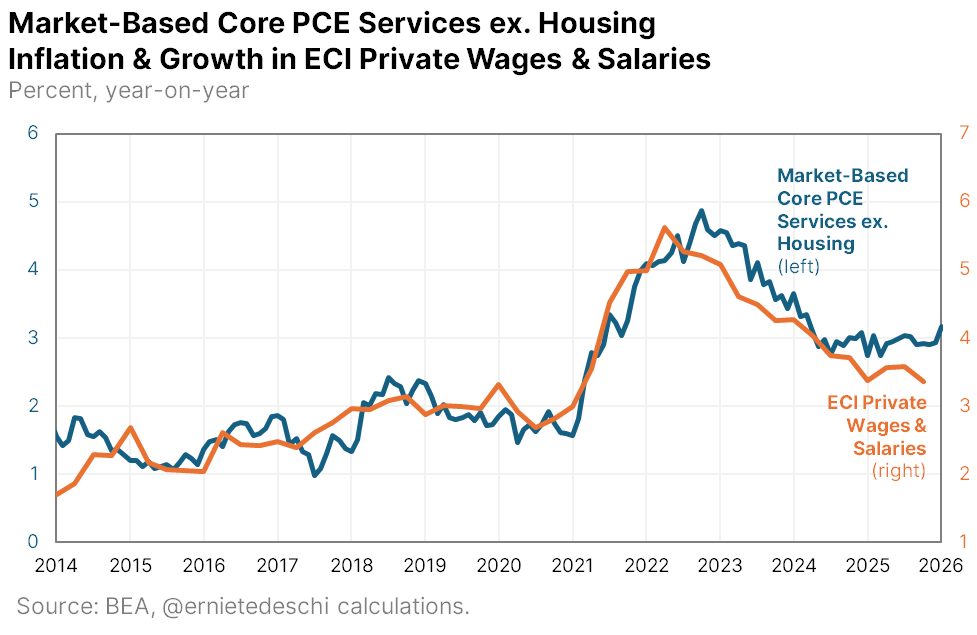

@ernietedeschi Chart that over the inverse of u3. Then make the time period 2022-2026

English

Delta North Macro

23 posts

@DeltaNorthMacro

Buy-Side Equity & Fixed Income Macro | Not Investment Advice

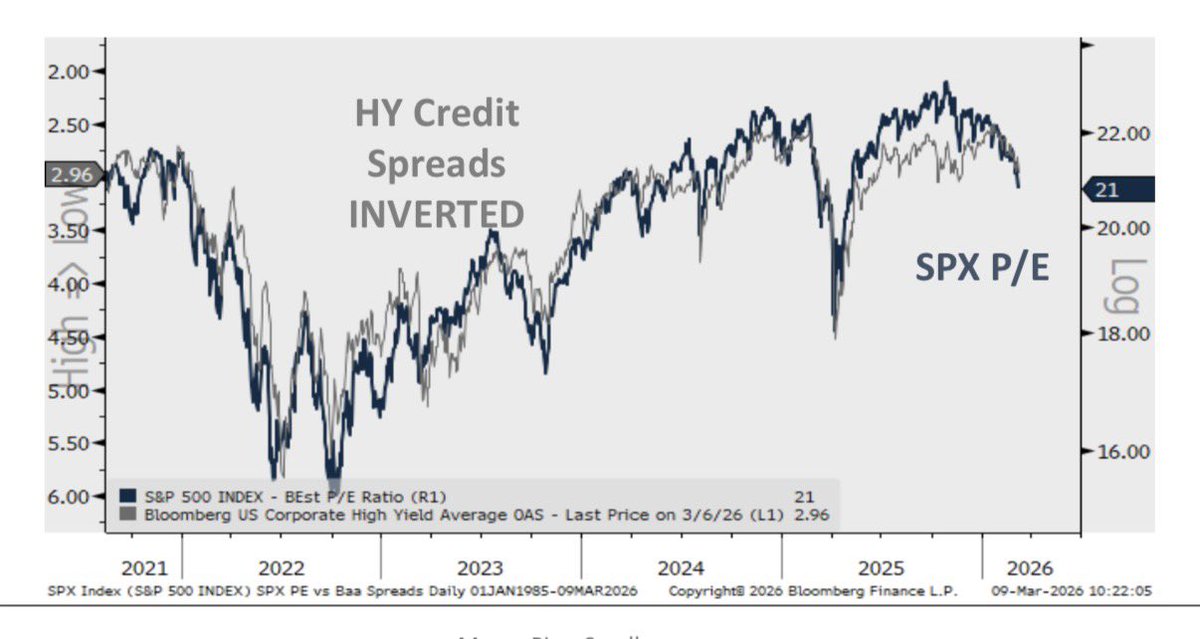

U.S. junk bond yields at the highest level of the year

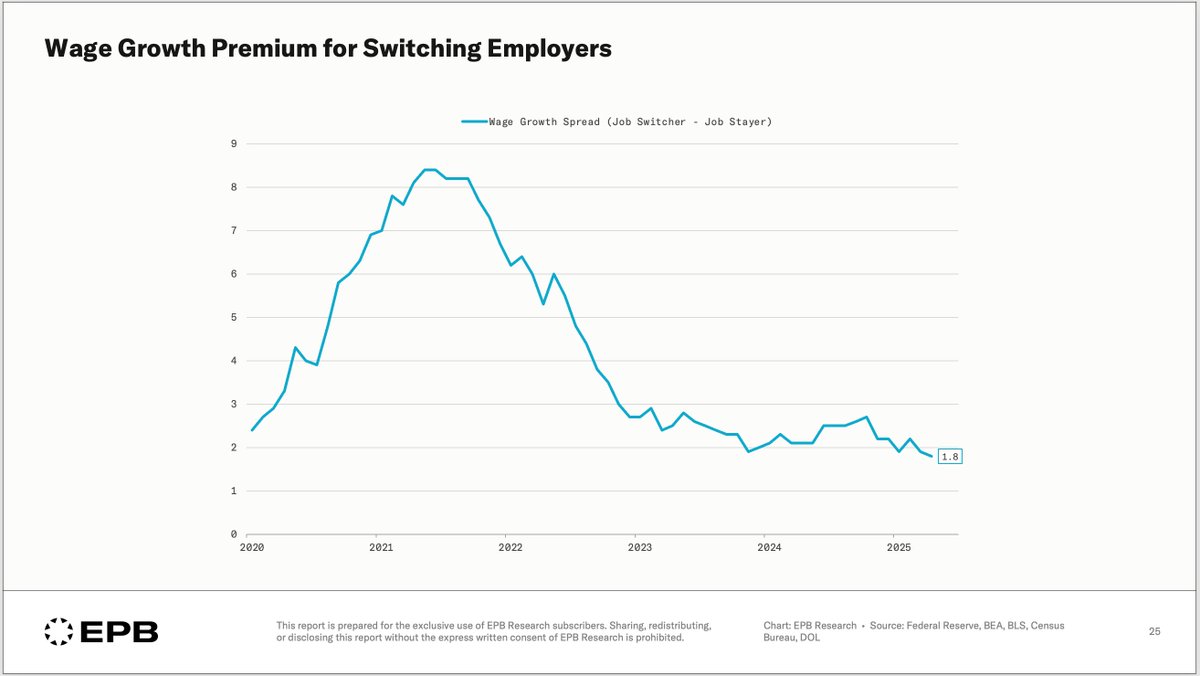

Joining @CNBC around 11am to discuss macro and markets, especially where employment and inflation data are heading as that's what's driving long, short and Fed policy rates.

@DiMartinoBooth Will cutting rates have much effect?