@aleabitoreddit Real choke point = higher-kV utility and transmission transformers

English

FadeTheNoise

728 posts

@FadingTheNoise

27. Engineer and long term investor. Tracking my wealth building journey and giving opinions. Current holdings: $SOFI $AMZN $ASML $MSCI $MSFT $FTNT $MA

Microsoft 365 connectors are now available on every Claude plan. Connect Outlook, OneDrive, and SharePoint to bring your email, docs, and files into the conversation. Get started here: claude.ai/customize/conn…

Big milestone — Robinhood Banking just crossed $1.5B in deposits from nearly 100K funded customers, and deposits are up ~50% in the past three weeks. The team is cooking 🔥 Robinhood is a financial technology company, not a bank. Banking services are provided by Coastal Community Bank, Member FDIC.

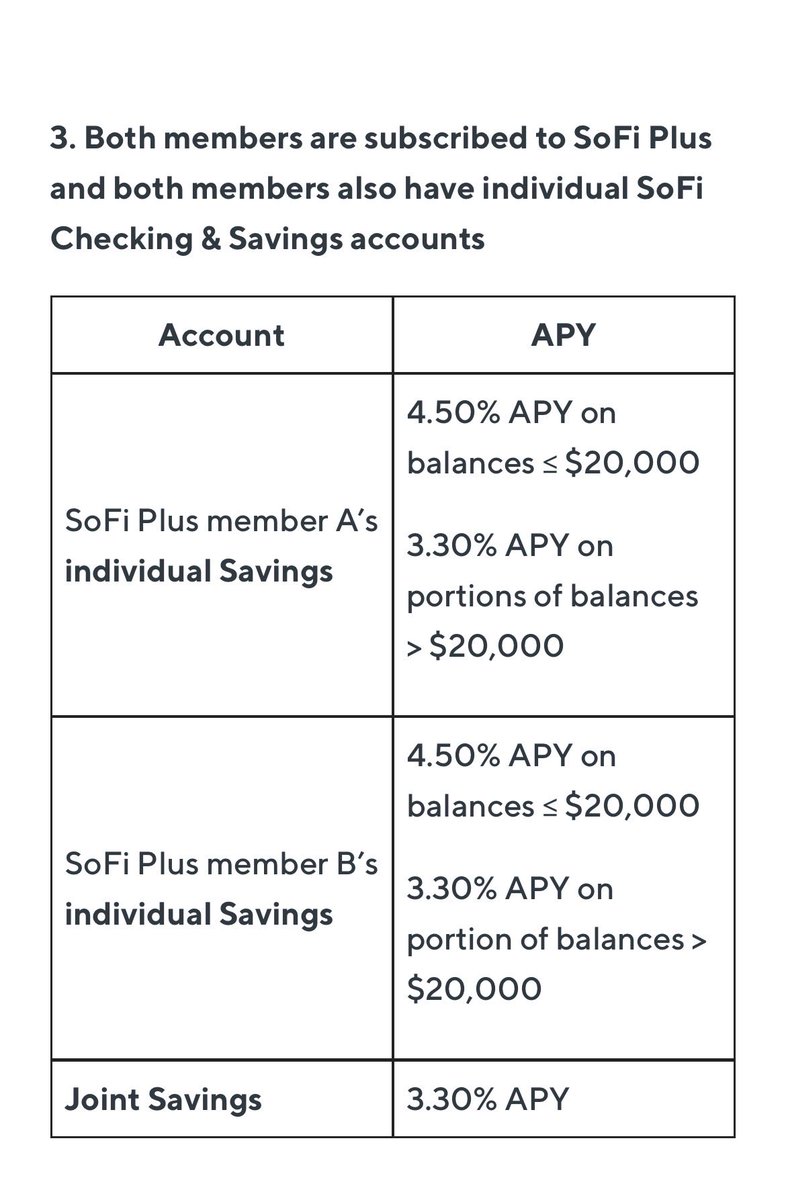

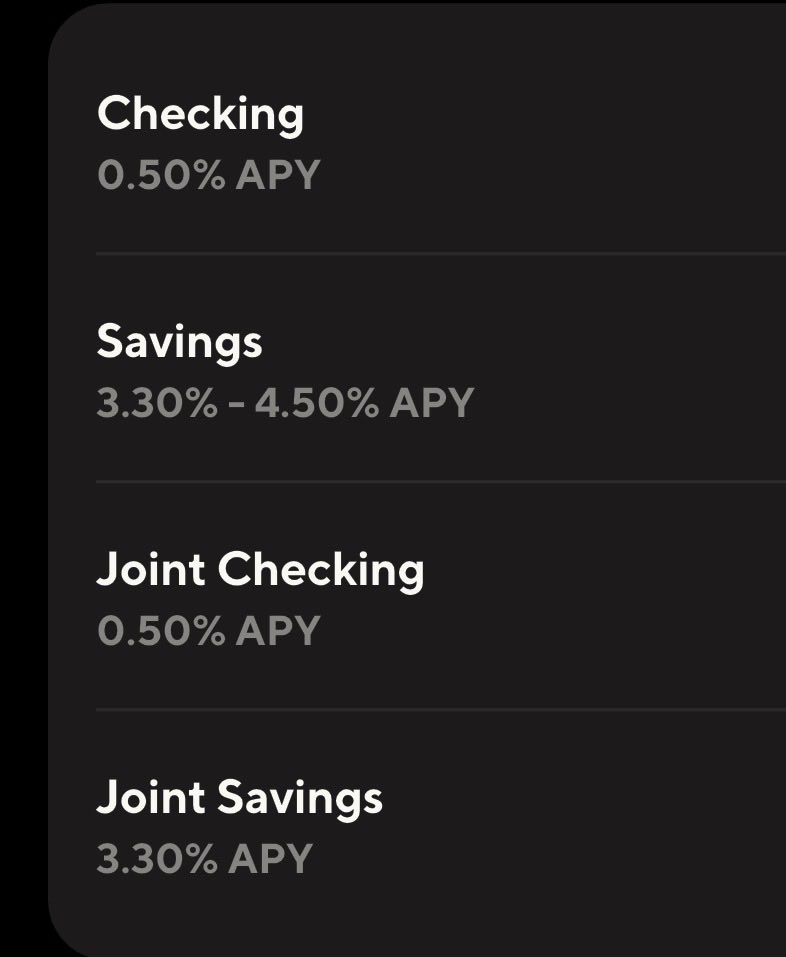

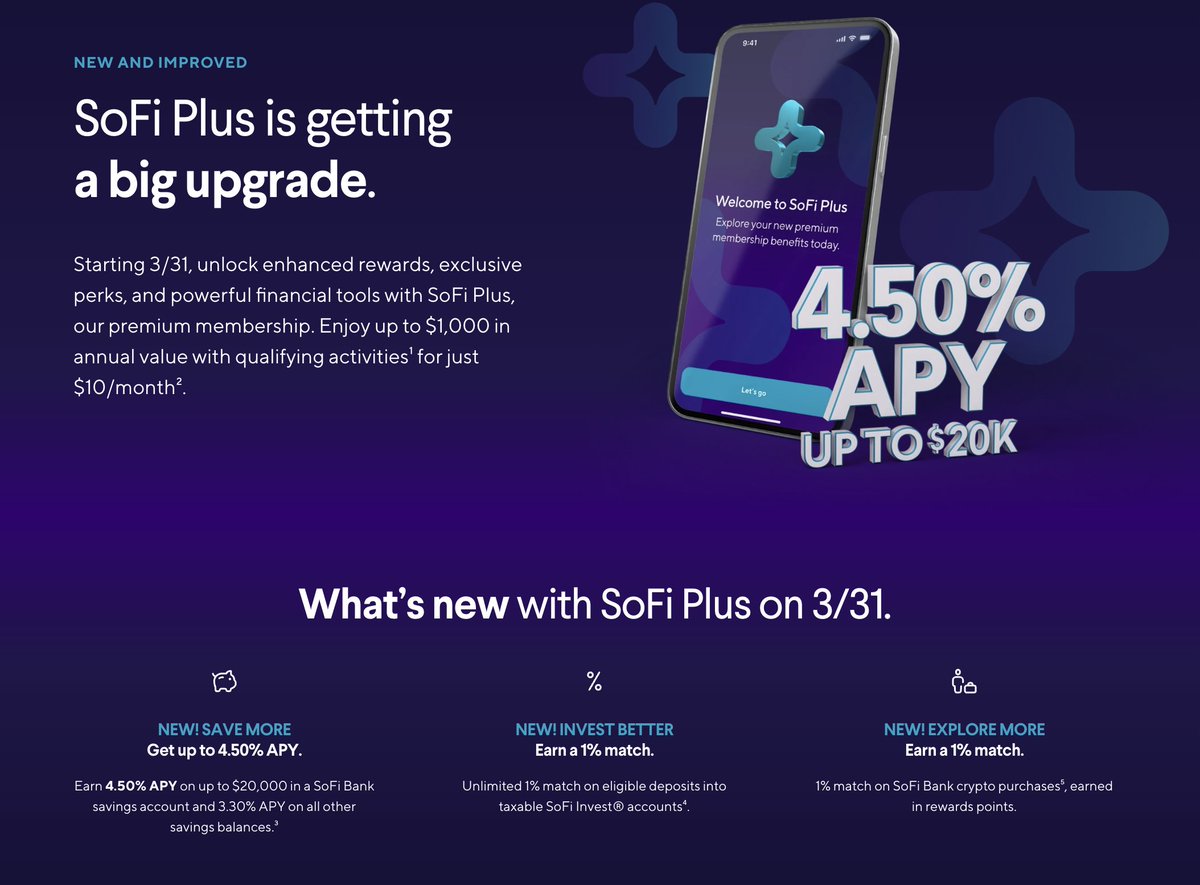

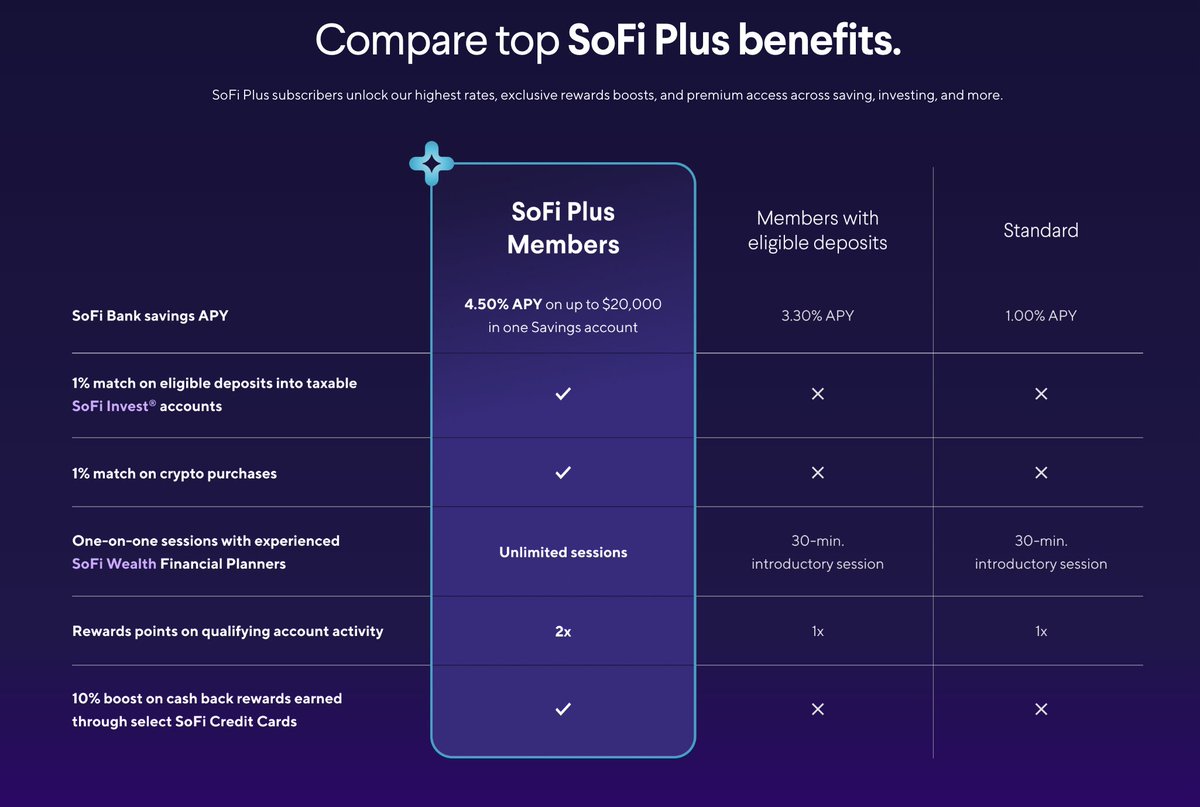

We didn’t just hear your feedback—we listened 🦻 Here are some great benefits that make SoFi Plus even better: NEW ➡️You can now earn 4.50% APY on up to $20,000 in a SoFi Bank savings account and 3.30% APY on all other savings balances.* If you max out the $20K, this could mean $900 in annual interest.** 🎉 NEW ➡️Unlimited 1% match on all eligible deposits into taxable SoFi Invest® accounts.^ NEW ➡️1% match on SoFi Bank crypto purchases, earned as rewards points.† Upgrade to SoFi Plus for $10/month‡ now ➡️ SoFi.com/SoFi-Plus/

Moved my retirement accounts to Robinhood last year bc of their asset match (like 3% match on all assets or something like that?) But it’s incredibly annoying that you have to scroll past prediction markets (read: sports betting) to see portfolio positions. The forced sports betting is gross.

*SOFTBANK CEO: OHIO DATA CENTER WILL BE $500 BILLION PROJECT uhm, is this a joke?

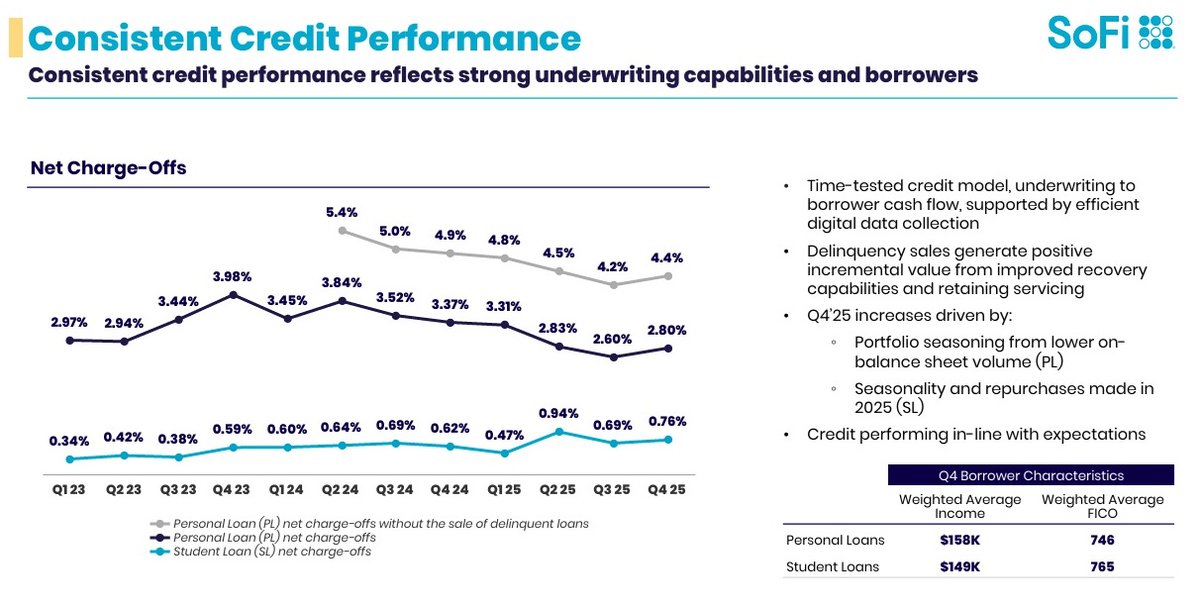

$SOFI The biggest problem that could come for Sofi isnt investors... its depositors. They have enough liquidity to weather some withdrawals, but not if there is a cascade. If depositors pull their money out of Sofi. They would be hit with a bank run. The Loans they have on the balance sheet would then have to be liquidated and Im not sure what they would be worth mark to market. Interesting development to say the least... At least Sofi has been smart enough to dilute shareholders at an attractive price and raise capital before something like this showed up. Though I doubt Sofi will be able to maintain a 45 PE ratio... when JP Morgan, a supestar, trades at 12-15 and the rest trade at 10. The biggest problem that I see in all of this is the accusation of manipulating charge offs via sale of loans and financing the buyers of those same loans... Havent read the Sofi reply yet but man this is getting interesting.

Muddy Waters vs. $SOFI Accusations Check - A Thread 🧵👇 1/ Accusation 1: Personal Loan Charge-Off Rate is Really ~6.1%, Not 2.89% MW's Claim: Muddy Waters asserts that SoFi manipulates its charge-off rate by disposing of loans just before they reach the charge-off threshold and by "parking" defaulted loans in unconsolidated entities. Why It's Misleading: - SoFi emphasized that it operates under strict regulatory oversight and adheres to established accounting standards, with financial disclosures prepared in accordance with U.S. GAAP and complying with SEC rules. Any loan sales or off-balance-sheet treatment would have to be disclosed and approved under these frameworks. - SoFi is regulated as a bank holding company supervised by the Federal Reserve and the OCC. Misrepresenting charge-off rates to these regulators, not just to public investors, would be an extraordinary and career-ending fraud, not a management bonus trick. - Selling loans before they charge off is a standard, entirely legal practice in consumer lending. It's not manipulation, it's portfolio management. The loans are sold at fair market value, and any gains/losses flow through the income statement. - Muddy Waters alleged the charge-off data contains a "mathematical impossibility," yet didn't account for how SoFi's loan vintage mix, rapid origination growth, and loan sale activity interact with the charge-off denominator, a common error in short-seller charge-off math. 👇