ShadowStock retweetledi

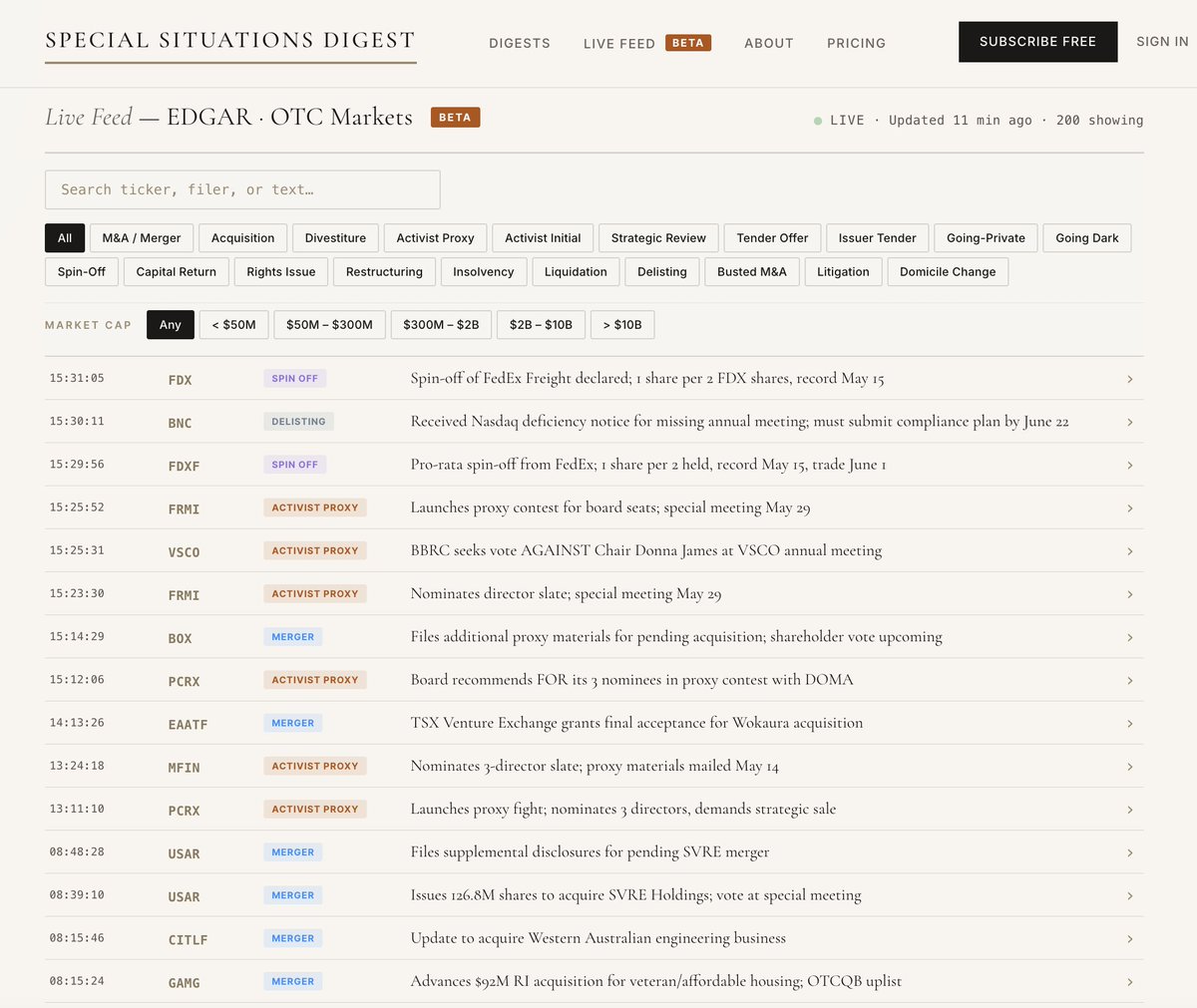

Created a live feed of US special situations (spin-offs, divestments, rights offerings, etc). Refreshed every 5 minutes.

Check it out! It's free!

English

ShadowStock

45.6K posts

@ExpectedValues

There are No Bad Assets, just Bad Prices: Exploiting Market Anomalies with Neglected Data

"I haven't seen a real new idea in trading in at least 15 years." Tom Costello (@tcoste110) ran money at Tudor, Moore Capital, and Caxton. Built one of the first NLP-driven equity systems in 2003. 20 years managing capital, never had a down year. "Comparing what a retail trader does to what a quantitative hedge fund does is like comparing driving a bus on the New Jersey Turnpike to winning a Formula One race." We cover: - His hot take: no genuinely new trading idea in 15 years — only better people doing the same things faster - Why everyone in quant finance is a genius — and why that makes you ordinary, not special - Crypto is "super smart guys cosplaying at finance" — built for retail, which is exactly why it's the easiest money in finance right now - Why AGI won't beat the hedge fund industry — all the readily-capturable alpha is already captured - The status trap: why the path that made Paul Tudor Jones a billionaire won't work for the kid trying to copy it in 2026 - His friend the investment banker who'd quit it all to run a 10-employee ambulance supply company worth $150M - Why excitement is "wildly overbid" in finance — and why wanting an exciting trading job is itself a disqualifier - The most honest end of the financial industry — and why the media has it exactly backwards Thanks so much to Tom for coming on Odds on Open! Highlights: 00:00 Intro 01:18 Building institutional credibility for early-stage managers 03:01 The Pareto distribution of hedge fund returns 04:25 Applying the Unified Field Theory of Finance to fair value 08:14 Trading against human incentives in a deterministic market 13:54 Why allocators don’t steal alpha from prospective PMs 25:16 Evaluating career edge in quantitative finance for 2026 30:48 Paul Tudor Jones and the art of game selection 33:42 Analyzing the economic viability of starting a new fund 35:16 Identifying common retail pitfalls: Mean reversion and arbitrage 38:55 Why there hasn't been a new trading idea in 15 years 50:33 Managing tail risk: Physics vs. deterministic financial distributions 59:10 Career pathing for PMs after a fund blow-up 1:07:53 SBF and FTX: Credibility vs. the "Founder-Genius" archetype 1:13:44 Establishing proof-of-concept through audited multi-year returns

David Siegel built a personal net worth of $8,000,000,000 without drawing a single support line on a chart. He realized decades ago that human intuition is flawed. His fund, Two Sigma, doesn't predict the future-they use Neural Networks to compute pure mathematical expectation across 10,000 live signals. Watch him explain why AI is eating Wall Street. Then read the exact framework his industry uses today below

This guy beat the market for 17 straight years trading a sector many investors have written off post-2008 Derek Pilecki (@gatorcapital) runs a financials-only fund. 21%+ annualized. His edge? A corner of the market many investors moved away from after the GFC. We cover: - Why he expanded from 25 → 40 positions and returns went UP - His counterintuitive rule: buy higher, not lower (positions get LESS risky as they rise) - The Robinhood call — bought late 2023, rode it to a multibagger - Why he's quietly watching FactSet, Morningstar & Verisk right now - His view on private credit risk (and why he disagrees with Jamie Dimon) - How he uses AI to analyze more stocks without losing his edge - Why markets chronically underreact to good news — and how to exploit it - The brutal career reality no one tells young PMs about Highlights: 00:00 Intro 01:06 Derek's +21% annualized return track record 02:50 Fundamental business change vs market noise in Robinhood 05:25 Portfolio construction: Concentration limits and adding to winners 09:09 Sourcing alpha and identifying three-year doubles in financials 12:44 Developing edge through repetition and management team cycles 14:16 Why the post-GFC regime fundamentally changed bank underwriting 17:07 Assessing tail risk and leverage in the private credit market 21:23 AI-driven market dispersion and identifying moaty businesses 24:11 Why shareholder base turnover matters for timing broken charts 29:37 Integrating AI into fundamental research and SEC filing analysis 35:39 Risk management: Permanent capital loss vs mark-to-market volatility 37:12 Capacity constraints: Optimizing for returns over AUM scale 50:39 Career risk and the reality of active money management

Every American should watch every second of this video. Thank you, @BenSasse.