Gideon Malherbe

798 posts

Gideon Malherbe

@GideonM

Achieving Extraordinary Results with Clients worldwide through Scenario Planning, Technology Innovation, Digital Transformation, Executive Coaching and M&A.

New York, New York Katılım Mart 2008

1.7K Takip Edilen607 Takipçiler

Gideon Malherbe retweetledi

The best part about this is Tucker Carlson saying to the prankster, "We’ve done our best to verify that your identity is what you say it is. You’re not a fake [Alexei] Navalny or doing a prank." (They were doing a prank.)

Josh Pieters@joshua_pieters

We Pranked Tucker Carlson...

English

@ShivenChabria And you crafted this whole narrative all by yoursef - pretty impressive!

English

How to balance your company strategy with counter-intuitive shifts in the industry

linkedin.com/pulse/how-bala…

English

Philip Meyer presenting at Bank of America the award winning fintech decentralized card solution @Vaultavo the technology is amazing - master key wrapped in biometrics cryptographically imprinted on secure chip in card. NO Backdoor!

Manhattan, NY 🇺🇸 English

Gideon Malherbe retweetledi

A recap of our selection as a finalist for Accenture's #FILAP2023 program! Exciting times ahead! 🚀

#DigitalAssets #Blockchain #DeFi #Web3 #AsiaPacific #Fintech #Cryptocurrency #CryptoHub #Innovation #PrivateKeyManagement #BiometricSecurity

linkedin.com/pulse/vaultavo…

English

Gideon Malherbe retweetledi

Excited for @money2020 in Amsterdam from 6th-8th June? We certainly are! 💼 Our CCO, James Fick, will be there too. Give us a like if you'll be attending, and we'll keep an eye out for you! 👀 #Money2020 #Amsterdam #Fintech #DigitalAssetsCustody

English

Gideon Malherbe retweetledi

🚀Get to know our Co-Founder and CEO, Philip Meyer, as shares his take on Blockchain, DLT, Biometrics for Private Keys, and more in an exclusive interview with Global FinTech Series. Check it out now 👉 ow.ly/xxuv50Or3ps #Blockchain #DLT #Biometrics #FinTech

English

"Talent is rarely enough to assure victory and bad luck is rarely enough to guarantee defeat.

Do they influence the outcome? Of course. But your response will always sway the final tally."

– @JamesClear @Vaultavo

English

April’s crypto scams, exploits and hacks lead to $103M lost — CertiK cointelegraph.com/news/april-s-c… via @cointelegraph #vaultavo

English

Gideon Malherbe retweetledi

"With $3.5 billion of two‐year notes maturing today and $3.3 billion of bills maturing tomorrow, the Treasury faced the necessity of having to stop payment on checks already mailed to Social Security recipients and recipients of income tax refunds."

1979, not 2023.

nytimes.com/1979/04/03/arc…

English

Gideon Malherbe retweetledi

The pace of change in the payments industry is clearly accelerating. It's not a matter of 'if', but a matter of 'when' blockchain technology is adopted into mainstream finance accross the world - it's time to embrace and support this change!

finance.yahoo.com/news/apple-lau…

English

29 “5 Star” customers in line at Hertz Dallas - no cars??? Wtf!

English

English

@RaoulGMI I think any decentralized tech with long-term staying power will survive legal challenges, gravitate towards jurisdictions that are more open, and people will go through frictions to keep participating in it.

eg even if BTC is cut off from US banks, I doubt that's a kill shot.

English

@rafferty998 @KobeissiLetter Centralize and control to do what?

English

New Fed data shows banks lost ~$100 billion in deposits last week.

Here’s the breakdown:

1. Large U.S. Banks: +$67 billion

2. Small U.S. Banks: -$120 billion

3. Foreign-Related Banks: -$45 billion

Overall borrowing from banks is up a record $475 BILLION.

The worst part?

SVB is counted as a large bank in this calculation, and large banks still ADDED $67 billion.

Small banks are collapsing.

English

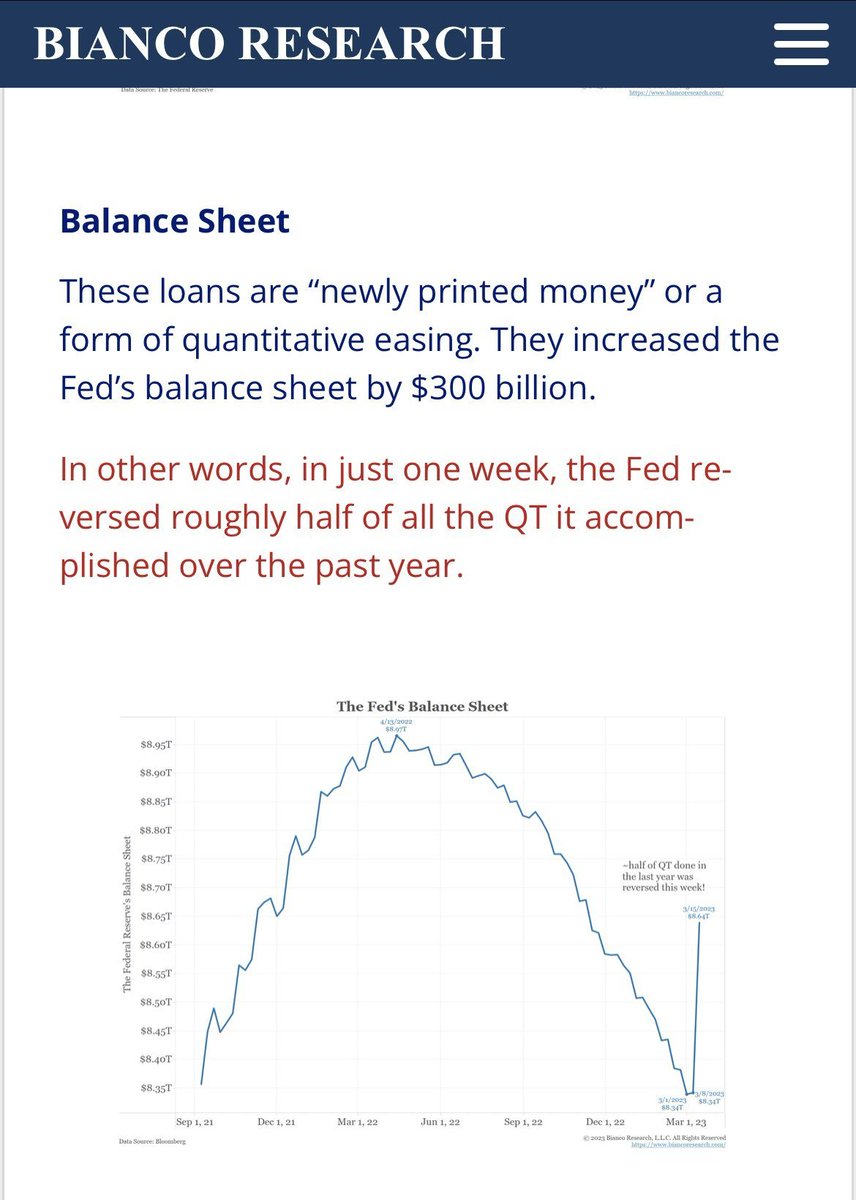

PRINT TRILLIONS WHILE HIKING RATES

The Fed now has “high rates” like SF has “low crime rates”. It says it does, but it doesn’t.

Because you have to be pretty naive to think today’s rate hike means the Fed is still “fighting inflation”. You can see it in the graphs — the printing is already vertical[1,2], and trillions in new money is available for both domestic[3,4] and foreign[5] banks. Yet the Fed continues hiking rates to fool low information voters into thinking the last two weeks were just an isolated series of multi-hundred-billion dollar bank failures, and that their policy is unchanged. Nothing to worry about, the Western banking system is resilient, and it’s normal to have banks die at the rate of five in ten days![10]

Because that’s actually all this state does: it fakes the rates.

Remember when SF claimed officially low crime rates[6] even as criminals robbed stores in broad daylight[7]? Remember when FDA prevented labs from testing so we all underestimated the COVID infection rate[8], till old people in New York started dropping dead? And remember when the Fed claimed the inflation rate wouldn't be a problem[9] before anyone buying groceries found out it was an emergency?

The American state fakes the rates.

And that’s what’s happening with today’s “hike”. After killing five of their own banks[10], catalyzing a series of bank runs[11], and realizing the public now knew they’d made hundreds more banks insolvent[12,13], the Fed rolled out programs over the last two weeks that broke the normal relationship between “hiking rates” and “tightening monetary policy”.

All the losses the Fed rate hikes cause for domestic banks?

They’re printing money to cover it.[14]

All the losses they cause for foreign banks?

Printing money to cover that too.[15]

And the losses they cause for depositors?

Naturally, more printed money![16]

So now the banks don’t publicly die from bank runs. Instead, even as this rate hike keeps pushing bank stocks further into the ground[17], and banks further into insolvency[18], the banks know they can just get more printed money (eg at the discount window[19] for BTFP) to cover their losses. That’s what BTFP, the swap lines, and the effective “FedDIC” policy mean: infinite money.

And this infinite money is no longer abstract. It’s printed dollars that individuals touch directly when they wire their money out of banks they fear may collapse, which is happening everywhere from community banks[20] to Credit Suisse[21]. The money printer is now connected directly to your checking account. And in the digital era, the bank runs are of a historical scale.[22]

Remember also: the BTFP, swap lines, and FedDIC measures are *so enormous* that the Fed is doing them over weekends[23] with all the other central banks[24], and publishing multiple joint statements[25,26] assuring people that the “system is resilient”, even as Moody’s has downgraded the US banking system as a whole[27].

One of the things I hate about this system is that it’s evolved to be opaque, like a snake that’s evolved camouflage. If the Fed came outright and *said* they were digitally devaluing the dollar by printing trillions, that they were monetizing the debt as Dalio predicted[31] and even getting bondholders to abet the devaluation, everyone would flee for the Bitcoin exit. So instead they lie, to themselves and to others, just as Jean-Claude Juncker recommended[32]. As with CDOs[33] in 2008, the point is to fool themselves and to fool you.

But you have to see through the camouflage. They’re printing trillions[34,35] even as they’re hiking rates. Indeed, they’re printing trillions to compensate for the *consequences* of hiking rates. There will of course be other consequences to printing trillions. You can wait to find out, or you can get into Bitcoin now.

5 figures and 35 citations follow. 👇

English

Gideon Malherbe retweetledi

📁documents

└📁finance

└📁crypto

└📁reasons to use self-custody

└ 🚀vaultavo.com

OKX@okx

📁documents └📁finance └📁crypto └📁reasons to use self-custody └⚠️folder too large to open

English