Sabitlenmiş Tweet

Intel God

45 posts

Intel God

@God_Of_Intel

Just my thoughts on Intel/semiconductor. Not financial advice.

Katılım Nisan 2025

3 Takip Edilen20 Takipçiler

@zephyr_z9 $intc and $tsla stealing TSMC talent. It's come back season.

English

@aleabitoreddit $mbly owned by $intc had robotaxi and humanoids robots with 20b backlog at 7b marketcap.

There's decent chance of $tsla and $mbly collab in the future even if the CEO hate each other as Lip Bu is the meditator

English

@jukan05 @aleabitoreddit Intel pouch QCOM physical AI talent to help $mbly ($intc humanoids, robotics, robotaxi) division. $mbly is only 7 billion marketcap. Feels like the the market and analyst do not understand gold right in front of their eyes.

𝐷𝑟. 𝐼𝑎𝑛 𝐶𝑢𝑡𝑟𝑒𝑠𝑠@IanCutress

Breaking: @AlexKatouzian has left Qualcomm and joined @Intel as EVP of the Client Computing and Physical AI Group (CCAI?), reporting direct to CEO @LipBuTan1. Jim Johnson and Mike Hurley will report direct to AK. Also: @magicsilicon moves permanently to CTO. Congrats dude! #INTC

English

@mingchikuo If Intel needs 98% yields for EMIB-T then why did TSM advance their R&D in packaging once they heard about it (Reported by Jukan a while back). if you're going to shill for TSM at least provide all the facts instead of trying to take down $intc Make Intel Great Again

English

Some quick thoughts on Intel's EMIB-T packaging for the new 2H27 Google TPU (Humufish). Based on my industry checks:

【How to read EMIB-T's 90% yield?】

1. Given Intel's track record running EMIB in mass production, hitting 90% technology validation yield on EMIB-T (still under development) is a very positive but reasonable data point.

2. Intel benchmarks EMIB production/assembly yield against FCBGA. Industry FCBGA yield today is generally above 98%.

3. On yield, getting from 90% to 98% is harder than getting from project kickoff to 90%. And technology validation yield ≠ final production yield, especially with some Humufish specs still unfinalized. So long-term, I'm positive on Intel's advanced packaging story. Near to mid-term, I'm staying cautious on how they get there.

【From 90% to 98%. Looks like just a few points. Does Google care? Absolutely】

1. Google recently asked TSMC how much it could save by placing wafer orders for Humufish's main compute die (designed in-house by Google) directly, rather than routing them through MediaTek.

2. Google and MediaTek have run a semi-COT model since day one (8t). MediaTek's mark-up sits mostly on the parts it designs itself, so whether Google places the wafer orders for main compute die directly isn't a key swing factor for MediaTek's earnings trajectory.

3. But Google even probing whether it can squeeze out the pass-through mark-up on wafer orders tells you something: Google has shifted from easygoing buyer to hard-nosed on cost. The reason is simple: to take on Nvidia head-on, cost is Google's edge, which makes EMIB-T production yield Google's problem to solve. For context, TSMC's yield target on 5.5-reticle CoWoS in 2026 also starts at 98%.

【TSMC's position】

1. My understanding is TSMC is still working out how much advanced-node capacity to allocate to Humufish in 2H27, for two reasons: (1) it still wants the back-end packaging orders, though looks unlikely for now, and that's by design on Google's part; and (2) it's still gauging actual back-end output from EMIB-T, to avoid misallocating scarce advanced-node capacity.

2. Humufish's effective back-end output hinges on both EMIB-T and substrates, and both need to be tracked together.

3. On the Humufish semi-COT model, TSMC also prefers MediaTek to place the wafer orders for the main compute die. Beyond the close working relationship, the key point is MediaTek is TSMC's third-largest advanced-node customer in 2025. If TPU orders shift, MediaTek's scale makes it a natural buffer for TSMC to rebalance its wafer allocation mix.

English

@jukan05 @Alex_Intel_ One major flaw in your logic Jukan. All three major memory makers don't have Lip Bu Tan. He's exclusive to Intel. Make $intc great again

English

@Alex_Intel_ Logic-on-memory isn’t Intel’s exclusive domain. All three major memory makers are working on it. In fact, they’re already putting out samples.

English

@aleabitoreddit $mbly is currently 7b marketcap. You can't complain you didn't find 2026 AMD. NFA

English

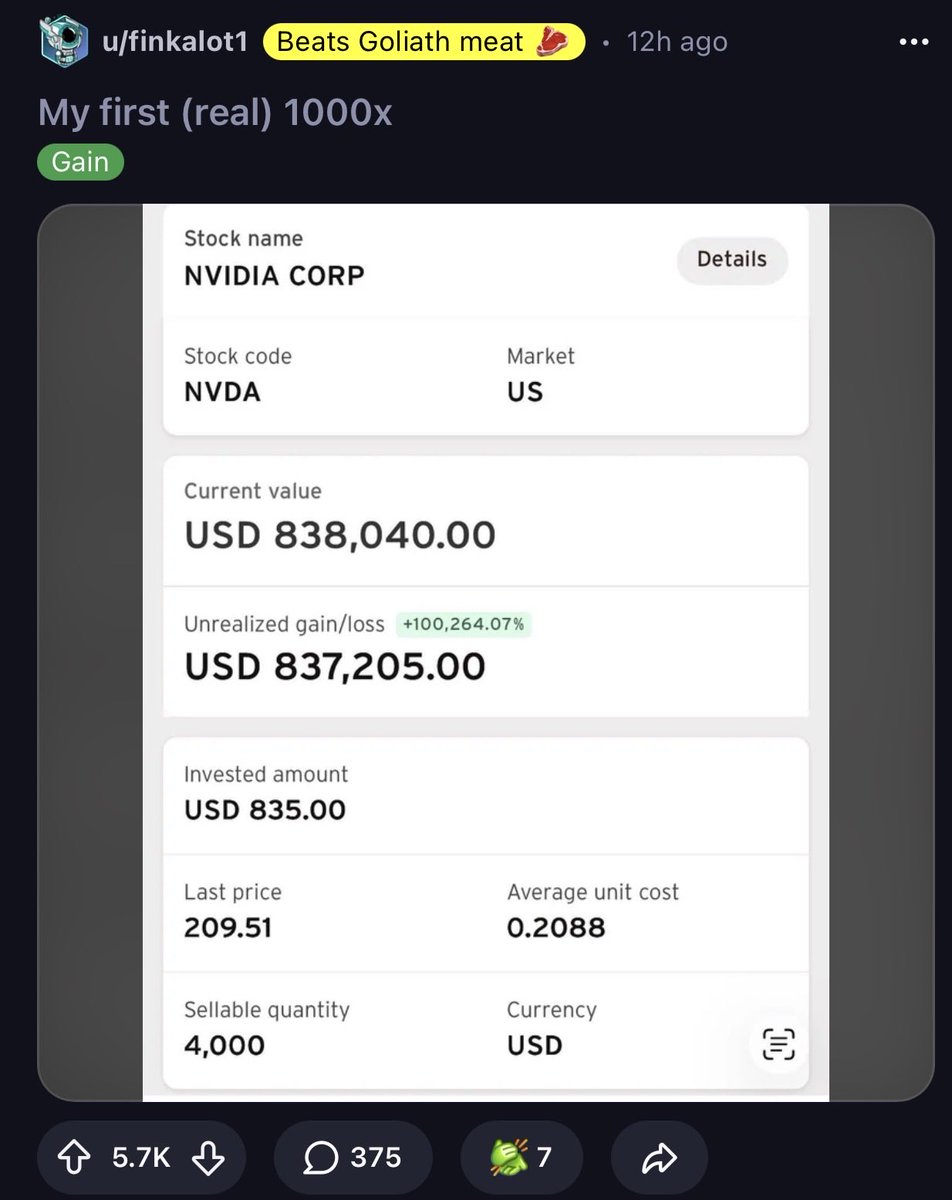

Wow... Someone turned $835 -> $838,000 from $NVDA shares.

This was shared on $RDDT. Unrealized gain was +100,264.07%.

From Oct 2008 -> April 2026.

See, it is possible to make generational wealth without too much to start.

Just gotta find the next Nvidia… easy, right chat?

English

Those selling the stock after reading the WSJ article on OpenAI fall into two categories:

1.Those who had been looking for an excuse to sell and are using this as the opportunity; and

2.Those who are simply dumb enough to follow the mood.

Why do you think Sam Altman declared “code red” last year? Obviously, it was because they were falling short of their targets.

If turning something everyone already knew into a sensational story counts as a skill, then I guess that is a skill.

English

@aleabitoreddit Trump technically owns $mbly since Intel owns 80%. Intel will rule the physical AI space.

English

Disillusioned by the growth of AI.

Starting to believe the only chance to escape the permanent underclass is in the next 5 years?

By owning compute and control of the infrastructure that makes AI and Robotics work.

Hard to see new generations having much opportunities, unless they’re highly specialized.

Especially with physical AI and automation coming to replace everyone in the human workforce.

All the value derived from AI will go to shareholders, without requiring the cost of labor.

English

@PatrickMoorhead @Mojo_flyin I know the stockholders hate each other. If Lisa and Pat is taking pics with each other then there's probably not that much bad blood left. Especially since LPT is brand new (besides being on the board)

English

When $AMD becomes an $INTC IFS customer we will know $INTC has achieved a substantial moat.

$AAPL $NVDA

Jukan@jukan05

According to Jeff Pu's estimates, Intel is expected to win a portion of the AI6 orders that were previously anticipated to be awarded exclusively to Samsung.

English

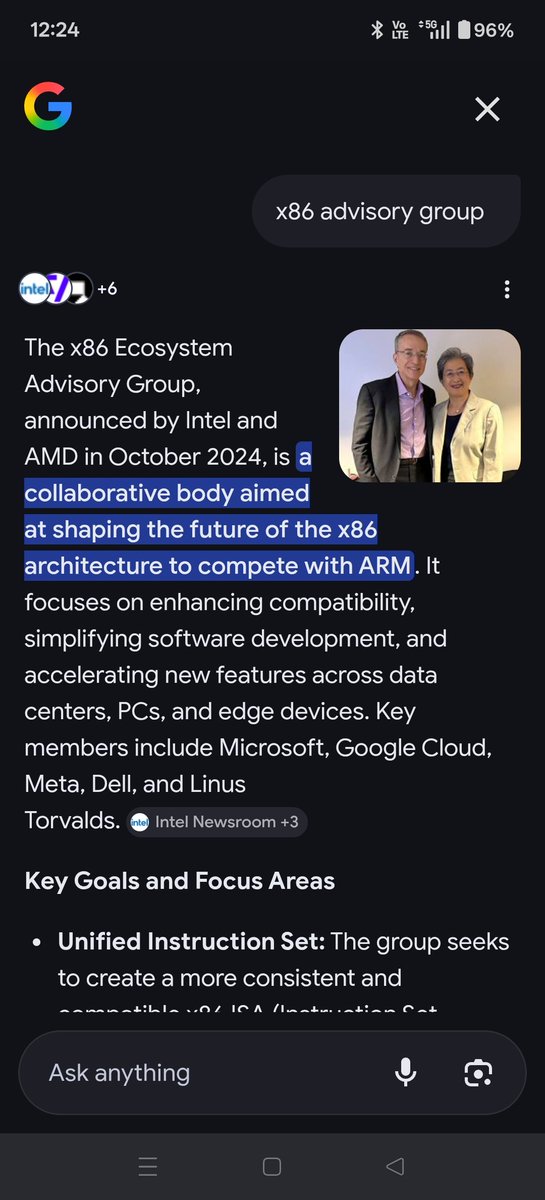

@PatrickMoorhead @Mojo_flyin They do have a x86 advisory group together. It's better for $intc to not take AMD short term as that would be helping AMD get more pie, when CPU currently has insane demand with supply constraint

English

@Mojo_flyin AMD will be one of the last companies to do wafers there. Smaller design teams. History of mutual hate. TSMC loyalty. Packaging, yes.

English

@jukan05 @Alisvolatprop12 The more bullish $intc you post, the more money you get. First law of Lip Bu Tan

English

@PatrickMoorhead Hope @LipBuTan1 poaches Srouji by delighting him.

English

CPU shortage more acute than memory; industry awaits Intel 18A yield improvement

A global CPU shortage is disrupting PC and industrial-computing supply chains, as processors are out of stock even at premium prices, while memory is limited but purchasable. The scarcity threatens notebook and industrial PC availability worldwide and may persist for some time until Intel's 18A process yields improve, industry sources warn.

Industry contacts described the current situation as more acute for processors than for memory, which is available in limited quantities at higher prices. By contrast, several processors are effectively unavailable regardless of price, affecting both Intel and Advanced Micro Devices (AMD). Suppliers said relief may hinge on improvements in Intel's 18A process yields.

Both Intel and AMD raised processor prices by 10-15% recently to reflect rising costs. Notebook supply chain representatives, however, reported no immediate expectation of further increases because product availability, rather than price, is the primary constraint. The most scarce parts are Intel's 2022 Raptor Lake series, and one source said lead times have become meaningless because waiting does not guarantee delivery.

Analysts foresee Raptor Lake discontinuation in 2026, prompting manufacturers to shift buying toward Arrow Lake and the newer Panther Lake processors. Given Panther Lake's higher cost, the market focus is expected to concentrate on Arrow Lake as the N-1 generation choice.

Industrial PC makers serving enterprise clients are particularly affected. While memory shortages can be eased by paying premiums, Intel CPUs are reported as genuinely unavailable. With Intel estimated to hold roughly 90% market share in industrial segments, the impact on IPC makers is pronounced.

Intel's supply constraints are expected to ease gradually as 18A yields improve, a point reportedly echoed by Intel CEO Lip-Bu Tan, who said 18A production has started, but yields remain below expectations. Some insiders warned consumer demand may cool in 2026, especially in the second half, as higher prices dampen seasonal sales, prompting vendors to adjust inventories cautiously.

Notebook original design manufacturer shipments exceeded expectations in the first quarter due to aggressive brand pull-ins and are expected to be stable in the second quarter, though manufacturers remain conservative about the latter half and foresee annual shipment declines versus 2025.

Observers noted that low-end Intel processors have been in short supply since 2025, a situation that once prompted some makers to switch to AMD; shortages are now reported across both vendors. Experts attribute the CPU scarcity to AI-driven demand surges that have strained capacity across GPUs, substrates, memory, passive components, and CPUs, framing the issue as an industry-wide upgrade and transition rather than an isolated corporate strategy.

$INTC $AMD

English

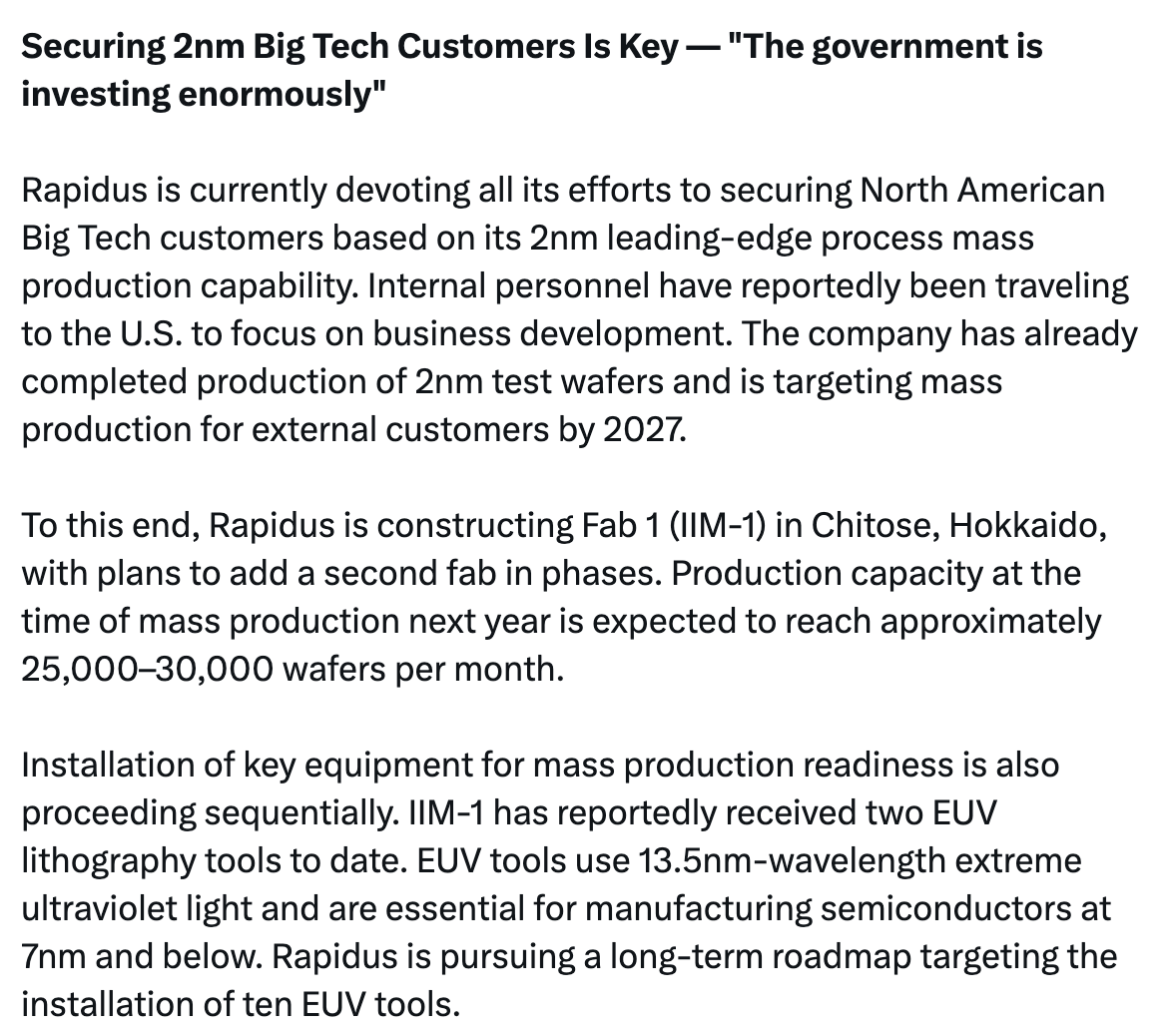

[Exclusive] Samsung Foundry 2nm Yield at 55%… Stuck Below the 'Mass Production 60%' Threshold

Samsung Electronics' foundry business — a key future growth engine — has hit a wall at the '60% mass production' threshold for its 2nm (nanometer; 1nm = one-billionth of a meter) process. With yields stuck in the mid-50% range and failing to enter stable mass production territory, effective yields are expected to drop to the 40% range once back-end processing is factored in. While the company has succeeded in achieving technical entry, the consensus is that it remains insufficient to win orders from global Big Tech clients.

According to semiconductor industry sources on the 13th, Samsung Electronics' foundry division's average yield for the 2nm process is understood to be approximately 55%. This is lower than the '60%-plus' estimates floated by some, signaling that additional time is still needed to reach mass production stability. A source with knowledge of internal affairs stated, "The 2nm process yield is in the 50–60% range, with an average around 55%," adding, "The process is running, but it is still a long way from a stable mass production phase."

The pace of yield improvement itself has been rapid. Samsung's foundry 2nm yields were reportedly stuck in the 20% range as recently as the second half of last year. Reaching the mid-50s in less than a year is assessed as technically reaching a level where the mass production line can be operated. This is attributed in part to the accumulation of process experience driven by incoming orders for Bitcoin mining chips from China's Canaan and MicroBT, among others. Given the extreme difficulty of the 2nm ultra-fine process, some consider this an exceptionally fast rate of improvement.

However, the prevailing view in the industry is that it remains a "half-process" at best. In a structure where nearly half of all wafer input is discarded as defective, the process fails on both price competitiveness and delivery reliability. In particular, when factoring in losses from performance binning and packaging, the actual percentage of chips that can generate profit is estimated to fall as low as 40%. Considering that a single wafer for cutting-edge processes costs tens of millions of won, a 1% difference in yield translates to annual operating profit differences ranging from hundreds of billions to trillions of won. This is bound to significantly derail Samsung Electronics' efforts to improve foundry business profitability.

An industry source said, "A yield in the 50% range only means the process 'runs' — it is not a stage where customers can entrust orders with confidence," adding, "It is a zone where both delivery and quality variability coexist."

By contrast, rival TSMC is reported to have secured stable yields of 60–70% for its 2nm process. Samsung Foundry's current mid-50% yield is therefore assessed as corresponding to the technical entry stage, but falling short for securing major customers — a "transitional zone." Significant progress has been made, but analysis suggests actual mass production remains premature.

In practice, Samsung has secured some customer and internal volumes, but has yet to achieve results in winning key clients such as Apple, NVIDIA, and AMD. Notably, Qualcomm — a global mobile application processor (AP) company that had raised expectations for new orders — is also showing signs of returning to TSMC, citing process yield and stability concerns. Additionally, the 'AI6' advanced autonomous driving chip contracted with Tesla is scheduled for mass production this year, and the yield level achieved at the actual production milestone will be critical in determining profitability and supply stability.

Meanwhile, Samsung Electronics' strategy is to win new orders, run its facilities, and improve yields going forward. At Samsung Electronics' annual general meeting on March 18, Han Jin-man, head of the foundry business division (President), stated, "For the 2nm process as well (which is at a higher level than the 4nm process), we can build up order experience with major companies and secure yields through that process."

$INTC $TSM

English

@jukan05 If TSMC care about relationship more than money than they would lower their margins. Business is business. It's better for Intel to fail in TSMC eyes, as that means less confidence for companies to try other foundryn like Samsung or rapidus in fear of execution failure.

English

@God_Of_Intel MediaTek and TSMC have a very close relationship. MediaTek’s pain is not good for TSMC either. It’s not that cold-blooded a relationship.

English

Interesting. Even within MediaTek itself, there are concerns about using Intel's EMIB.

1. Intel has no track record, and it can't even reliably handle its own volume.

2. If they commit to EMIB and it fails? They can't switch to CoWoS at that point. Even TSMC is worried about what might happen if MediaTek uses Intel EMIB and it fails.

$INTC $TSM

English

@God_Of_Intel TSMC does not think EMIB itself will necessarily fail. Rather, it seems concerned because if any issue arises with EMIB and disrupts MediaTek’s TPU shipments for Google, the impact would also flow back to TSMC. That is probably why it is worried.

English