Duck Hunter

120 posts

@Coffffee2020 That’s almost 1,600 beds or 600mm would pay off there 10.5% mezz debt save them 70mm a year in interest

English

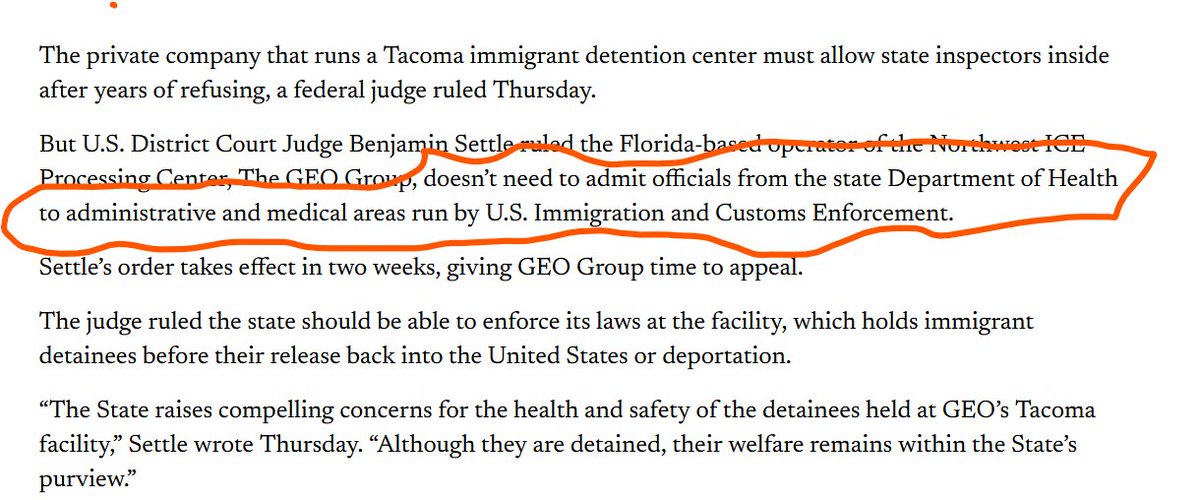

$GEO Appeal deadline next Friday, the 23rd. If ninth circuit doesn’t grant a stay, Washington State health inspections begin which will lead to the northwest ice processing center being shut down. DHS can’t allow it.

Duck Hunter@Coffffee2020

$GEO Is this the next site to sell? washingtonstatestandard.com/2026/07/09/wa-…

English

$GEO Trump over rules dhs hold on traffic stops.

foxnews.com/politics/trump…

English

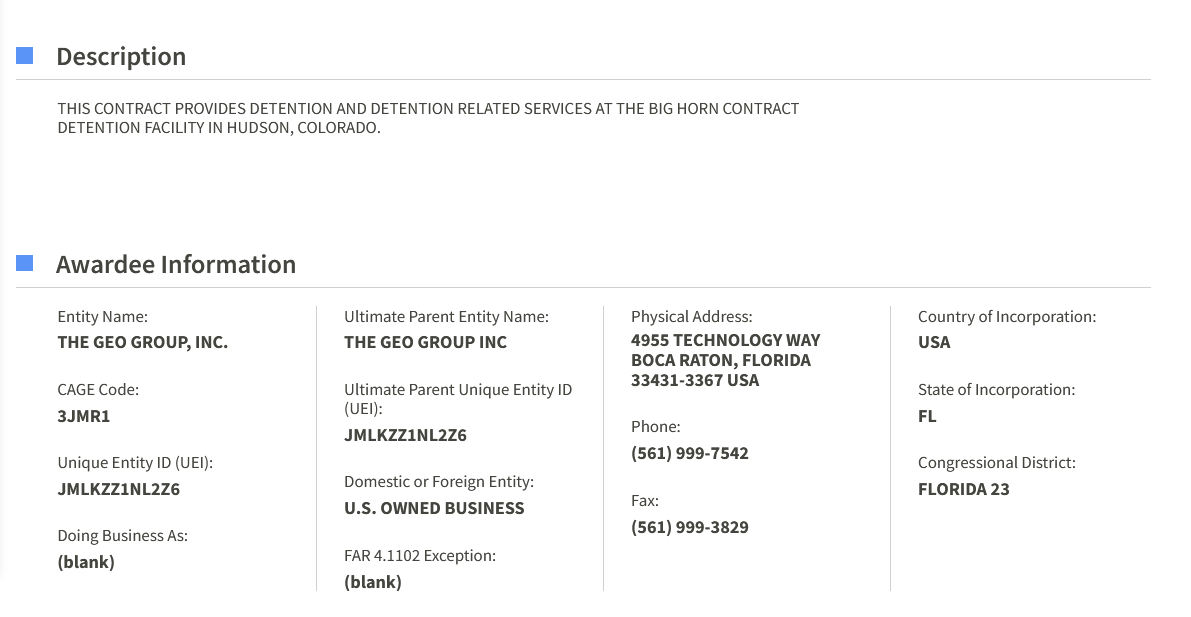

@Buffaloofnorth This contract is to fund the reopening of the detention center in Hudson Colorado. I assume that they will discuss this on the earnings call.

English

$GEO Your forecast of 8-900K ISAP could happen soon if DOJ loses their appeal in the Supreme Court. Almost seems like they are acknowledging as much with the losses in immigration court. Long Read.

politico.com/news/2026/07/0…

Tulip Critique@TulipCritique

@Market_Sherpa $GEO free cash flow story is underappreciated. I forecast $376m FCF in FY26, $463m in FY27, & $955m b/w FY25-27 (3yrs), based on 800k & 900k ISAP participation, respectively.

English

$GEO George never impressed me in the earnings call, but I believe you are right. He should be highly motivated to sell everything he can at those elevated prices. These opportunities don't come around very often in the detention RE sector.

BDC@BlueDuckCap

I believe that's exactly what they will do. Note that George Zoley founded the company in 1984. He owns over 4mn shares personally and likely more via other entities. He wanted to retire from the CEO role and did so in 2021 after being CEO for 27 years. Then he was called back as CEO in March. He'e been dragged before congress to testify re ICE and other political stuff. He is endured countless hit pieces from the media. He's 76. He has 2.5 more years of a friendly executive branch. If you were him, would you juice it now as much as you can? I would.

English

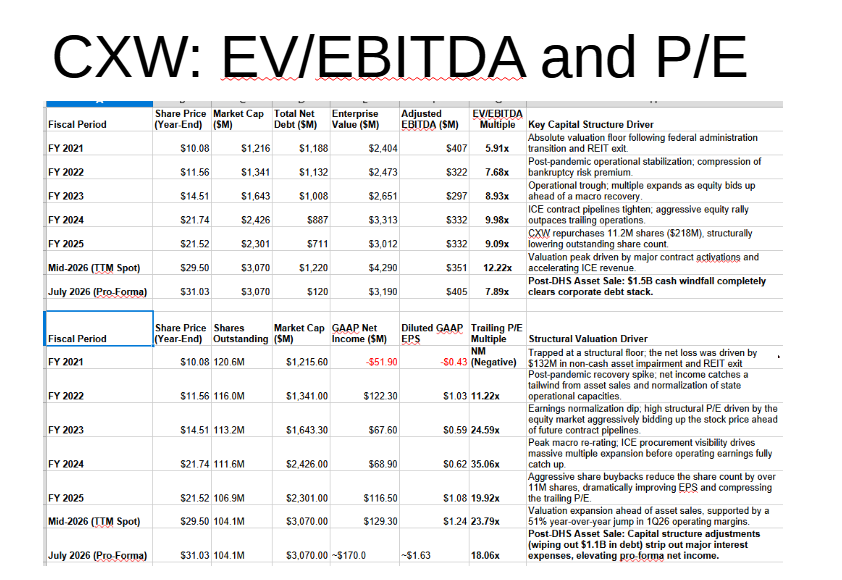

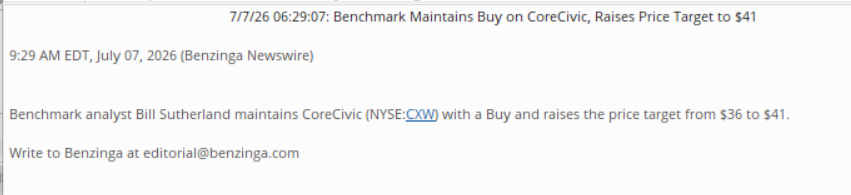

$GEO $CXW Even with the sales baked in, the valuations still lag! Makes no sense.

Cemini23@Cemini23

We got the CoreCivic sale right. We got the pop wrong. New Article: what we missed on the tape, and how I am reading $CXW $GEO $TH for the next six months. outlierweekly.substack.com/p/corecivic-so…

English

@TulipCritique With respect, I think your decimal is off by a factor of 10...

English

DHS is still looking to purchase an additional 8 properties after y’day’s $CXW announcement selling 2 to DHS for $1.5b or $323k per bed. Assuming 1.2k beds per $GEO US Services facility @ $323k that’s a potential $3.1b in property sales - unlocks huge liquidity for deleveraging.

English

$GEO bears are you listening? With $625m unsecured debt & $80m cash skeptics will continue to spark the credit debate. The FCF story is STILL underappreciated. With FY’26 $550m adj EBITDA and a debt profile that will continue moving south, investment-grade territory in sight.

Tulip Critique@TulipCritique

@Market_Sherpa $GEO free cash flow story is underappreciated. I forecast $376m FCF in FY26, $463m in FY27, & $955m b/w FY25-27 (3yrs), based on 800k & 900k ISAP participation, respectively.

English

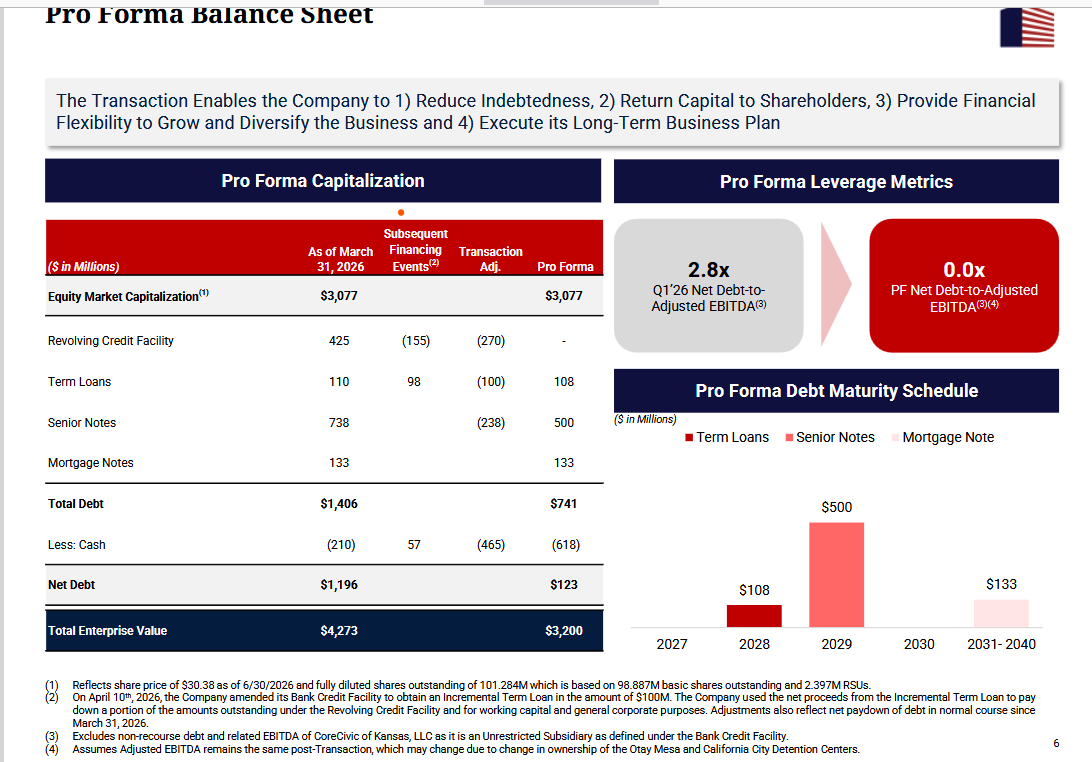

$GEO $CXW full slide deck can be found here.

ir.corecivic.com/events-and-pre…

Duck Hunter@Coffffee2020

$GEO $CXW I think this is a better slide

English

@Buffaloofnorth slide down to the presentations section

ir.corecivic.com/events-and-pre…

English

@Coffffee2020 where did you get the presentation from?

English

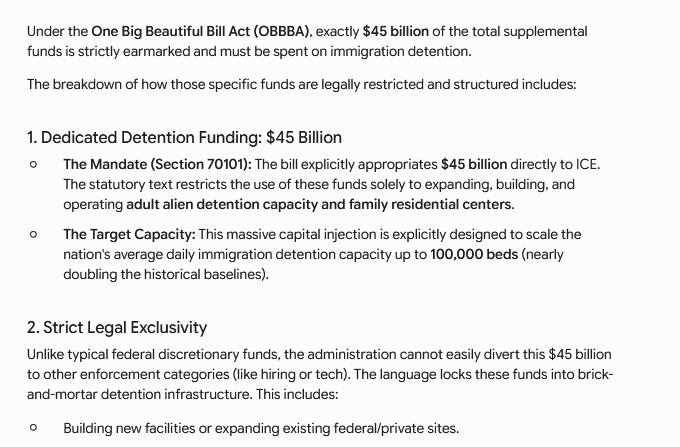

$Geo $CXW OBBB funds have to be spent by Sept 30, 2029.

Duck Hunter@Coffffee2020

$GEO facility sales while keeping the management contracts is accretive to earnings for debt over 10%.

English

$GEO facility sales while keeping the management contracts is accretive to earnings for debt over 10%.

Duck Hunter@Coffffee2020

@BoxLongs below is an estimate of the actual effect on GEO's profit and cash flow. We can argue about the assumptions, but if they use proceeds to pay down debt, then as you can see, it is a win win for GEO. This story needs to get told!

English

$GEO $CXW So, CXW nets $11.5 per share cash, keeps the management contracts and the stock is basically flat. $11.5 per share! Can still buy calls. They have $38B that has to be spent or they lose it.

Cemini23@Cemini23

CoreCivic sold California City + Otay Mesa to DHS for $1.5B. Closed July 2. The turnkey thesis was not a Reddit hallucination. Full map: why CXW vindicates the trade, what happens to ~$1.1B net cash, and why $GEO is still the chase leg

English

CoreCivic sold California City + Otay Mesa to DHS for $1.5B. Closed July 2. The turnkey thesis was not a Reddit hallucination.

Full map: why CXW vindicates the trade, what happens to ~$1.1B net cash, and why $GEO is still the chase leg

Cemini23@Cemini23

English