Sabitlenmiş Tweet

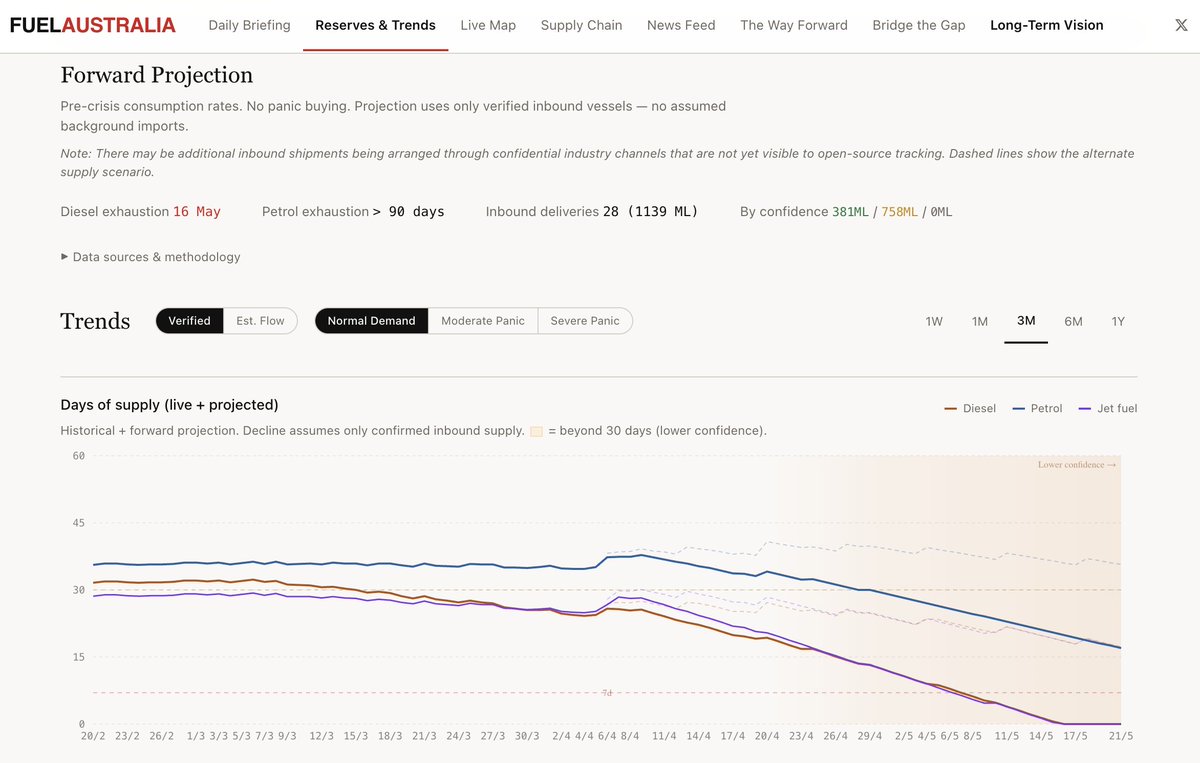

Australia is the largest importer of diesel fuel in the world. It also holds the lowest fuel reserves of any IEA member nation — dead last out of 28 developed economies. Japan stockpiles 260 days. We're at ~26 and falling.

Six of eight refineries have closed since 2013. We import over 90% of our refined fuel, mostly through a single chokepoint that's been closed for 37 days.

I built fuelaustralia.org to track what's actually happening — in real time, from primary sources:

— Live AIS tanker tracking (750+ vessels, 40+ confirmed inbound)

— Government reserve data direct from DCCEEW Power BI

— 90-day depletion projections with vessel delivery modelling

— Daily intelligence briefings synthesised from 80+ sources

— Cargo type inference, multi-source vessel fusion, confidence grading

— 28 evidence-backed policy solutions stress-tested against expert review

Every data point sourced. Every claim confidence-graded. Independent and non partisan.

Follow @FuelAustralia for daily briefings.

English