Sabitlenmiş Tweet

Capital discipline in the Canadian Oil & Gas industry? Let’s find out. A thread.

English

Canadian Energy Analysis

4.8K posts

@CdnEngyAnalysis

Canadian Energy. Former sell side scrub, IR punching bag, corporate schmuck.

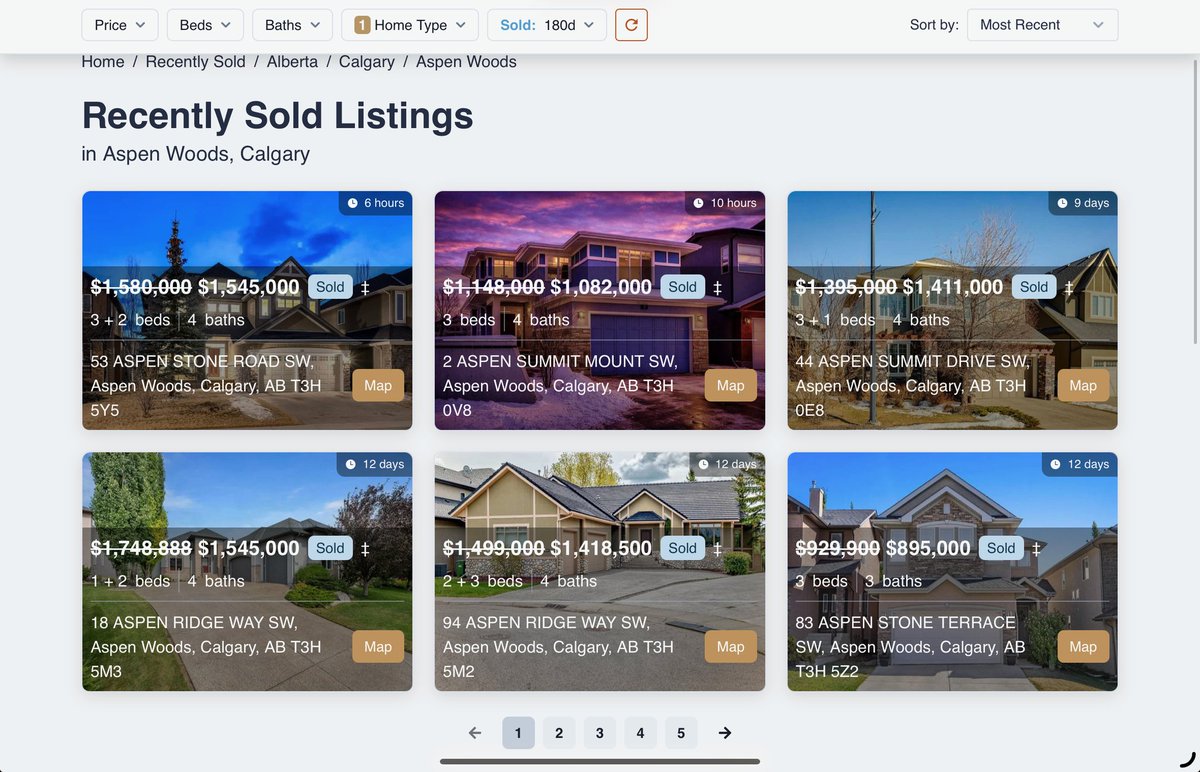

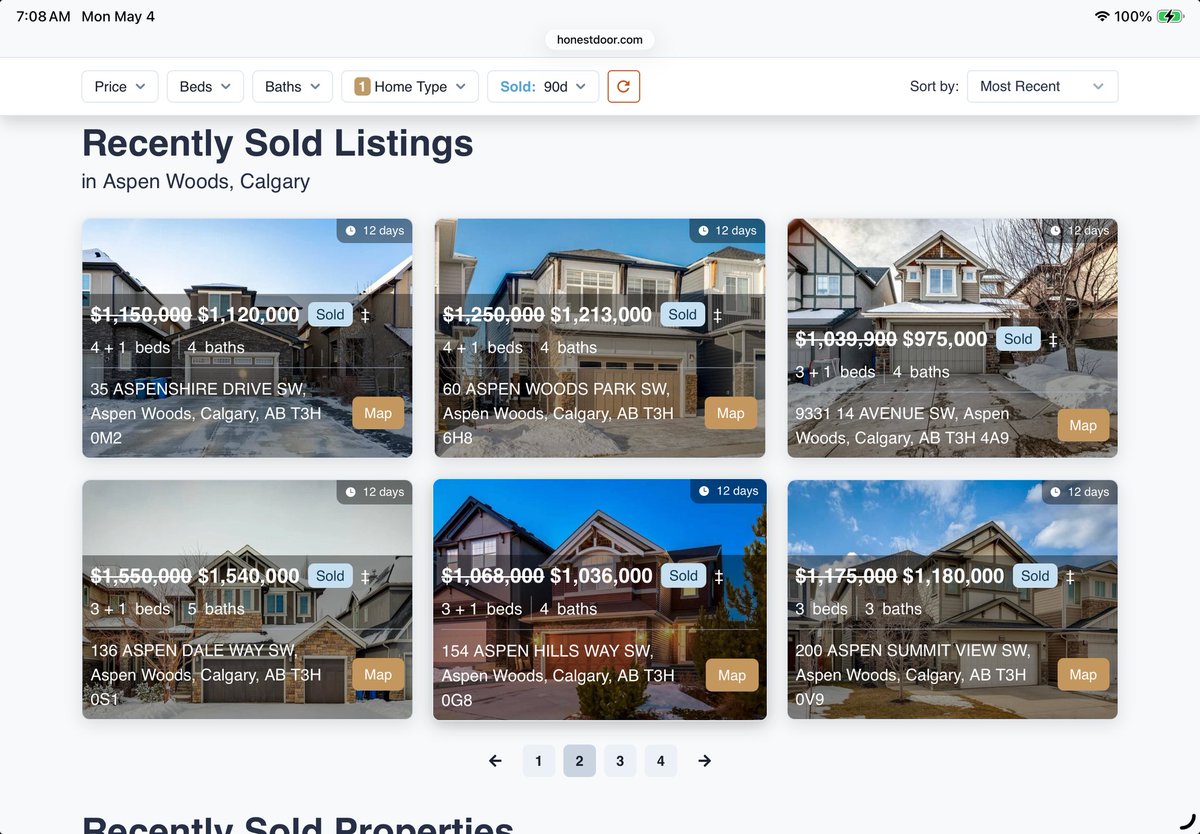

Calgary single family housing market on fire. Multiple offers, gone in hours if priced fairly. Know someone sold $2mm house with multiple offers within hours. Amazing. $100 oil?

O&G E&P's still look cheap E&P Vs. S&P Multiple