Sabitlenmiş Tweet

F22

11.8K posts

$MU $SNDK $DRAM

@MicronCEO: AI is still in its "first innings" (very early stages). AI-driven demand for DRAM and NAND is projected to exceed 50% of the total industry TAM this year, with severe supply constraints persisting due to long lead times for new capacity

HBM (AI GPUs), DRAM (AI CPUs), and NAND are ALL in tight supply.

Memory is now a "strategic asset" for customers.

RE-RATE INCOMING

Trade Whisperer@TradexWhisperer

$MU I worked 21 years as an HBM, DRAM & NAND engineer. AMA is open. Ask me anything. I'll drop rare insights where I can.

English

$META and Zuck get no respect (relatively speaking).

Zuck is growing Meta faster than Google, Microsoft, Amazon and Apple and is more profitable than all of them on per $1 of revenue. But Wall Street is like "but Zuck wastes money on pet projects!" 🤣

ok, if that's your take, then imagine how badly he would be destroying everyone else if he didn't waste money. He's destroying everyone *despite* supposedly wasting money.

Stock Market Nerd@StockMarketNerd

There are people still doubting if $META can effectively use AI for its core business. Do they think Meta just magically snapped its fingers or accelerated from 16% to 32% growth by chance? Just listen to an earnings call. AI is dramatically helping their core. Right now.

English

$MU $DRAM $SNDK

It is time to have the most important debate of the entire AI market.

Is memory cyclical or permanently re-rated?

No hiding. Pick a side and defend it!

Best bull thesis and best bear thesis both get a public callout from me. Please keep it respectful 👇

English

You’re highlighting a key trend

AI customization and personalization.

This refers to tailoring AI models and outputs to individual users’ preferences, data, and needs…. think adaptive interfaces, user-specific recommendations, or fine-tuned responses based on past interactions.

Need more memory for this like 1 billion X

English

I’m coming to the conclusion that the biggest challenge for Enterprise AI, and AI in general , as of now, is that it’s still impossible to make sure that everyone gets the same answer to the same question, every time.

Which is a great response to the doomers. AI doesn’t know the consequences of its output.

Judgement and the ability to challenge AI output is becoming increasingly necessary, and valuable.

Which makes domain knowledge more valuable by the second.

Am I wrong ?

English

@JohnTinsman memory rerating will not happen over many years

it will only take a few quarters

$MU $SNDK $DRAM

English

ALL TIME HIGHS IN MEMORY PREMARKET

$MU up 3%

$SNDK up 3%

It seems like these names aren’t going to cool off until they get to a value where investors are no longer excited about them.

English

@FluentInFinance vehicle ownership will tank next

replace by autonomous ride hailing

English

The American Dream is disappearing.

First Squawk@FirstSquawk

RECORD NUMBER OF AMERICANS LEAVING US FOR BETTER QUALITY OF LIFE ABROAD: WSJ

English

@StockMKTNewz Google

Micron

NVIDIA

Meta

Broadcom

Amazon

Ge Vernova

Tsmc

Amd

Sandisk

Intc

English

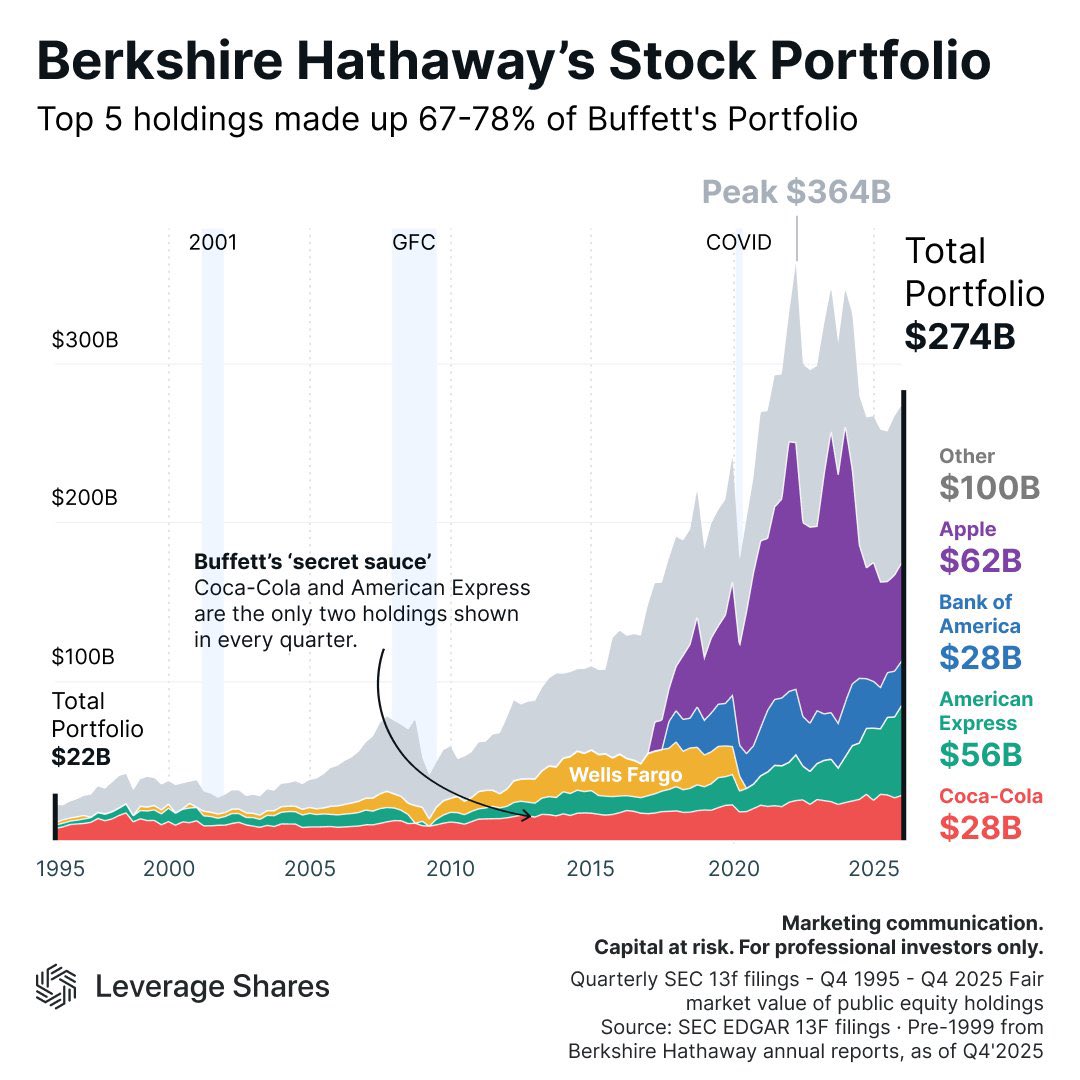

Warren Buffett and Berkshire Hathaway’s $BRK.B largest stock holdings visualized

Berkshire’s top 5 holdings currently make up ~70 of its total stock portfolio

Leverage Shares ETPs EU@LeverageShares

Buffett’s portfolio, visualized. Top 5 holdings drive the majority of Berkshire’s equity exposure with $AAPL leading, alongside long-time pillars $AXP and $KO. Concentration, patience, and conviction over decades.

English

@QC_Capitals Yes probably

Probability of $MU Stock split 2027 is high

NVIDIA did it at $1200 > $120

10 to 1

English

F22 retweetledi

5 Stocks that could make you Rich by 2030

1) AMD $AMD

2) Micron $MU

3) Taiwan Semi $TSM

4) NVIDIA $NVDA

5) Broadcom $AVGO

English

@realpristinecap Like selling Walmart and Costco Tsmc early. Brk.b underperform VOO in 1, 5, 10 year period.

English

The biggest signal of low IQ is someone who criticizes Warren Buffett’s investment decisions

English

@FluentInQuality He should invest in micron before it reaches multiple trillion dollars.

Memory (HBM) is the highest single component cost for Nvidia’s AI chips like the H100 (41%) and B200 (45%)

41% > 45% > higher prices

Please send this message to Jensen

Thx. 🙏

@nvidia @NVIDIAAI

English

Jensen Huang just admitted Nvidia made a mistake.

Not a small one.

Anthropic went to $GOOG and $AMZN AWS, not $NVDA, because Google and AWS wrote billion-dollar checks first.

Jensen's words: "We just weren't in a position to make the multi-billion dollar investment into Anthropic so that they could use our compute."

His admission: "That was my miss."

Without that early capital, Anthropic had no choice.

TPU and Trainium growth? Jensen says it plainly, it's 100% Anthropic. One customer. Not a trend.

Now, Nvidia is investing $30B in OpenAI and $10B in Anthropic.

The most profitable company in AI history, 70% gross margins, cranking out generational leaps every single year, was too small to write a $5B check when it mattered most.

They won the compute war. And still left the equity on the table.

Jensen isn't making that mistake again. Neither should you.

English

@wallstengine Amd will start gaining market share

The memory bandwidth is the key component to their success

Due to their best in class chiplet technology / architecture

English

HSBC Downgrades $AMD to Hold from Buy, P $340

Analyst comments: "We downgrade our rating to Hold as the stock has already significantly re-rated from trading at a 19x 2027E P/E multiple to a 33x P/E multiple, with limited room for earnings upside due to capacity constraints.

AMD's share price has gained 77% since the beginning of April, compared with the Nasdaq up 17% over the same period, on bullish server CPU demand expectations from agentic AI. However, we do not expect an upside earnings surprise from AMD's upcoming 1Q26 results despite strong demand, as ongoing foundry constraints will likely persist throughout 2026E.

We are lowering our 2026E AI GPU revenue estimate to $14.6B from $18.5B due to increasing supply chain uncertainty around the MI455 rack server ramp-up. While server CPU demand remains strong, AMD remains dependent on TSMC foundry capacity, limiting unit growth upside in 2026E. We see possible upside in 2027E, but this depends on better foundry capacity visibility emerging in 2H26E."

Analyst: Frank Lee

English

F22 retweetledi

The FED will be overhauled, printing will continue, and rates will be lowered.

Fred Krueger@dotkrueger

Warsh will be confirmed in 2 weeks. May the printing begin...

English

My Sunday not so hot takes:

$NVDA is still undervalued

$TSM is still undervalued

$AMAT is still undervalued

$MU is still undervalued

English