

x.com/i/status/20335…

Trevor Noren@trevornoren

Apollo's John Zito on private equity: "I literally think all the marks are wrong...This next cycle is going to be a big moment in time for the private markets because people are way smarter than I think private-market participants, particularly people in the wealth channel. Like, I kind of sense an arrogance of the people who grew up in the private-markets business . . . If you don’t mark your book, I think you actually lose trust with the clients." As I dissected in my report on the "Retailization of Private Markets" (sageroadresearch.com/collections/re…), it's dumbfounding how much enthusiasm for PE over the past decade+ was predicated on nakedly absurd performance assumptions. In an article in May, the FT dissected IRR claims made by both KKR and Apollo in 10-K filings. First, they quoted KKR: “From our inception in 1976 through December 31, 2024, our Private Equity and Real Assets investment funds with at least 24 months of investment activity generated a cumulative gross IRR of 25.5%, compared to the 12.2% and 9.5% gross IRR achieved by the S&P 500 Index and MSCI World Index, respectively, over the same period.” As for Apollo, it claims a 39% gross IRR generated by its private equity funds from inception through year-end 2024. The FT contextualized these numbers: "Across almost all regulatory and marketing material filed by private equity, awe-inspiring IRRs are common. Apparently, these private equity firms have managed to defy the laws of mathematics, economics—and reality. Since most people typically don’t have a good grasp of compounding, it might be helpful to express these numbers in dollars to show how fantastical they really are. If KKR’s first $31 million fund from 1976 had compounded at 26% a year it would be worth $2.6 trillion today. Add in its second $350 million fund and you get $13 trillion—more than the global PE market. Apollo’s first funds would now be worth $74 trillion, just shy of global GDP." Private credit problems could easily spill over into PE and finally force a reckoning with the "laws of mathematics, economics—and reality." To again quote Zito: “There’s . . . unlimited demand for secondary private equity but they are worried about private credit which finances 80% of those portfolios . . . I can’t compute, but I’m the dumb guy. I don’t understand. I start saying this and I get these blank stares back at me like OK, I don’t know.” This is a particularly acute concern for the broader US economy given the PE creep into small businesses over the past decade (chart below). Learn more about Sage Road Research: sageroadresearch.com. Interested in subscribing? Message me. WSJ interview with Zito: wsj.com/finance/invest… Chart source: bloomberg.com/news/articles/…

English

cattlecapital retweetledi

Apollo's John Zito on private equity: "I literally think all the marks are wrong...This next cycle is going to be a big moment in time for the private markets because people are way smarter than I think private-market participants, particularly people in the wealth channel. Like, I kind of sense an arrogance of the people who grew up in the private-markets business . . . If you don’t mark your book, I think you actually lose trust with the clients."

As I dissected in my report on the "Retailization of Private Markets" (sageroadresearch.com/collections/re…), it's dumbfounding how much enthusiasm for PE over the past decade+ was predicated on nakedly absurd performance assumptions. In an article in May, the FT dissected IRR claims made by both KKR and Apollo in 10-K filings. First, they quoted KKR: “From our inception in 1976 through December 31, 2024, our Private Equity and Real Assets investment funds with at least 24 months of investment activity generated a cumulative gross IRR of 25.5%, compared to the 12.2% and 9.5% gross IRR achieved by the S&P 500 Index and MSCI World Index, respectively, over the same period.” As for Apollo, it claims a 39% gross IRR generated by its private equity funds from inception through year-end 2024. The FT contextualized these numbers:

"Across almost all regulatory and marketing material filed by private equity, awe-inspiring IRRs are common. Apparently, these private equity firms have managed to defy the laws of mathematics, economics—and reality. Since most people typically don’t have a good grasp of compounding, it might be helpful to express these numbers in dollars to show how fantastical they really are. If KKR’s first $31 million fund from 1976 had compounded at 26% a year it would be worth $2.6 trillion today. Add in its second $350 million fund and you get $13 trillion—more than the global PE market. Apollo’s first funds would now be worth $74 trillion, just shy of global GDP."

Private credit problems could easily spill over into PE and finally force a reckoning with the "laws of mathematics, economics—and reality." To again quote Zito: “There’s . . . unlimited demand for secondary private equity but they are worried about private credit which finances 80% of those portfolios . . . I can’t compute, but I’m the dumb guy. I don’t understand. I start saying this and I get these blank stares back at me like OK, I don’t know.” This is a particularly acute concern for the broader US economy given the PE creep into small businesses over the past decade (chart below).

Learn more about Sage Road Research: sageroadresearch.com. Interested in subscribing? Message me.

WSJ interview with Zito: wsj.com/finance/invest…

Chart source: bloomberg.com/news/articles/…

English

cattlecapital retweetledi

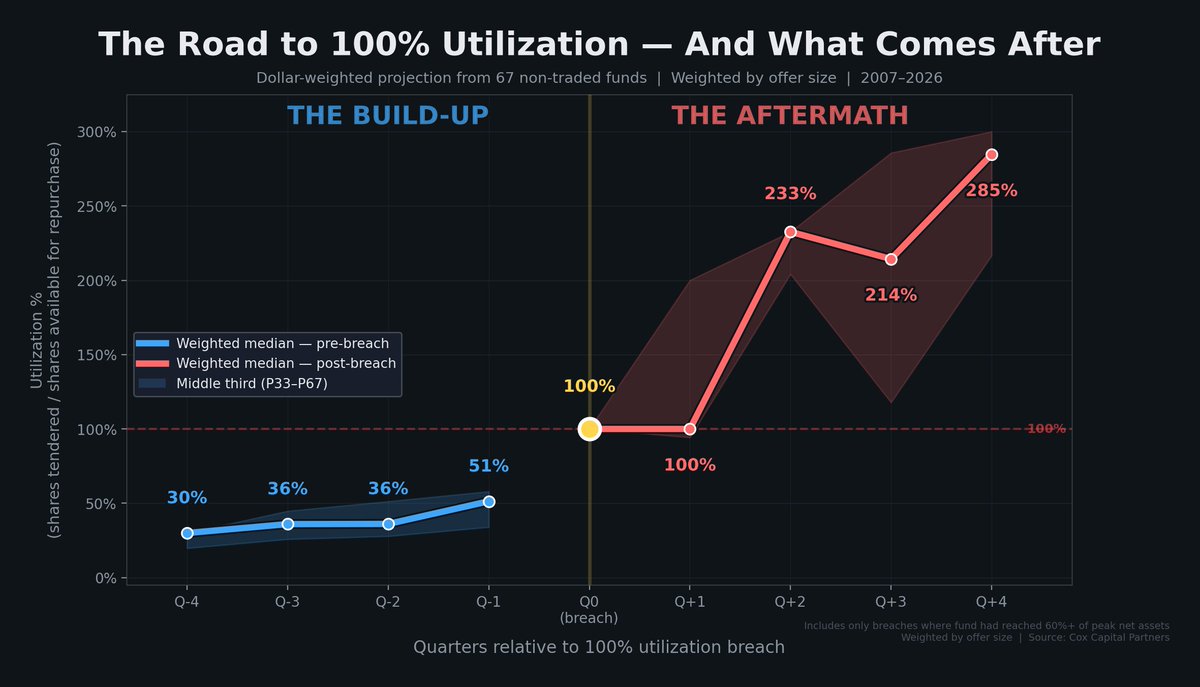

"Gradually, and then suddenly."

Continued growth is critical for #semiliquid funds working through redemption backlogs. When growth stalls, the math turns against you fast.

When semi-liquid funds hit 100% utilization after exceeding 60% of their peak net assets (after fundraising has leveled off) 70% never stop prorating.

This chart shows dollar-weighted results across all semi-liquid fund structures we track, representing how the largest funds behave before and after proration.

Interestingly, holding the line at Q+1 by creating additional capacity (expanding offers from 5% to 7%, etc.) is rarely rewarded.

#intervalfund #nontraded #privatecredit

English

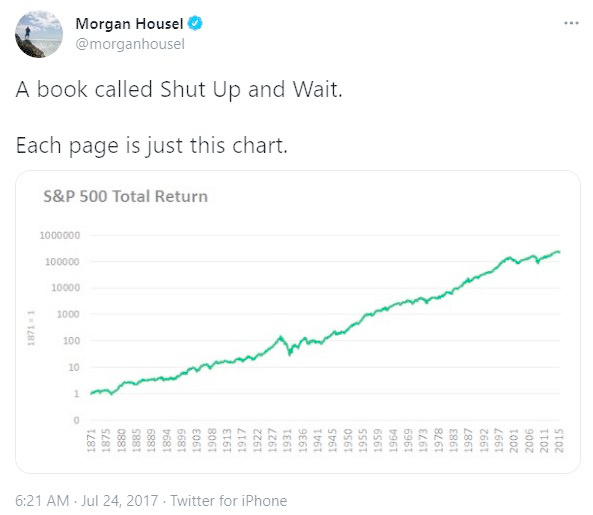

cattlecapital retweetledi

10 Tweets that will change your life forever

1. Shut up and wait:

English

I'm thinking about getting two dogs. What breeds should I consider?

English

@mark_slapinski Power has to be shown sometimes or people forget

English

Serious question:

Why is America at war with Iran?

I still haven't received a coherent answer.

English

BREAKING: Iran announces their requirements for a potential ceasefire with the US and Israel.

Requirements include:

1. “Recognizing Iran’s legitimate rights”

2. “Iran receives a payment of reparations”

3. “Firm international guarantees against future aggression”

English

cattlecapital retweetledi

After hundreds of conversations with financial advisors, one frustration comes up again and again:

Top performers being treated and compensated the same as average performers.

The advisors bringing in the most revenue.

Driving the strongest client relationships.

Growing the fastest.

They’re often rewarded with the same payout grids, the same recognition, and the same support structure as everyone else.

And eventually, one of two things happens:

1. They disengage.

2. Or they leave.

English

I’m refusing to believe that AI is taking my job as a financial advisor until the 401(k) rollover process is streamlined.

English