Dchammer

22 posts

.@Metaplanet friends, it's time.

• Mar 31: 107M shares issued (9.4% of OS).

• Apr 1: 1M MSW units allotted (~8.6% of OS). Initial exercise floor of ¥298; adjusts from Apr 17.

• Apr 1: 1.07M FSW units allotted (9.4% of OS). Currently underwater.

EVO shorting + market front-running = shares down 22% in two weeks.

Good luck, to all those brave (or numb) enough to hold through this.

Abbreviations:

• OS = outstanding shares

• MSW = moving strike warrant

• FSW = fixed strike warrant

The Ni (f. Obsequious Knight of the Realm of ...)@NitherDither

.@Metaplanet announced that they will be raising an impressive ~$765M through a combination of shares, MSWs and regular warrants. This will add ~10K #Bitcoin to their current stash of ~35K. Also impressive. Unfortunately, it's not so great for current shareholders. These transactions will likely depress share price in the medium term, keeping it glued to mNav of 1, if not dipping lower. It makes sense to me to sell now, and buy back once all this issuance is behind us. Here are my reasons: 1⃣ The dilution is a significant ~27%. 9.40% from the new shares, and 9.40% from the warrants, and 8.57% from the MSWs. A total of 314,736,000 shares on top of the existing 1,166,803,340. [1, 2] 2⃣ Traders and shorts will front run this dilution. This will likely cause price to drop even before the shares and warrants are issued on Apr 1. (Great choice of date, btw.) 3⃣ EVO Fund has no chill. A mNav floor of 1.01 simply means they will sell as soon as mNav is over that threshold. With mNav pretty much there already, it will take a while for them to go through their 1M units equivalent to 100M shares. 4⃣ The MSW exercise price floor is 187 yen. That's ~50% lower from here. $3350 has never failed to hit these MSW floors yet. 5⃣ When the fixed-strike warrants are exercised, they will very likely not be accretive, as price would have to be higher than 410 yen at that time, reflecting the Nav of the underlying Bitcoin. 6⃣ Acquiring BTC near an mNav of 1 does shareholders no good. As far as bitcoin-per-share is concerned, it's like the purchases never happened. Recall how we already did this with the international offering last year - yield was a minimal 3% even though a +56% increase in its BTC holdings, as deal terms increase shares outstanding by 51%. [3] I can see similar paltry returns from these transactions. And on a somewhat petty note.. it does annoy me that the same participants who contributed to price tanking during the IO through delta hedging are now getting another sweetheart deal of buying 2-year 410 yen LEAPs (soft callable after 1 year if shares trade at a 40%+ premium) for 4.10 yen only! I understand they are underwater, but so are shareholders. In fact, more so. Any shareholder would likely "bite the arm off" if they were offered a similar deal. The long and short of it is this: 🔴 It looks like price will remain glued to an mNav of 1 for the foreseeable future. 🔴 As long as that is the case, Metaplanet is not providing leveraged exposure to BTC. 🔴 If it is not providing leveraged exposure, there isn't much point in holding it until it does so again. Who knows, maybe we get our deal at a < 187 yen price point too. For reference, closing price on Mar 16, 2026: • $3350: ¥391 • $MTPLF: $2.39 • $MPJPY: $2.34 [1] contents.xj-storage.jp/xcontents/3350… [2] contents.xj-storage.jp/xcontents/3350… [3] x.com/NitherDither/s…

English

@BitcoinNews @Metaplanet @DylanLeClair @_dsencil @BitcoinJP_ he forgot to add a majority of their shareholders are down 80% at the expense of this

English

Director of Bitcoin Strategy at @Metaplanet, @DylanLeClair says their Bitcoin-per-share is up 5,000% since adoption — making them Japan's best-performing public equity. @_dsencil @BitcoinJP_

English

If Metaplanet breaks below this, there is basically no support area left until $0,70… kinda scary.

$MPJPY $MTPLF

₿ANE@matyr3al

Bearish possibility case for $MPJPY / $MTPLF

English

@DylanLeClair @Groenschoen I mean even Capital Group is trimming…they should know more than the rest.

English

@Groenschoen Just pointing out the facts, not bragging.

People playing gotcha to judge the business results based on a snapshot while our game plan has been consistent and unwavering for 24 months straight.

English

Metaplanet is the #1 performer out of 4,000+ publicly listed companies in Japan since adopting BTC in April of 2024. So yes, #winning.

§tack-O-§ats ∞/21м@SnarkyAlien

@basedlayer So this is what winning looks like…

English

Buying a Bitcoin Treasury Co like Strategy or Metaplanet without having complete conviction in Bitcoin itself is the reason why you're capitulating.

You should sell your positions if you do not think Bitcoin is going to $1mil by 2035.

I thought this was obvious.

Clearly not.

English

@ActuallyClimber @E055Michel1842 @ZynxBTC @BrianTGoodman What happens if you expand the time horizon to two years, do you think MP will be up again just by btc value being up?

English

@E055Michel1842 @ZynxBTC @BrianTGoodman When stocks do nothing but drop for months, there will likely be lots of selling pressure on any upswing. I think the longer we stay around 1 mNAV the more it solidifies the low mNAV narrative.

English

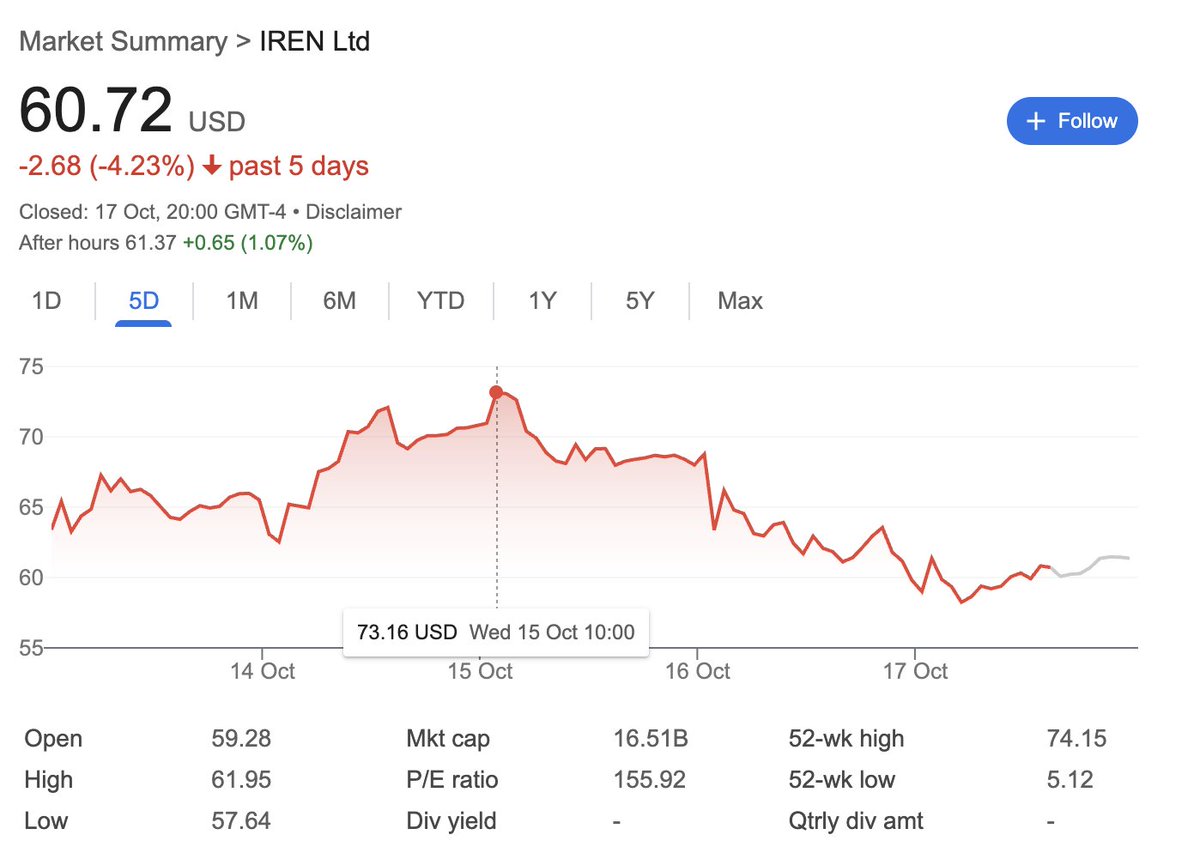

Some people sold their MSTR and Metaplanet to rotate into IREN and other Bitcoin miners this week.

IREN is up 10x over the last 6 months.

Selling the Bitcoin Treasuries at their lows to buy a stock that has run up so much like this is literally selling low and buying high.

Hope it works out.

English

In just a few short months, how many analysts have completely pivoted from their previously strong convictions?

Nobody can predict the future, including me.

This is why I no longer make price predictions, it's a fool's errand.

It's better to make directional bets and forecasts with a lower time preference.

I wasn't expecting such a severe correction for the Bitcoin Treasuries, but I certainly was prepared to hold my positions to 0.5 mNAV if need be.

Investing ≠ Trading.

What timeframes are people dealing with here?

Unless something fundamentally has changed, I see no reason to abandon the top Bitcoin Treasuries.

I believe in Bitcoin.

I believe in Bitcoin Credit.

Who's accumulating the most Bitcoin?

Strategy, Metaplanet and a few others.

Of course they have far more volatility than Bitcoin itself. That's the whole point.

I do agree most of the companies are not worth touching, but the aforementioned two are clearly going to be successful in my opinion.

We need to distinguish the premier ones from the rest somehow.

Anyway, I'm happy to be proven wrong, but we are no where near the point or time where the the thesis has been invalidated.

I'm more confident than ever in my positions.

English

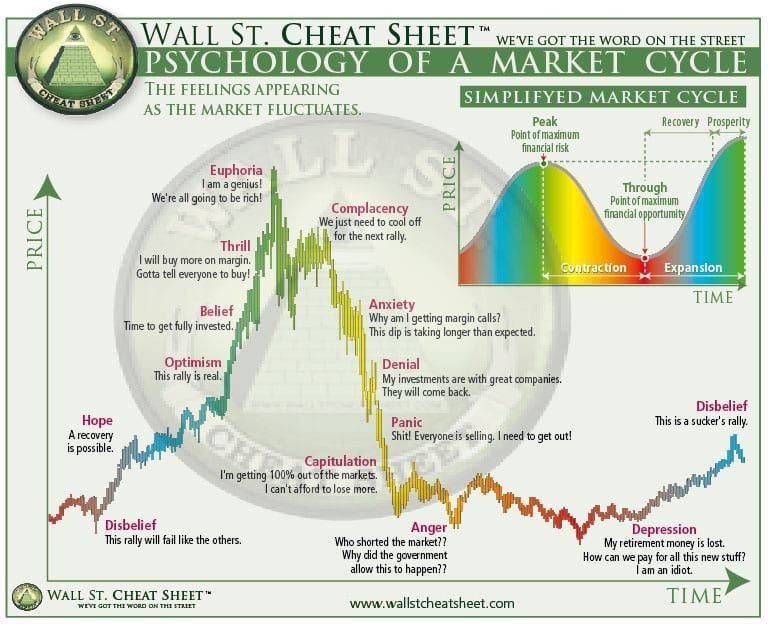

I’m going to tell you something NO KOLs or “market experts” will admit.

NONE of them knows where the markets are headed including me.

Here is the reality:

Macro peeps:

We all could do chart crimes and do correlations to suit our narrative.

I’m able to push out a bearish topping chart and also post bullish bottom chart

Fundamental peeps:

Why overvalued keeps staying overvalued?

TA peeps:

If you do trending strategies, this mean reverting environment will chop you dead. Vise versa.

Your indicator says bottom. But price drops further and your indicator repaints. Jokes on you.

For everything thing else peeps:

Cycles / Seasons / Liquidity whatever else, it works until it doesn’t. Remember that M2/BTC chart everyone sharing?Even its creator, Raoul Pal, just took profits.|

For the bears:

You can be bearish all you want. This is Trump era. It’s crime season. All you need is one move from Trump, like sell gold reserves for BTC. We will instant see $1M BTC. Always be invested a portion no matter how bearish you are. Keep a moon bag.

My advise:

Develop market instinct. Build your own conviction. Control your own risk ( profit-taking and stop-loss!!) Find asymmetric opportunities.

That’s all you can do.

What’s my current positioning?

I mostly stabled my portfolio at the August top and have been slowly buying dips since I’m sitting on a lot of cash.

Most of my cash will be deployed In Q4 making one of the biggest trades I will take.

Couldn’t get allocation thru VCs, I’ll buy on the public markets.

Will talk about it more soon. This is the most obvious trade of a lifetime for me.

Invest safe my friends.

English

Gave you multiple warnings. Again who is 1st on X to warn you? ME

Aug 1st:

Who was the first on X to tell you rate cuts are bearish?

x.com/pakpakchicken/…

Who was the first to started scaling out at the very top? ME.

x.com/pakpakchicken/…

x.com/pakpakchicken/…

Who was the 1st to tell you to rotate out from $eth to $hype and $sol for outperformance? ME

x.com/pakpakchicken/…

Who was the first to tell you to rotate to out of $hype and $sol? ME

x.com/pakpakchicken/…

Sorry I didn’t have any “charts” “proof” “thesis”

All I had was a “bad feeling”

x.com/pakpakchicken/…

Cycle always repeat. Haters shit on me at the top.

Don’t fear the man who is always bullish

Don’t fear the man who is always bearish

Fear the man who is bullish at bottoms and bearish on top

Chicken Genius@pakpakchicken

You don't need to be 100% invested at all time. Zoom out. SP500, BTC, GOLD, REAL ESTATE. We went max long in 2022. Good enough. Also: Rotation working perfectly to $sol and $hype I'll take more off the table. Find me any KOLs that called for that rotation. At the same time called for eth bottom. My flow state is fking back. To all those shitting on me asking you to rotate from $eth, jokes on you. Suddenly quiet. Death threats gone. 🤡

English

Touching grass.

I hope all of you make plenty of $$$

Will be back if needed

Portfolio up multiple Xs this cycle. 2 cycles publicly. 1 top exit, 2nd yet to be determined. It’s enough for me. Will use the $$ to help others. Material goods mean nothing to me.

If there’s any opportunity i feel it’s worth the risk / reward. I’ll share. After all, men only need god candles. God speed.

English

@pakpakchicken Its all good man stop beating yourself up over it. Everyone following you knows your intentions. My thing is 3350, want to understand your thoughts on it and why its dipped again and again.

English

Still pretty bumped out about my recommendation on $sbet

At the end of the day, I want you guys to make $$.

Recommended shitbet from $24 all the way to $17. So average is about $20. Not too late to cut before becoming community member / bag holder.

Shitbet was the obvious choice if you are always in the trench. Those who gets it, get it.

From here, shitbet may bottom of course. Looking for next rotation.

Meanwhile if you are bullish $eth. Just buy eth. You want leverage, $bmnr.

English

@pakpakchicken You said the same about 3350, are you referring to this as well? Would be good to know your thoughts on this, thanks

English

facts: $sbet is a consistent underperformer vs $eth and $bmnr

I chose to recommend the wrong horse, that's on me. Or maybe some of you jinx followed me into this trade. Either that's still on me.

Have not taken any action. Still riding both. If I cut, I'll let you know

English

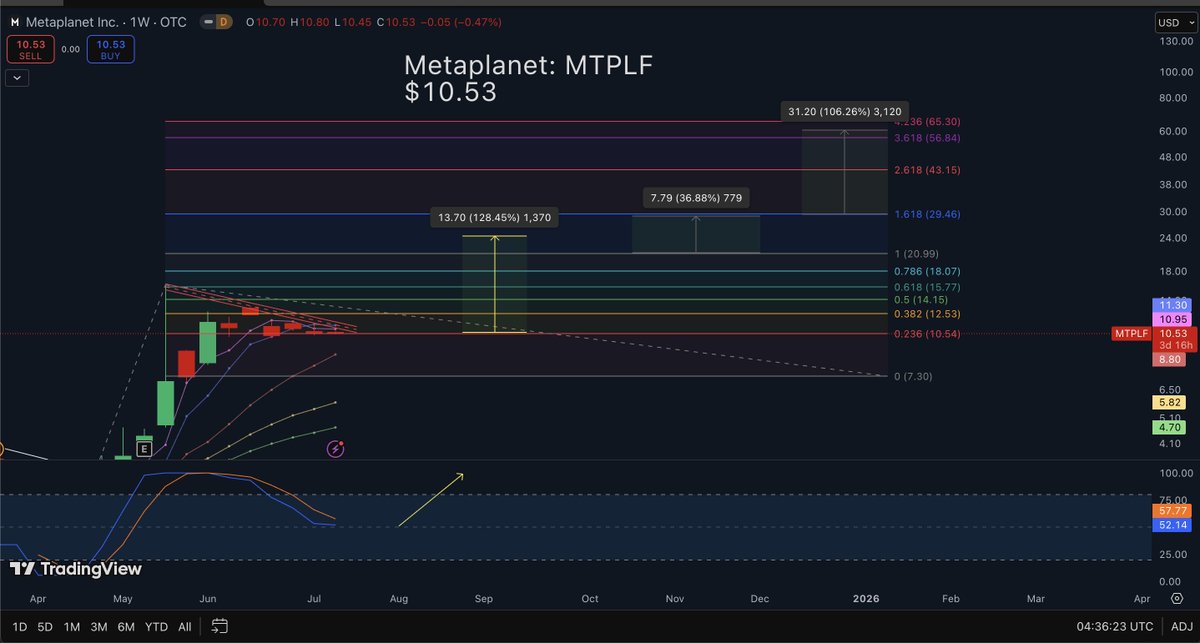

Metaplanet MTPLF $10.53

This looks like a bullish set-up

August and September should be interesting

English

@mc_khristina @mikesmlw What happens when btc drops in price though?!

English

$MTPLF one thing that experience has taught me is to never be afraid to ask questions (even ones you think you should really already know the answers to), so I asked ... If BTC starts to really take off, is that not necessarily good for $MTPLF because they haven't acquired enough Bitcoin yet at these somewhat lower Bitcoin prices? How should I be thinking about this? @ActuallyClimber was kind enough to educated me and said he thinks it's "EXTRA GOOD" for MetaPlanet.

1. There tends to be mNAV contraction when in a Bitcoin bear market, so the opposite is more likely in a bull. 2. Unlike $MSTR who doesn’t have enough volume to dilute shares very quickly (as a %), MetaPlanet has that in spades♠️ 3. How many Japanese investors are offsides and will want to hop in on Bitcoin when they see it being talked about, hitting new highs. Where can Japanese investors go -> MetaPlanet.

English

@pakpakchicken This is on the assumption that btc prices are kn the up, what happens when or if it goes down?

English

Doing TA on $MTPLF #メタプラネット 3350 is a sign of lesser intellect

Metaplanet's current BTC holdings 8888

CEO guidance 30,000 EOY 😂 FUD

My projection: 69,420 EOY

English

Dchammer retweetledi